- All Insurance

- Endowment PlansNew

- Savings PlansNew

- Term InsuranceNew

- Pension PlansNew

- Critical Illness Insurance

- ULIP PlanNew

- Group Insurance

- Protection Solutions

- Employer Employee

- Voluntary

- Affinity

- Credit Life

- Retirement Solutions

- Annuity Scheme

- Gratuity

- Leave Encashment

- Post Retirement Medical Benefits Scheme

- Superannuation

- Withdrawn Products

- NRI PlansNew

- Articles

- Where Do I?

- Term Insurance

- Manage My Policy

- Her Insurance

Connect

Aditya Birla Sun Life Insurance Company Limited

Aditya Birla Sun Life Insurance Company Limited

ABSLI Platinum Gain Plan

IN THIS POLICY, THE INVESTMENT RISK IN INVESTMENT PORTFOLIO IS BORNE BY THE POLICYHOLDER

Wealth Boosters & Loyalty Additions

Life Cover

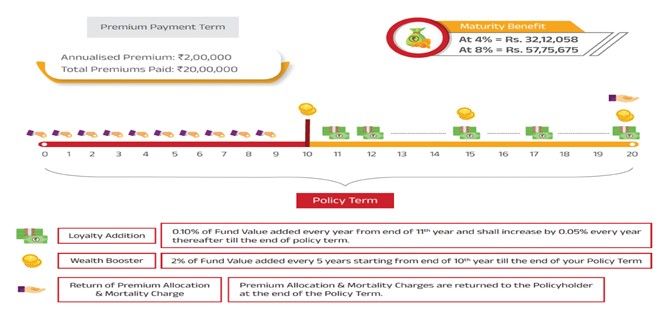

Give ₹ 2 lakhs/ year for 10 years Get ₹ 32.12 lakhs @ 4% or ₹ 57.76 lakhs @ 8% at maturity1.

Why Buy ABSLI Platinum Gain Plan?

Key Features

Choice of 3 Premium Bands

Choice of Sum Assured Multiple – 7X and 10X

Wealth Boosters and Loyalty Additions added periodically to enhance the Fund Value

Choice of 5 investment strategies and 20 funds to suit your varied investment needs.

Benefits Of ABSLI Platinum Gain Plan

Death Benefit

In case of Death of the Life Insured anytime during the Policy Term, while all due premiums under the policy have been paid, the nominee/legal heir/Policyholder will be paid the higher of:

Maturity Benefit

On survival of Life Insured up to the end of the Policy Term and provided all due premiums under the policy have been paid or is a Reduced Paid-Up Policy, We shall pay the Fund Value in a lump sum to the customer or as a structured payout using Settlement Option.

Riders

Get Added Protection and Enhance Your Plan by Opting For Riders at a Nominal Cost

ABSLI Comprehensive Critical Illness Rider

(UIN: 109A041V01)

In the unfortunate event that the life insured is diagnosed to be suffering from critical illnesses as mentioned in the Rider prospectus, as per the variant, rider Sum Assured is paid in lumpsum as per the conditions mentioned in the rider prospectus.

How Does ABSLI Platinum Gain Plan Work?

Use Case 1

Use Case 2

In case the Life Insured Survives till the end of the Policy Maturity:

Mr. Sharma aged 35 years purchases ABSLI Platinum Gain Plan with Annualized Premium: Rs. 2,00,000 with premium payment mode: Annual.

He chooses Premium Payment Term: 10 years and Policy Term: 20 years

Investment Option: Self-Managed Option, Fund Chosen: Maximizer, Sum Assured Multiple: 10X, Sum Assured: Rs. 20,00,000.

Mr. Sharma survives the entire policy term.

Plan Finances For Your Life Goals

Buy ABSLI Platinum Gain Plan Now.

| Product Specifications | |||||||||

| Type of Plan | A Unit-Linked Non-Participating Individual Life Insurance Savings Plan | ||||||||

| Coverage | All Individuals (Male | Female | Transgender) | ||||||||

| Minimum Entry Age (age as on last birthday) | 30 days* | ||||||||

| Minimum Maturity Age (age as on last birthday) | 18 years | ||||||||

| Maximum Entry Age (age as on last birthday) | 65 years | ||||||||

| Maximum Maturity Age (age as on last birthday) | 85 years | ||||||||

| Minimum Premium | Rs. 2,00,000 | ||||||||

| Maximum Premium | No Limit (subject to Board Approved Underwriting Policy) | ||||||||

| Minimum Sum Assured | Rs. 14,00,000 | ||||||||

| Maximum Sum Assured | No Limit (subject to Board Approved Underwriting Policy) | ||||||||

| Premium Paying Term (PPT) | Limited Pay: 5 to 12 years Regular Pay: 10 to 20 years | ||||||||

| Minimum Policy Term | For Regular Pay & 5 to 9 Pay : 10 years For 10 Pay: 11 Years For 11 Pay: 12 Years For 12 Pay: 13 Years | ||||||||

| Maximum Policy Term | 20 years | ||||||||

| Premium Payment Mode | Annual | Semi-Annual | Quarterly | Monthly | ||||||||

| Premium Bands |

| ||||||||

*risk commences from the policy issue date

How To Claim Online?

3 quick, everything online

1

Fill basic details

2

Claim intimation

3

Document submission

Frequently Asked Questions

Know more about ABSLI Platinum Gain Plan in detail here:

ABSLI Platinum Gain Plan is a unit linked, non-participating insurance plan is an exclusive product for HNI customers which combines protection and market linked return into a simple and flexible solution and provides a wide range of flexibility. Further the customers can choose from a combination of 5 investment strategies along with 20 funds (2 new fund offerings) giving you complete control over your savings.

Policy premiums can be paid annually, semi-annually, quarterly or monthly. Premiums can be paid by cheque, credit card, demand draft, ECS or salary deduction (monthly mode only). For monthly mode, minimum two months premium is required upfront. ECS includes standing instruction, direct debit and other automated payment modes.

For Regular Pay & Limited Pay options, Sum Assured multiple allowed is 7 times or 10 times the Annualized Premium is allowed under the plan. If the Sum Assured chosen is 7/10 times the Annualized Premium, the death benefit after partial withdrawals shall never be less than Annualized Premium multiplied by 7/10. The minimum Sum Assured allowed under this plan is Rs. 14,00,000. There is no maximum Sum Assured limit subject to Board Approved Underwriting Policy.

Yes, Policyholder will have the flexibility to increase or decrease the Premium Payment Term provided the policy is in-force for full Sum Assured and such increase or decrease is subject to boundary conditions of the product. Policyholder can exercise this option only after Annualized Premiums for first five policy years are paid in full

Example: Mr. Raheja opts for ABSLI Platinum Gain Plan with Policy term of 20 years and Premium paying term of 12 years & chooses Smart Investment Option. His annual premium is Rs. 5,00,000 and premium due date is 1st of Jan every year. Mr. Raheja in the 6th Policy year i.e. after paying 6 premiums realizes he won’t be able to pay the all 12 premiums due to financial instability (since his PPT is 12 years). He chooses to decrease his premium payment term to 8 years by opting for the Increase/Decrease in Premium Payment Term feature.

The Return Optimiser option enables to take advantage of the equity market at the same time protect gains from the future market volatility and creates a more stable sequencing of investment returns.

This investment strategy safeguards the returns earned on investments by shifting the returns to a more conservative fund. Thus the return on investment is safeguarded from price volatility in the equity market.

Under this option all your Annualized Premium (net of premium allocation charges) are invested in the Maximiser fund. The Maximiser fund will be tracked every day for each policyholder for a pre-determined upside movement of 10% or more over the net invested amount (net of all charges). When the gain from the Maximiser fund reaches 10% or more of the net invested amount, the amount equal to the appreciation will be transferred to the Income Advantage fund at the prevailing unit price. This ensures that gains are protected from any future market volatilities. Where the gain is less than the pre-determined upside movement of 10%, the fund value will continue to remain in the Maximiser fund and no transfers will be made to the Income Advantage fund.

Example Suppose Mr. Raheja aged 30 years opts for Milestone Variant with the Return Optimiser option strategy. He invests premium of Rs. 2,00,000 and Policy Term of 20 years. At the end of the third policy year,

| Total Premiums Paid (invested in Maximiser Fund) | Rs. 6,00,000 |

| Less charges deducted from Maximiser Fund (Premium Allocation Charge, Mortality Charge and GST) | Rs. 87,442 |

| Net amount lying in the Maximiser Fund (after FMC charges) | Rs. 5,12,558 |

Suppose the Fund Value is now Rs. 5,64,000 which is higher than 5,63,813 (i.e. 110% of the net invested amount of 5,12,558) then Rs. 51,442 (i.e. 5,64,000 – 5,12,558) will be transferred to Income Advantage Fund. If the Fund Value is less than Rs. 5,64,000 then there will be no transfer to Income Advantage Fund.

1 Mr. Sharma aged 35 years purchases ABSLI Platinum Gain Plan with the following details:

Annualized Premium: Rs. 2,00,000 | Premium Payment Term: 10 years | Policy Term: 20 years | Investment Option: Self-Managed Option | Fund Chosen: Small Cap Fund | Premium Payment Mode: Annual | Sum Assured Multiple: 10X | Sum Assured: Rs. 20,00,000

These assumed rates of return are not guaranteed and they are not the upper or lower limits of what you might get back as the value of your policy is dependent on a number of factors including future investment performance.

This is a unit-linked non-participating individual life insurance savings plan.

This policy is underwritten by Aditya Birla Sun Life Insurance Company Limited (ABSLI).

Linked Life insurance products are different from the traditional life insurance products and are subject to the risk factors.

Linked Insurance Products do not offer any liquidity during the first five years of the contract. The policyholder will not be able to withdraw/surrender the monies invested in Linked Insurance Products completely or partially till the end of the fifth year from inception.

Aditya Birla Sun Life Insurance and ABSLI Platinum Gain Plan are only the names of the Company and Policy respectively and do not in any way indicate their quality, future prospects or returns.

The name of the funds offered in this plan does not in any indicate their quality, future prospects or returns.

The value of the fund reflects the value of the underlying investments. These investments are subject to market risks and change in fundamentals such as tax rates etc affecting the investment portfolio. Please know the associated risks and the applicable charges, from your Insurance agent or the Intermediary or policy document.

The premium paid in unit linked life insurance policies are subject to investment risk associated with equity markets and the unit price of the units may go up or down based on the performance of fund and factors influencing the capital market and the policyholder is responsible for his/her decisions.

Past performance of the Unit Linked fund of the company is not necessarily indicative of the future performance of any of these Unit linked fund(s).

An extra premium may be charged as per our then existing underwriting guidelines for substandard lives, smokers or people having hazardous occupations etc.

This prospectus contains only the salient features of the plan. For further details, please refer to the policy contract.

This product shall also be available for sales through online channel.

In the Unit Linked Policy, the investment risk in the investment portfolio is borne by the Policyholder.

Tax benefits may be available as per prevailing tax laws. For more details and clarification call your ABSLI Insurance Advisor or visit our website and see how we can help in making your dreams come true.

“We”, “Us”, “Our” or “the Company” or “ABSLI” means Aditya Birla Sun Life Insurance Company Limited.

“You” or “Your” means the Policyholder.

Policyholder and Life Insured can be different under this product.

For other terms and conditions, request your Agent Advisor or intermediaries for giving a detailed presentation of the product before concluding the sale. Should you need any further information from us, please contact us on the below mentioned address and numbers.

UIN: 109L142V01