- All Insurance

- Endowment PlansNew

- Savings PlansNew

- Term InsuranceNew

- Pension PlansNew

- Critical Illness Insurance

- ULIP PlanNew

- Group Insurance

- Protection Solutions

- Employer Employee

- Voluntary

- Affinity

- Credit Life

- Retirement Solutions

- Annuity Scheme

- Gratuity

- Leave Encashment

- Post Retirement Medical Benefits Scheme

- Superannuation

- Withdrawn Products

- NRI PlansNew

- Articles

- Where Do I?

- Term Insurance

- Manage My Policy

- Her Insurance

Connect

Aditya Birla Sun Life Insurance Company Limited

Aditya Birla Sun Life Insurance Company Limited

ABSLI Nishchit Pension Plan

A non-linked, non-participating individual pension plan!

Fully Guaranteed# Corpus

Life Insurance Cover

Pay ₹1 lac1 for 5 years and

Get ₹19.35 lakhs after 25 years.

Why buy ABSLI Nishchit Pension Plan?

Key Features

Fully guaranteed# corpus accumulated on your retirement helping you secure a regular income for your golden years.

Guaranteed# Additions accrued periodically during the Policy Term to build your retirement corpus.

Loyalty Addition added at the end of the Policy Term to further boost your retirement corpus, provided all due premiums paid.

Build your own plan by choosing between varied Premium Payment Terms – invest for the entire Policy Term or for a limited period to suit your requirements.

Life Insurance Cover to offer financial protection for your loved ones, equal to total premiums paid accumulated at a fixed percentage during the Policy Term

Flexibility to defer your Vesting Benefit by up to 10 years to ensure your retirement planning always stays aligned with your life goals.

Benefits of ABSLI Nishchit Pension Plan

Make yourself future ready and receive regular income with ABSLI Nishchit Pension Plan.

Death Benefit

In the event of death of the Life Insured during the Policy Term and provided that the Policy is In-force, the Death Benefit will be payable to the Nominee(s)/Legal heir(s). Nomination can only be effected if the Policyholder and Life Insured are the same.

Guaranteed Additions

Guaranteed Additions are defined as a fixed percentage of Total Premiums Payable which get accrued into your policy as per terms and conditions given below:

Check your Eligibility

|

Product Specifications | ||||||||||||||||

|

Type of Plan |

A Non-Linked Non-Participating Individual Pension Plan | |||||||||||||||

|

Coverage |

All Individuals (Male | Female | Transgender) | |||||||||||||||

|

Premium Payment Term (PPT) & Policy Term (PT)

|

The Premium Payment Term and Policy Term can only be chosen at Policy inception and cannot be changed thereafter.

| |||||||||||||||

|

Age of the Life Insured at Entry (Age as on last birthday) |

Minimum |

30 years | ||||||||||||||

|

Maximum |

65 years | |||||||||||||||

|

Vesting Age of the Life Insured (Age as on last birthday) |

Minimum |

45 years | ||||||||||||||

|

Maximum |

75 years | |||||||||||||||

|

Minimum Annualized Premium |

Rs. 20,000 | |||||||||||||||

|

Maximum Annualized Premium |

No Limit (subject to Board Approved Underwriting Policy) | |||||||||||||||

|

Premium Payment Frequency and Frequency Loadings |

| |||||||||||||||

|

Premium Bands |

The benefits under this product vary by premium bands as mentioned below:

| |||||||||||||||

How does ABSLI Nishchit Pension Plan work for you?

Use Case 1

Use Case 2

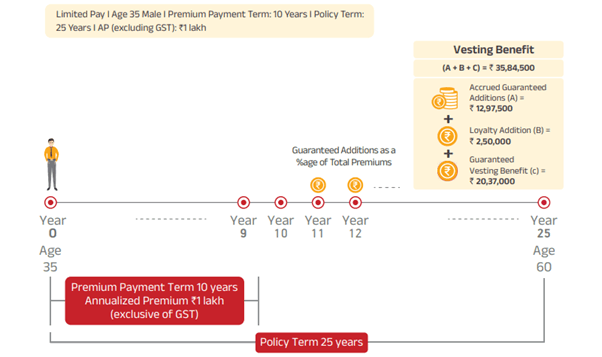

Mr. Khanna, aged 35 years, works in XYZ Ltd invests Rs. 100,000 (excluding GST) in ABSLI Nishchit Pension Plan

He chooses Vesting Age - 60 years, Policy Term - 25 years, Premium Paying Term - 10 years, Premium Payment Mode: Annual

Mr. Khanna survives through the Policy Term and receives the Vesting Benefit as follows:

Mr. Khanna will have the option to utilize his Vesting Benefit basis the options given in the ‘Vesting Benefit’ section above.

Enjoy a lumpsum corpus and regular income in your golden years

Invest in ABSLI Nishchit Pension Plan

How to initiate Claim?

3 quick steps, everything online.

1

Fill basic details

2

Claim intimation

3

Document submission

FAQs on Nishchit Pension Plan

ABSLI Nishchit Pension Plan is a non-linked non-participating individual pension plan, that helps you accumulate a guaranteed# corpus for your retirement along with a life insurance cover. This lump sum corpus allows you to secure an uninterrupted income throughout your golden years.

Key features of ABSLI Nishchit Pension Plan are:

- Fully guaranteed# corpus accumulated on your retirement helping you secure a regular income for your golden years.

- Guaranteed Additions during the Policy Term to build your retirement corpus.

- Loyalty Addition added at the end of the Policy Term to further boost your retirement corpus, provided all due premiums have been paid.

- Build your own plan by choosing between varied Premium Payment Terms – invest for the entire policy term or for a limited period to suit your requirements.

- Life Insurance Cover to offer financial protection for your loved ones, equal to total premiums paid accumulated at a fixed percentage during the Policy Term.

- Flexibility to defer your Vesting Benefit by up to 10 years to ensure your retirement planning always stays aligned with your life goals.

ABSLI Nishchit Pension Plan offers a Policy Term for a period of 10 years to 35 years.

The minimum annualized premium is Rs. 20,000 for all PPTs.

The premium amount chosen will be payable every year throughout the premium paying term.

Yes, higher vesting benefit is available if you pay a higher premium. The premium bands are as mentioned below:

|

Annualized Premium (Rs.) |

Band 1 |

Band 2 |

Band 3 |

Band 4 |

Band 5 |

Band 6 |

|

20,000 to 49,999 |

50,000 to |

100,000 to 199,999 |

200,000 to 499,999 |

500,000 to 24,99,999 |

25,00,000 & above |

Our life insurance policies cover COVID -19 claims under life insurance claims, subject to applicable terms & conditions of policy contract and extant regulatory framework

#Provided all due premiums are paid.

* Tax benefits are subject to changes in tax laws. Kindly consult your financial advisor for more details.

1 Policy holder, aged 35 years invests Rs. 100,000 (excluding GST) in ABSLI Nishchit Pension Plan. He chooses Vesting Age - 60 years, Policy Term - 25 years, Premium Paying Term - 5 years, Premium Payment Mode: Annual

- This policy is underwritten by Aditya Birla Sun Life Insurance Company Limited (ABSLI).

- This is a non-linked non-participating individual pension plan. All terms & conditions are guaranteed throughout the policy term

- GST and any other applicable taxes will be added (extra) to Your premium and levied as per extant tax laws.

- An extra premium may be charged as per our then existing underwriting guidelines for substandard lives, smokers or people having hazardous occupations etc.

- This prospectus contains only the salient features of the plan. It does not purport to be a contract of insurance and does not in any way create any rights and/or obligations. All the benefits are payable subject to the terms and conditions of the Policy.

- This product shall also be available for sales through online channel.

- All policy benefits are subject to policy being In-force.

- “We” or “Us” or “Our” or “Company” or “ABSLI” means Aditya Birla Sun Life Insurance Company Limited.

- “You” or “Your” or “Policyholder” means the Policyholder.

- Policyholder and Life Insured can be different under this product. In all situations, it is ensured that the Policyholder has an insurable interest in the Life Insured.

For other terms and conditions, request your Agent Advisor or intermediaries for giving a detailed presentation of the product before concluding the sale. Should you need any further information from us, please contact us on the below mentioned address and numbers. (UIN : 109N151V04)

ADV/7/25-26/766