- All Insurance

- Endowment PlansNew

- Savings PlansNew

- Term InsuranceNew

- Pension PlansNew

- Critical Illness Insurance

- ULIP PlanNew

- Group Insurance

- Protection Solutions

- Employer Employee

- Voluntary

- Affinity

- Credit Life

- Retirement Solutions

- Annuity Scheme

- Gratuity

- Leave Encashment

- Post Retirement Medical Benefits Scheme

- Superannuation

- Withdrawn Products

- NRI PlansNew

- Articles

- Where Do I?

- Find Customer Service

- Learn About Life Insurance

- Become a Life Insurance Advisor

- Know Our Funds

- Manage My Claim

- Know more about UPI Autopay

- Read FAQs

- Register For One ABC Id

- Download Forms

- Read Market Outlook

- Download Public Disclosures

- Disclosure of Key Performance and Financial Parameters

- Financial Calculator

- Know your Advisor

- Term Insurance

- Manage My Policy

- Her Insurance

Aditya Birla Sun Life Insurance Company Limited

Aditya Birla Sun Life Insurance Company Limited

Outlook for the Month of August’26

Economy Review

The key events in the month were –

- Domestic Factors –

a) IIP – IIP growth accelerated further in June’26, with growth rate at 7.3% YoY vs. 5.0% in May’26, driven by broad-based strength in manufacturing and electricity and a favorable base. Manufacturing, which accounts for 76% of the index, accelerated to 7.8% YoY from 5.2% in May’26.

b) GST collections – GST collections increased by 15.4% yoy to Rs 2.11 tn in July’25. Tax collection from domestic transactions grew 10% to ~Rs1.44 tn, while gross revenues from imports were up 29% to Rs 66,511cr.

c) IMD – Monsoon activity has seen a pickup with the deficit falling to 12% as on 3rd Aug’26. Region-wise, East & Northeast India (-29%), Northwest India (-13%) and South Peninsula (-19%) remained deficient, while Central India (+4%) turned surplus. Kharif sowing as on July end was down 2.9% YoY.

d) Manufacturing PMI – Manufacturing PMI remains firmly in the expansion territory although it has moderated to 53.5 in Jul’26 vs. 54.2 in Jun’26.

e) Trade Deficit – India’s trade deficit stood at $30.1 bn in Jun’26 vs. $28.2 bn in May’26, which was led by higher oil prices. Imports rose 31% yoy in Jun’26 whereas exports rose by 15.5% YoY.

- Global Factors –

a) FOMC – The FOMC kept the Federal Funds rate unchanged but was divided with a 9-3 vote on a pause versus a hike.

b) AI Stocks – Global AI stocks saw a sharp drawdown amid margin unwinding, even as US tech giants re-affirmed/increased their capex guidance.

c) West Asia Conflict – The USA President has said that talks would soon happen with Iran for re-opening the Strait of Hormuz although Iran’s foreign ministry has denied any ongoing negotiations.

b) Crude Oil – Brent crude oil prices continue to remain volatile and stood at $85/bbl. Prices have seen correction from peak level of $100/bbl during Jul’26.

Domestic Macro Economic Data

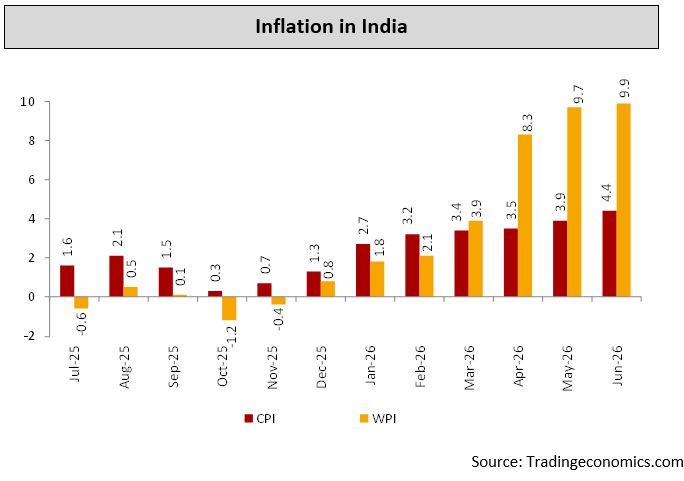

Inflation – India’s CPI inflation inched up to 4.4% in June’26 Vs 3.9% in May 2026 driven by higher food and transport inflation. India’s WPI inflation continues to remain elevated at 9.9% in June’26.

Outlook for Equities

Indian equity markets gained 1.6% in the month of Jul’26 as crude prices have moderated from the earlier elevated levels. Nifty Midcap-150 Index was also up 1.4% and the Nifty Smallcap-250 Index was up 1.1% during the month. Domestic market movements were driven largely by 1QFY27 earnings and commentary, as operating performance was broadly strong for the Nifty-50 Index.

Brent crude oil prices have seen correction from peak level of $100/bbl during Jul’26, and currently are trading at $85/bbl. Monsoon activity has seen a pickup with the deficit improving to 12% as on 3rd Aug’26. Region-wise, East & Northeast India, Northwest India and South Peninsula remained deficient, while Central India turned surplus. India’s trade deficit stood at $30.1 bn in Jun’26 vs. $28.2 bn in May’26, which was led by higher oil imports. Global equity markets have seen reversal of the AI trade, with sharp selloffs seen in Korea (-18%) and Taiwan (-12%) while Germany (+3.6%), the UK (+3.3%) and India (+3.1%) outperformed on a USD basis. FIIs bought $2.3bn worth of Indian equities whereas DIIs bought $3.7bn of equities during the month of Jul’26.

Nifty is currently trading at ~17x FY28e P/E. We expect Nifty earnings to grow at 13-15% CAGR over FY26-28. We expect rerating in the Indian equity markets given correction in crude oil prices and improving macros. This can lead to strengthening of the rupee and increase in foreign capital inflow. Investors can continue to invest in equities from a medium to long-term perspective.

Outlook for Debt

Monsoon has progressed and till July 31 cumulative rainfall was 13% below long-term average while weekly rainfall was 2% below long-term average. On a cumulative basis, rainfall was deficient in east, north east and south India while rainfall was normal in central and north-west India. Overall rainfall in June was 40% below long-term average, while in July it was 3.5% above long-term average. El Nino conditions have strengthened and neutral IOD conditions continue to prevail. As of July 24, the total kharif acreage was 4.7% lower than the same period last year. Rice sowing was 2.6% lower while pulses acreage was 7.5% lower than last year. Overall basins and reservoirs levels were 7% below long-term average for week ending July 30.

Bloomberg deferred the inclusion of Indian bonds in the Global Aggregate Bond Index which was anticipated by the markets. Robust flows materialized from RBI’s FX swap measures to the extent of US$40.8 bn till July end. Durable liquidity surplus improved to around Rs5.4 tn as of July 15, 2026. Government cash balances increased to Rs4.3 tn. Banking system liquidity surplus improved amid flows from RBI’s measures, month-end government spending and G-Sec buybacks. RBI’s FX intervention to curb the pressure on rupee and CRR product buildup offset part of the surplus.

June CPI inflation continued on the uptrend at 4.4% yoy. Food inflation was driven by oils and fats, meat and fish, fruits and vegetables. Core inflation was at 3.9% yoy. WPI inflation for June was at 9.9% yoy led by fuel and power inflation at 27.4% yoy. IIP growth in June was at 7.3% led by electricity production growth at 10.6%. In terms of the use-based classification, growth was led by capital goods. India’s goods trade deficit widened to US$30.4 bn in June as imports rose 31% yoy in June. The services trade surplus in June at US$15.1 bn fell as compared to the significantly downward revised print of US$15.7 bn in May.

The FOMC kept its policy rate unchanged at 3.5-3.75%, with three dissenters voting for 25 bp of rate hike. Prior to the July FOMC, markets were fully pricing 50bps of rate hike. This has shifted to one rate hike, as the Fed Chair failed to provide market guidance. The consequent market reaction has been a US yield curve steepening with 2Y yields down 10 bps while the 10Y and 30Y yield moved up by 5bps and 11bps respectively following the FOMC meeting. The Bank of England kept the Bank Rate unchanged at 3.75%, with three out of the nine members voting against the decisions, favoring a 25bp hike. The Bank of Japan left its benchmark rate unchanged at 1.0%, with one of the eight members dissenting in favor of a rate hike. The BOJ warned that inflation is likely to exceed its target range in second half of the financial year. This status quo decision was followed by BOJ’s coordinated move with the US of aggressive FX intervention to curb the losses in JPY. JPY is trading ~4.5% stronger against the US Dollar from the lows of ~164 levels.

In the near term, markets await RBI monetary policy review, path of CPI data, FPI flows and currency movement. Globally, labour market data from US, inflation data and global yields will be observed. 10-year Gsec closed at 6.84% on July 31, 2026, higher by 9 bps during the month. 10-year Gsec yield in the near term is likely to be in a range of 6.70%-6.90%. Spread of 10-year Gsec with corporate bond is near 50 bps and is likely to be in a range of 45-55 bps.