Home Loans

Home Loans

Personal

Loans

Personal

Loans

SME Loans

SME Loans

Business Loans - Udyog

Plus

Business Loans - Udyog

Plus

Loan against Securities

Loan against Securities

Mutual Funds

Mutual Funds

Stock and

Securities

Stock and

Securities

Portfolio

Management Services

Portfolio

Management Services

Pension Funds

Pension Funds

Life

Insurance

Life

Insurance

Health

Insurance

Health

Insurance

Wellness

Solutions

Wellness

Solutions

Pay Bills

Pay Bills

Pay anyone

Pay anyone

Pay on call

Pay on call

Payment

Lounge

Payment

Lounge

ABC Credit

Cards

ABC Credit

Cards

1800-270-7000

1800-270-7000

Life Insurance

Buy New Plan

Existing Customer

Savings

Term-Life

Retirement

Child

ULIP

My Policy

Claims

Update Profile

Contact Us

Manage your policy with ease

Our easy claim settlement process provides a sense of security when you need it the most!

Stay Current, Stay Protected. Update your profile with ease!

Your questions are important.

We`re just a click away to answer your queries

WhatsApp Us

Register by giving a missed call on

+91 7676690033 or SMS OPT IN on 567679 from your registered mobile number.

Save +91 8828800040

as 'ABSLI Contact'.

Say 'Hi' to us on WhatsApp and you are done.

WhatsApp Us

Register by giving a missed call on

+91 7676690033 or SMS OPT IN on 567679 from your registered mobile number.

Save +91 8828800040

as 'ABSLI Contact'.

Say 'Hi' to us on WhatsApp and you are done.

Looking for the help with your claims, renewal

or Policy update? Please fill in the details and

we will get back to you.

Mail Us

Reach us at:

care.lifeinsurance@adityabirlacapital.com

For NRI Customer:

absli.nrihelpdesk@adityabirlacapital.com

Thank you!

We will call you shortly

Thankyou

Facing Some Issue

Different Types of Life Insurance Plans

Aditya Birla Sun Life Insurance (ABSLI) offers various life insurance plans to cater to diverse needs. Primarily, these can be categorised into Term Plans (Pure risk cover) and Investment Plans (Risk Protection + Investment Option).

Let's explore each:

Why Buy Aditya Birla Sun Life Insurance Plan?

Choosing Aditya Birla Sun Life Insurance (ABSLI) for your life insurance needs means more than just securing a policy; it's about entrusting your financial future to a name synonymous with reliability and excellence. Here's why ABSLI stands out:

Most Asked Questions on Life Insurance

|

Feature |

Term Life Insurance |

Whole Life Insurance |

|

Coverage Duration |

Fixed term (e.g., 10, 20, 30 years) |

Lifelong coverage |

|

Premiums |

Generally lower, fixed for the term |

Higher, fixed for life |

|

Cash Value |

No cash value component |

Builds cash value over time |

|

Investment Component |

None |

Yes, part of the premium goes into a cash value account |

|

Flexibility |

Less flexible, coverage ends after the term |

More flexible, can borrow against cash value |

|

Purpose |

Suitable for temporary needs, like a mortgage or income replacement |

Suitable for long-term needs, like estate planning or retirement savings |

● Waiver of Premium Rider: Waives your premium payments if you become disabled and unable to work.

● Accidental Death Benefit Rider: Pays an additional sum if your death is the result of an accident.

● Critical Illness Rider: Provides a lump sum payment if you're diagnosed with a specified critical illness.

● Age: Generally, the younger you are, the lower your premiums.

● Health: Your medical history and current health condition can impact your rates. A healthier individual usually pays lower premiums.

● Lifestyle: Habits like smoking, drinking, or high-risk habits can increase your premiums.

● Type of policy: Term life plan typically has a lower premium as it does not have investment component like other life insurance plans such as whole life, ULIP, savings plans.

● Coverage amount: The higher the life cover, the higher the premium.

● Term length: Longer terms usually mean higher premiums.

● Term Life Insurance: Provides coverage for a specific period (e.g., 10, 20, or 30 years). If you pass away during the term, your beneficiaries receive the death benefit. It's like renting a house for a fixed period; you have protection as long as you're paying the rent.

● Whole Life Insurance: Offers lifelong coverage and includes a cash value component that grows over time. It's like owning a house, where you have permanent protection and can build equity.

● Universal Life Insurance: A flexible policy that combines lifelong coverage with an investment component. You can adjust premiums and death benefits over time, similar to having a customizable financial plan.

● Endowment Policies: These policies have a maturity date and pay out the sum assured either on death or on the policy reaching maturity, whichever comes first. They're like a savings plan with a life insurance component.

● Parents with Young Children: If you have children who depend on your income for their upbringing, education, and overall well-being, life insurance is crucial. It ensures that your children can maintain their standard of living and pursue their dreams even in your absence.

● Couples with Shared Financial Obligations: If you're in a relationship where both partners contribute to shared financial goals, such as paying off a mortgage or saving for retirement, life insurance can help ensure that these goals are still achievable if one partner passes away.

● Individuals with Debt: If you have debts like a home loan, car loan, or personal loan, life insurance can help ensure that your loved ones aren't burdened with these financial obligations after you're gone.

● Business Owners: If you own a business, life insurance can help protect your business partners and employees. It can provide funds to keep the business running or to buy out your share in the event of your death.

● People with Dependents: If you have ageing parents or siblings who rely on you for financial support, life insurance can help ensure their continued care.

● High-income Earners: If you're a high-income earner, life insurance can help preserve your family's lifestyle and future financial security.

● Estate Planning: Life insurance can be used as a tool for estate planning, providing liquidity to pay estate taxes and settle other financial matters.

For example, let's say you're a 35-year-old parent with two young children and a spouse who is a homemaker. If you're the primary breadwinner, your family relies on your income for their daily expenses, education, and future aspirations. In this scenario, having a life insurance policy ensures that your family has financial support to continue their lives without drastic changes in the event of your untimely death. Life insurance also helps you to build corpus to fulfil long-term and short-term financial goals.

Life insurance is not just for the elderly or the wealthy; it's for anyone who has financial responsibilities or people who depend on them. It's a way to ensure that your loved ones are taken care of, even when you're not there to provide for them.

In simpler terms, it's a way to ensure that your family remains financially secure even when you're no longer around to support them.

Here's how Life insurance works:

● Policy Selection: You start by choosing a life insurance policy that suits your needs. There are various types of policies, such as term life, whole life, and universal life, each with its own features and benefits.

● Premium Payments: Once you've selected a policy, you agree to pay a regular amount, known as a premium, to the insurance company. These payments can be made monthly, quarterly, semi-annually, or annually, depending on the policy terms.

● Coverage Period: If you opt for term life insurance, your coverage will last for a specific period, say 10, 20, or 30 years. On the other hand, whole life and universal life policies provide coverage for your entire life.

● Death Benefit: In exchange for your premium payments, the insurance company promises to pay a sum of money, known as the death benefit, to your designated beneficiaries upon your death. This benefit can be used by your loved ones to cover funeral expenses, pay off debts, or provide for their future financial needs.

● Cash Value (for permanent policies): Some life insurance policies, like whole life and universal life, also have a cash value component that grows over time. This cash value can be borrowed against or withdrawn during your lifetime under certain conditions.

For example, let's say you purchase a term life insurance policy with a coverage amount of ₹50 lakhs and a term of 20 years. You pay a monthly premium of ₹1,000. If you were to pass away during those 20 years, your beneficiaries would receive the ₹50 lakh death benefit, providing them with financial support in your absence.

In summary, life insurance is a crucial tool for financial planning, offering peace of mind that your loved ones will be taken care of financially when you're no longer there to support them.

- Visit the ABSLI Website: Go to the official website of ABSLI.

- Log In to Your Account: If you're a registered user, log in using your credentials. If you haven't registered yet, you may need to create an account using your policy number, date of birth, and other personal details..

- Access Your Policy Details: Once logged in, navigate to the section where your policy details are displayed. This usually includes your policy status, premium details, nominee information, and other relevant data..

- Download/View Documents: Often, there's an option to download or view your policy documents for your reference.

- Customer Support: If you face any issues or need additional information, you can always contact the insurer’s customer support for assistance..

- Identity Proof: A valid government-issued ID such as a passport, driver's license, or Aadhar card.

- Age Proof: Documents like your birth certificate, passport, or PAN card can be used to verify your age.

- Address Proof: Utility bills, bank statements, or government-issued documents that have your current address.

- Income Proof: Recent salary slips, Income Tax Return (ITR) documents, or an employer's certificate that validates your income.

- Medical Records: Depending on the policy and the insurer, you might be asked for medical reports or a declaration of good health.

- Photograph: A recent passport-sized photograph.

- Other Documents: Depending on the insurer, there might be additional forms or declarations to be filled out.

- Financial Security: It provides financial security to your loved ones in the event of your untimely demise, ensuring they are not burdened by debts or living expenses.

- Debt Protection: Helps in covering any outstanding debts, like home loans or personal loans, so that the burden doesn’t fall on your family.

- Income Replacement: Acts as an income replacement, especially if you are the primary breadwinner of the family.

- Long-Term Goals: Assists in achieving long-term financial goals like children’s education or retirement planning, depending on the type of policy you choose.

- Tax Benefits*: Offers tax benefits* under various sections of the Income Tax Act, adding to your savings.

- Income and Expenditure: Consider your current income, regular expenses, and the lifestyle you wish to secure for your family.

- Financial Liabilities: Factor in debts like loans or mortgages that need to be paid off.

- Future Goals: Account for future financial obligations, like children’s education or marriage.

- Inflation: Keep in mind the impact of inflation on future expenses.

- Insurance Needs: Analyze how much financial coverage your family would need in your absence.

- Affordability: Choose a sum assured that aligns with a premium you can comfortably afford.

- Age: Younger applicants generally pay lower premiums as they are considered less risky.

- Health: Medical history and current health status can affect premium rates.

- Lifestyle: Habits like smoking or high-risk hobbies can lead to higher premiums.

- Policy Type and Term: Different types of policies and coverage periods have varying premium rates.

- Sum Assured: Higher the sum assured, higher the premium.

- Riders/Add-ons: Additional coverage options selected can increase the premium.

- Grace Period: Most policies offer a grace period (typically 15-30 days) after the due date for paying the premium without losing coverage.

- Policy Lapse: If the premium is not paid within the grace period, the policy may lapse, and the coverage will cease.

- Reinstatement: Many insurers allow policy reinstatement within a specific period post-lapse, but this may involve paying all due premiums, interest, and possibly undergoing a medical examination.

- Loss of Benefits: A lapsed policy means loss of life cover, and in the case of certain policies, a loss of accumulated benefits or bonuses.

- Term Insurance: Usually, there are no survival benefits under pure term insurance policies.

- Endowment Plans, Whole Life Insurance, ULIPs: These policies often include survival benefits, paying out a maturity amount if you outlive the policy term.

- Notification: Inform the insurance company about the policyholder’s death as soon as possible.

- Documentation: Submit the required documents, which typically include the death certificate, policy documents, ID proof of the beneficiary, and a claim form.

- Claim Processing: We will process the claim after verifying the documents.

- Claim Settlement: Once the claim is approved, the death benefit is paid to the nominee(s).

- Financial Protection: Life insurance is worth buying for financial protection and peace of mind, ensuring that your family remains financially secure in your absence

- Debt Coverage: It can cover outstanding debts, preventing financial burden on your family.

- Tax Benefits*: Offers tax savings, which can be an added incentive.

- Investment Component: Some life insurance policies come with an investment component, aiding in wealth creation over time.

- Individual Needs: The worth of life insurance ultimately depends on individual circumstances, financial goals, and family responsibilities.

- Multiple Beneficiaries: You can name multiple beneficiaries on a life insurance policy. The number can vary based on the policy terms and the insurer's guidelines.

- Primary and Contingent: Beneficiaries are often categorized as primary (first in line to receive the death benefit) and contingent (receive the benefit if the primary beneficiaries are deceased).

- Percentage Allocation: You can specify the percentage of the death benefit each beneficiary will receive. This allocation must total 100%.

- Changes and Updates: It's important to regularly review and update beneficiary information, especially after major life events like marriage, divorce, or the birth of a child.

- Claim Process Duration: The time it takes to receive the life insurance amount after a death can vary. Typically, once a claim is filed with the necessary documentation, the insurance company may take a few days to a few weeks to process the claim.

- Documentation and Verification: Prompt submission of required documents like the death certificate, claim form, and policy document can expedite the process. The insurer will review and verify these documents.

- State Regulations: Some regions have specific regulations about how quickly insurance companies must process claims. It's advisable to check local laws for guidance.

- Complex Cases: In cases where the claim is complex or if there's an investigation (e.g., in the event of suspicious circumstances surrounding the death), the process can take longer.

- Financial Obligations: Consider your debts, like mortgages or loans, and ongoing financial responsibilities.

- Income Replacement: Calculate how much income your family would need to maintain their lifestyle in your absence. A common approach is to choose a cover 10-15 times your annual income.

- Future Goals: Factor in future expenses like children’s education or retirement planning for your spouse.

- Inflation: Account for inflation and how it might affect future financial needs.

- Existing Savings and Assets: Deduct your current savings and investments from the total required sum to avoid over-insuring.

- Financial Adviser: Consulting a financial adviser can provide personalized advice based on your specific circumstances.

- Type of Policy: Term insurance is generally more affordable than whole life or investment-linked policies.

- Age and Health: Younger, healthier individuals typically pay lower premiums.

- Lifestyle Factors: Smoking or high-risk hobbies can increase premiums.

- Coverage Amount: Higher sums assured lead to higher premiums.

- Term Length: Longer policy terms can increase the cost.

- Riders/Add-ons: Additional coverage options will increase the premium.

- Gender and Occupation: These can also influence the cost.

- Frequency: Options often include monthly, quarterly, semi-annual, or annual payments or lumpsum one-time payment.

- Methods: Payments can be made via direct debit, credit card, online transfers, checks, or even cash at the insurer’s office.

- Automatic Payments: Setting up autopay can ensure premiums are paid on time and prevent policy lapse.

- Term Insurance: These policies typically do not have a maturity benefit.

- Endowment and Whole Life Policies: You will receive the sum assured along with any bonuses or dividends accrued, if applicable.

- ULIPs: The maturity benefit will include the sum assured and the value of the investment component.

- Payout: The maturity amount is usually paid out as a lump sum, but some policies offer structured settlement options.

- Tax Implications: Be aware of any tax implications on the maturity proceeds, as per recent Tax laws.

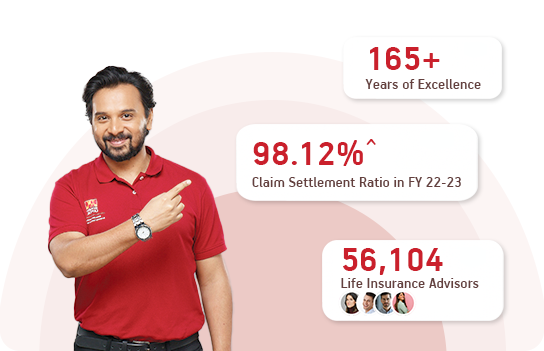

● 98.12%^ Claim Settlement Ratio

● 56,104 Life Insurance Advisors$

● ₹50,688 Crores Assets Under Management^

● 165+ Years of Excellence

The Insurance Regulatory and Development Authority of India (IRDAI) is the government agency responsible for policing the Indian insurance sector, including Aditya Birla Sun Life Insurance. As a result, policyholders have some assurance that the firm is operating in accordance with IRDAI norms and regulations.

Keep in mind, however, that investing in life insurance carries with it certain inherent dangers, and that you can never be sure that you will get the profits you anticipate. Before investing in a life insurance policy, it's vital that you read the policy's terms and conditions thoroughly and consult a financial counsellor if you have any doubts or queries.

It's crucial to perform one's own research and due diligence before making any investment selections, but Aditya Birla Sun Life Insurance looks to be a safe alternative for investing in India.

However, there are certain exceptions to this rule. If the premium paid on the policy is more than 10% of the sum assured for policies issued after April 1, 2012, then the amount received upon maturity or surrender will be taxable. Additionally, if the policy is transferred to another person for consideration, the proceeds may also be taxable.

It's important to note that the tax laws in India are subject to change, so it's always a good idea to consult a tax professional for the most up-to-date information.

Voice of Happy Customers

ABSLI provides various payment option to pay renewal premium, anytime and anywhere.! Best wishes to ABSLI

Mr. Singh

West Bengal

Entire surrender process was quite smooth with timely documentation and payout. Great experience!

Mr. Ganvit

Gujarat

Easy and simplified surrender process with a supportive branch and speedy payout experience!

Mr. Joshi

Maharashtra

Due to seamless branch support and timely communication from ABSLI, my maturity payout process was quite smooth.

Mr. Bansal

Haryana

Renewal payment through ECS has been quite smooth with timely reminders for the same. Great experience!

Mrs. Maheshwari

Madhya Pradesh

Looking for Assistance...

Latest Life Insurance Articles

-

Disclaimer

*Tax benefits are subject to changes in tax laws. Kindly consult your financial advisor for more details.

**Sec 10(10D) benefit is available subject to fulfilment of conditions specified therein

#Provided all due premiums are paid

^ As per annual audited figures submitted to IRDAI for the period FY 22 – 23 for individual death claims paid.

$ As on 30`th November 2023

¹LI Age 21, Male, Non Smoker, Option 1: Life Cover, PPT: Regular Pay, SA: ₹ 1 Cr., PT: 10 years, Premium paying term: 10 years, Annual Premium: ₹ 5900/- ( which is ₹ 491.66/month) Premium exclusive of GST. On death, 1 Cr SA is paid and the policy terminates.

² Provided 0 year deferment & monthly income frequency is chosen at the time of inception of the policy.

³ Guaranteed Annuity Plus Plan, Annuitant -Health Male: Age 45 years | Annuity Option: Deferred Life Annuity with Return of Premium | Premium payment term – Limited pay (5 years) | Purchase Price: Rs. 10,00,000/ year for 5 years | Deferment period: 15 years Annuity Pay-out Frequency: Annual | Single life. Get Rs 6,94,936/- (Exclusive of taxes) from the end of 15 years, every year till annuitant is alive.

⁴ABSLI Child’s Future Assured Plan. Plan option: Education & Marriage Milestone. Male | Age: 35 years | Policy term: 25 years | Premium paying term: 10 years | Education milestone benefit period: 3 yrs & Education assured benefit start term: 15 yrs | Marriage assured benefit start term: 25 years | Annualized premium: ₹1,00,000 (excluding tax) | Total Benefits Payout: Rs 21,58,664 [Education Milestone Payout: Rs 10,79,332 (policy year 15,16,17) and Marriage Milestone Payout: Rs 10,79,332 (policy year 25)] | Age of Child: 0 years, Child as a nominee | Sum assured multiple for marriage: 100%

⁵Male | Age: 35 Years | Sum Assured: Rs. 1,00,00,000 | Sum Assured Multiple: 50X | Annualized Premium: Rs. 2,00,000 | Premium Payment Term: 6 years | Policy Term: 20 years | Investment Option: Self-Managed Option | Fund Chosen: Maximizer | Premium Payment Mode: Annual | Comprehensive Critical Illness Rider: Silver Variant (10 CIs) | Comprehensive Critical Illness Rider Sum Assured: 75% of Base Sum Assured: Rs. 75,00,000 | Comprehensive Critical Illness Rider Premium: Rs. 55,875 | Accidental Death Benefit Plus Rider Sum Assured: Rs. 1,00,00,000 | Accidental Death Benefit Rider Plus Premium: Rs. 13,800 | Waiver of Premium Rider: Rs. 7,875 Depends on age, PPT, PT chosen at inception of the policy.

⁶Scenario: Healthy male age 25 years, premium paying term 10 years, policy term 20 years, payment frequency monthly, Sum Assured Rs. 16.2 lakhs, Premium Rs.10000/month excluding GST), you get Rs. 30.48 lakhs by age 45

ABSLI Accidental Death And Disability Rider - This rider is underwritten by Aditya Birla Sun Life Insurance Company Limited (ABSLI). UIN: 109B018V03

ABSLI Critical Illness rider. This rider is underwritten by Aditya Birla Sun Life Insurance Company Limited (ABSLI). UIN: 109B019V03

ABSLI Surgical Care Rider. This rider is underwritten by Aditya Birla Sun Life Insurance Company Limited (ABSLI). UIN: 109B015V03

ABSLI Hospital Care Rider. This rider is underwritten by Aditya Birla Sun Life Insurance Company Limited (ABSLI). UIN: 109B016V03

ABSLI Waiver Of Premium Rider. This rider is underwritten by Aditya Birla Sun Life Insurance Company Limited (ABSLI).UIN: 109A039V01

ABSLI Nishchit Aayush Plan. This is a non-linked non-participating individual savings life insurance plan. UIN No 109N137V06

ABSLI Assured Savings Plan. his is a Non-Linked Non-Participating Individual Savings Life Insurance Plan.UIN: 109N134V08

ABSLI DigiShield Plan. This is a non-linked non-participating individual pure risk premium life insurance plan; upon Policyholder’s selection of Plan Option 9 (Level Cover with Survival Benefit) and Plan Option 10 (Return of Premium [ROP]) this product shall be a non-linked non-participating individual life savings insurance plan. UIN: 109N108V11

ABSLI Salaried Term Plan. This is a non-linked non-participating individual pure risk premium life insurance plan; upon Policyholder’s selection of Plan Option 2 (Life Cover with ROP) this product shall be a non-linked non-participating individual savings life insurance plan.UIN:109N141V01

ABSLI Assured Income Plus. This is a Non-Linked Non-Participating Individual Savings Life Insurance Plan. UIN: 109N127V13

Aditya Birla Sun Life Insurance SALARIED SURAKSHA ULIP Plan (UIN: 109L145V01) is a unit linked non-participating individual life insurance savings plan

ABSLI Guaranteed Annuity Plus. This is a Non-Linked, Non-Participating, General Annuity Plan All terms & conditions are guaranteed throughout the Policy Term. GST and any other applicable taxes will be added (extra) to your premium and levied as per extant tax laws. UIN: 109N132V09

In the Unit Linked Policy, the investment risk in the investment portfolio is borne by the Policyholder.

Linked Life insurance products are different from the traditional life insurance products and are subject to the risk factors.

Linked Insurance Products do not offer any liquidity during the first five years of the contract.

The policyholder will not be able to withdraw/surrender the monies invested in Linked Insurance Products completely or partially till the end of the fifth year from inception. Please know the associated risks and the applicable charges, from your Insurance agent or the Intermediary or policy document. The premium paid in unit linked life insurance policies are subject to investment risk associated with equity markets and the unit price of the units may go up or down based on the performance of fund and factors influencing the capital market and the policyholder is responsible for his/her decisions. Tax benefits may be available as per prevailing tax laws. For more details on risk factors, terms and conditions please read sales brochure carefully before concluding the sale.

For further details regarding the above-mentioned rider, please refer to the respective rider brochure(s) available on our website.

Honesty is the best policy

Applicants should ensure that insurance details in the application form is filled by oneself with “ Utmost good faith”.

Be honest & truthful about your medical history, health conditions, or any other complications.

Also, let the insurer know about any habits like use of alcohol, tobacco or any narcotics/ psychotropic substances in the present or past, to ease the process of Policy issuance and claim assessment process.

ADV/2/23-24/3667