- All Insurance

- Endowment PlansNew

- Savings PlansNew

- Term InsuranceNew

- Pension PlansNew

- Critical Illness Insurance

- ULIP PlanNew

- Group Insurance

- Protection Solutions

- Employer Employee

- Voluntary

- Affinity

- Credit Life

- Retirement Solutions

- Annuity Scheme

- Gratuity

- Leave Encashment

- Post Retirement Medical Benefits Scheme

- Superannuation

- Withdrawn Products

- NRI PlansNew

- Articles

- Where Do I?

- Term Insurance

- Manage My Policy

- Her Insurance

Connect

Aditya Birla Sun Life Insurance Company Limited

Aditya Birla Sun Life Insurance Company Limited

Claim Related FAQs

Have questions? We’ve got the answers.

The claim money will be paid to the beneficiary who generally is the nominee / assignee / appointee (in case of a minor) as mentioned by the Life Assured in the Application Form for Insurance.

In such an eventuality, a "Succession Certificate" will have to be submitted by the Claimant. A Succession Certificate is issued on application by a competent court on the question of the right to the property of the deceased. The Succession Certificate should specifically provide for disbursement of policy monies. If, however, the deceased has left a will, a probate of the will is required along with the copy of the will.

The Life Assured should nominate some other person in place of the deceased Nominee under section 39 of the Insurance Act.

Except in some type of claims (e.g. Critical Illness Rider), where a waiting period is involved, all claims including death claims should be intimated as soon as possible.

The claimant or the family members of the Life Assured should inform the ABSLI Branch Office about the death of the Life Assured. Alternatively, they can directly intimate the Claims Section at:

The Claims Section, Aditya Birla Sun Life Insurance Company Limited G Corp Tech Park, 5th & 6th Floor, Kasar Wadavali, Ghodbunder Road, Thane - 400 601.

You can buy a term insurance plan anytime between 18 years to 65 years of age. As one’s age increases, the premium for the policy increases too. Hence, it is better to start early and in good health.

| Policy Year | Policy Term (upto 20 years) | Policy Term (above 20 years) |

|---|---|---|

| 1 to 5 | 100% | 100% |

| 6 to 10 | 90% | 95% |

| 11 to 15 | 75% | 90% |

| 16 to 20 | 50% | 85% |

| 21 to 25 | N.A. | 70% |

| 25 to 30 | N.A. | 50% |

Buying a term insurance plan is very easy. You can buy it online or offline. If you wish to buy term insurance online:

- Go to the website of your chosen insurance provider. Select the plan that meet your requirements.

- Fill up personal details such as name, gender, date of birth, policy term, smoking habit, city of residence, sum assured, mobile number, email id, etc

- The insurer would generate a quote based on the details which will let you know about the monthly/annual premium to be paid to get the term cover

- If you are satisfied with the quote, you would need to provide additional details such as nominee’s name, health and employment details, among others

- Make payment online through any of the digital payment modes

- Upload scanned copy of KYC documents and others as required

- The soft copy of the insurance policy will be mailed to your registered email id In case you get stuck, you can call the customer care who will provide the necessary assistance. Also, most insurers have chatbots on their website to guide you with the entire process.

On the other hand, if you wish to buy term insurance offline, you can do so from an insurance advisor. Fill up the proposal form and submit the relevant documents. Whether you buy term insurance online or offline, make sure to provide accurate details, particularly related to your health. Hiding information may lead to a claim rejection.

Also, before policy issuance, you may need to undergo a medical examination. Insurers do so for better risk assessment. Make sure not to skip it as it may reveal conditions that you aren’t aware of.

- Chose a plan that best answers the below questions for you What are the features offered by the plan? - Some important features to look out for will be flexibility in enhancing the cover as per your need, cover critical illnesses or cover all your protection needs.

- How much premium are you required to pay? – Do evaluate a term plan from a Company who has a legacy of trust and then identify the maximum coverage that you can get at an affordable cost

- What is your payment term? – Look out for a plan that provides you flexibility in choosing the payment term. For example, you may decide to pay premium in lumpsum amount or in monthly/yearly instalments

- What is the additional coverage (riders) being offered? – These are helpful additional features that you can check out like include waiver of premium, accidental benefits, etc.

- How good is the insurer’s claim settlement ratio? – The higher and more consistent the claim settlement ratio, the quicker and more robust is the company in its claim settlement process

- What is the insurer’s solvency ratio? - As per IRDAI, every life insurance provider should have a solvency ratio of 1.5, which tells if the company will be financially capable of settling your claim, should such a requirement arise.

In addition to benefit applicable for Option 1, in case you are diagnosed with Critical Illness^ or Total and Permanent Disability^ whichever is earlier, all future premiums, if any, will be waived off and policy will continue till end of policy term.

Demat of Insurance

The objective of creating an insurance repository is to provide policyholders a facility to keep all his insurance policies in electronic form in one account and to undertake changes, modifications and revisions in the insurance policy with speed and accuracy.

Once the investor opens an account with a Repository. He can purchase subsequent policies from any insurance company without the hassle of submitting KYC documents (Know your customer documents, ID & Address proofs) again.

All individual life insurance policies, health and pension policies issued by registered life insurance, Health Insurance and General Insurance companies registered with IRDAI.

In order to hold e- insurance policies a separate and distinct e‐insurance account shall be opened with insurance repositories for keeping insurance policies in electronic form and the same shall be opened by a person who has insurance policies on his own or who proposes to take insurance policies.

The documents that would be required are an Application form & KYC norms (ID Proof, Address Proof).

Subject to the provisions of insurance act and such Regulations, guidelines as may be made in this behalf from time to time, a policyholder may assign a policy of life insurance through insurance repository.

EInsurance

An e-Insurance account will be opened within 7 days from the date of submission of application complete in all respects. Once, an account is opened, a welcome kit with the details of how to operate the same would be sent to the applicant/e-Insurance account holder.

NO. e-Insurance account is offered 'free of cost' to the applicants.

The objective of creating an insurance repository is to provide policyholders a facility to keep insurance policies in electronic form and to undertake changes, modifications and revisions in the insurance policy with speed and accuracy. In addition, the repository acts as a single stop for several policy service requirements. The Insurance repository system also brings about efficiency and transparency in the issuance and maintenance of insurance policies.

"Insurance Repository" means a company formed and registered under the Companies Act, 1956 (1 of 1956) and which has been granted a certificate of registration by Insurance Regulatory and Development Authority (IRDA) for maintaining data of insurance policies in Electronic form on behalf of Insurers. The Insurance Repositories provide the ease of holding insurance policies issued in an electronic form.

No, only an entity which is registered under company's act and who is granted a 'Certificate of Registration' by Insurance Regulatory and Development Authority (IRDA) can act as an Insurance Repository.

An e-Insurance account will be opened within 7 days from the date of submission of application complete in all respects. Once, an account is opened, a welcome kit with the details of how to operate the same would be sent to the applicant/e-Insurance account holder.

NO. e-Insurance account is offered 'free of cost' to the applicants.

The objective of creating an insurance repository is to provide policyholders a facility to keep insurance policies in electronic form and to undertake changes, modifications and revisions in the insurance policy with speed and accuracy. In addition, the repository acts as a single stop for several policy service requirements. The Insurance repository system also brings about efficiency and transparency in the issuance and maintenance of insurance policies.

"Insurance Repository" means a company formed and registered under the Companies Act, 1956 (1 of 1956) and which has been granted a certificate of registration by Insurance Regulatory and Development Authority (IRDA) for maintaining data of insurance policies in Electronic form on behalf of Insurers. The Insurance Repositories provide the ease of holding insurance policies issued in an electronic form.

No, only an entity which is registered under company's act and who is granted a 'Certificate of Registration' by Insurance Regulatory and Development Authority (IRDA) can act as an Insurance Repository.

Investment

An 'asset class' is a group of investment instruments such as equity, debt, cash, etc., which have similar investment risk and return profile. Equities comprise of investments in various company stocks and though contain high levels of risk, are the best performing asset over the long term. Debt investments mainly consist of fixed deposits, government securities, corporate debt, etc. These generate a fixed return and generally face lower risk as compared to equities. Cash investments include saving deposits and short term money market investments and are exposed to negligible risks.

The risk-return profile is the relationship between the risk that an asset class is exposed to and the returns it generates. Generally, higher the risk involved in an asset class, higher is the return associated with it. For example, equity has the potential to generate higher returns than debt, but at a higher risk. Cash on the other hand, though the safest asset class, generates the lowest returns. E.g. An individual who invested in the equity market in April-September 2009 would have generated a whooping 76% returns on his investment but if he had invested in the entire Financial Year 2009 - 2010 he would have incurred a loss on investment of -38%. Further, his investment would have grown at a Compounded Annual Growth Return (CAGR) of approx 23% had he invested for a period of 20 years ending in September 2009. On the other hand, savings in bank will generate a stable return of 3-4% per annum with no downside risk and no upside potential as well whereas value of cash kept at home without investing will keep shrinking over a longer period of time due to inflation.

To determine your risk appetite you will have to consider several factors such as your age, number of dependants, income, future goals, etc. Your risk appetite may not remain constant and change depending on your life stage and financial status.

The process of dividing your investments across different asset classes is known as 'asset allocation'. By spreading your investment across different asset classes, you create a diversified portfolio where the loss that you may make on a certain asset class can be compensated by the profits that you make on another. Thus, you reduce the overall risk of your investments.

Your risk appetite, investment objective and investment horizon will determine the asset allocation between debt and equity. Higher the risk appetite and longer the investment horizon larger will be the allocation towards equity and vice versa. An ideal portfolio should have a judicious mix of various asset classes.

Login

To access and manage your policy account online you would need your CIP/User Name and TPIN/Password.

Yes, you would need to change your CIP & TPIN to User Name & Password of your choice. To change the same click on the log-in tab and type in your existing CIP (10 digit number), then follow the instructions.

Please click on Register tab and proceed to enter your Customer ID number followed by your registered e-mail id.

With your User Name and Password, you can manage your policy online. You can transact and view your policy details.

Online access benefit's

• Change or update your contact details. • Change the mode of your policy. • Switch of funds and Premium redirection. • Pay your premiums online (even for policies which are lapsed). • Generate the reinstatement quote.

You may have trouble logging in because of incorrect CIP/User Name and Password.

Policy Servicing

Survival Benefit is the amount which is paid to the policy holder at the end of the policy term on Monthly/Quarterly/Annually basis the due date of the policy.

Submit the survival certificate at nearest ABSLI branch. To locate a ABSLI branch nearest to you, click here: https://www.adityabirlacapital.com/branch-locator (Timings: Monday to Saturday 9:30 am to 6:00 pm).

Or

Submit the Survival Certificate through our Customer Portal.

Follow the below steps to upload the Survival Certificate through Customer Portal

|

Who has ONE ABC Login |

Who don't have ONE ABC Login |

|

Register user can login by ONE ABC ID |

Click on Manage my Policy -> Policy Servicing -> Submit Survival Certificate |

|

Click on My Services –> My policy Details -> Submit Survival Certificate |

Enter Registered Email ID/ Mobile No./ Policy No. and Primary Life Insured Date of Birth. In the OTP screen, enter the password and click on "Verify" |

|

On the policy dashboard screen click on "Submit Survival Certificate" button. |

On the policy dashboard screen click the "Submit Survival Certificate" button. |

|

Agree T&C and click on "Allow" to access camera. Smile and say "Namaste ABSLI"Or just smile while using phone to click selfie. |

Agree T&C and click on "Allow" to access camera. Smile and say "Namaste ABSLI"Or just smile while using phone to click selfie |

|

Upload PAN or Aadhaar card images - front/main side only. This can be done by capturing a fresh photo through the screen or by choosing the upload option if you already have an image stored on your device |

Upload PAN or Aadhaar card images - front/main side only. This can be done by capturing a fresh photo through the screen or by choosing the upload option if you already have an image stored on your device |

|

If all steps have been done properly, you will receive a "Success" message confirming your request number |

If all steps have been done properly, you will receive a "Success" message confirming your request number |

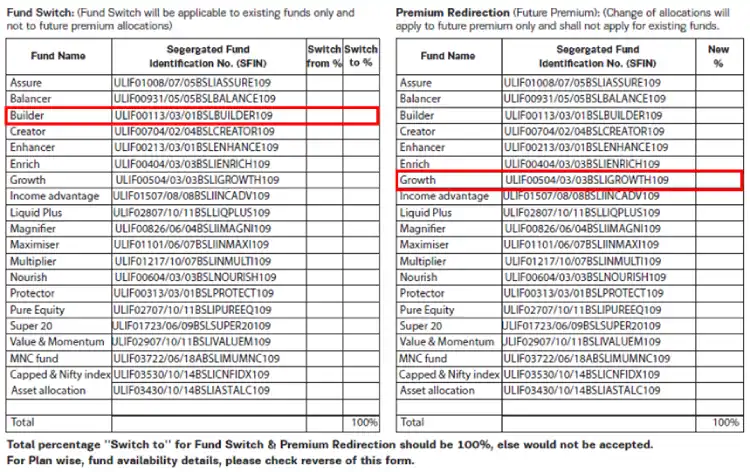

**Switch in Fund **– Fund Switch is the facility provided to the policy owner to switch existing fund option in the policy to available fund options as per the plan. On receiving this request, the existing fund value is moved to the fund requested by the customer.

Premium redirection – Premium redirection or Premium Allocation is an option given to the customer to redirect future premiums in requested fund available under the plan. Existing funds will continue to remain in old funds unless switch request is accompanied with the premium redirection request.

-

Branches: Submit fund switch form duly Signed by the Policy Owner. To locate nearest ABSLI branch click here: https://www.adityabirlacapital.com/branch-locator (Timings: Monday to Saturday 9:30 am to 6:00 pm).

-

Email: Submit switch request by writing to us on care.lifeinsurance@adityabirlacapital.com from registered email id. Provided if the client has invested in multiple funds then you have mention in email, the fund to which you wish to transfer and percentage or can also send scan copy of switch form.

-

Contact Centre: Submit the request by calling on our toll-free number 1800270700 (Timing: Daily, 10 am – 7 pm).

-

Website: Submit fund switch request through Customer Portal.

Follow below steps to submit the request through Customer Portal (Timing: Daily, 10 am – 7 pm).

|

Step 1 | |

|

Step 2 |

Click on – PROTECTING – Life Insurance |

|

Step 3 |

Click on – Mange My Policy - Switch Fund Option |

|

Step 4 |

Update mobile number/Registered Email ID/ Policy Number and Update Primary Life Insured Date of Birth. Click on Send OTP |

|

Step 5 |

Once customer Complete OTP process he/she will redirected to Fund Switch / Premium Redirection page. |

|

Step 6 |

Customers need to fulfill all requirement asked on page |

|

Step 7 |

On this screen it will show you the current funds with fund value and below you can enter the %age of fund where you want to do switching and click on "NEXT" |

|

Step 8 |

Submit the request once all details are mentioned. |

**Important Points:**

- In case of Investor profile change from guaranteed to self-managed fund, client must opt both “Fund Switch” and “Re – direction” option on fund switch from existing fund to new funds and re- allocation for future fund allocation.

Example:

If Fund Switch/premium redirection request is received and accepted at branch/contact centre/website before or at 3.00 pm then applicable NAV will be of the same day provided it is a business working day or else NAV of next working day is applied.

If Switch in fund/premium redirection request is received and accepted at branch/contact centre/website after 3.00 pm then applicable NAV will of the next day provided it is a business working day or else NAV of next working day is applied. Also, If the request is submitted on holidays then applicable NAV will be of next day.

Tax Benefit

Goods and Services Tax (GST), is a new Indirect Tax based on the concept of “One Nation One Tax”. It replaces the existing indirect taxes such as Service Tax, Vat, Excise Duty etc.

GST comes in applicable from 1st July 2017.

| Service Tax | Goods and Services Tax |

| Centralised Levy | State level Levy |

| Controlled by Central Government | Controlled by Central Government , State Government and Union Territories |

| Origin Based- Taxable where the service provider exists | Destination based Consumption tax- Belongs to the state where end consumer resides.s |

GST will be levied on supply of both, Goods and Services.

All present day Central and State taxes like VAT, Excise Duty, Service Tax etc will be subsumed in GST and only one tax

Explore categories