- All Insurance

- Endowment PlansNew

- Savings PlansNew

- Term InsuranceNew

- Pension PlansNew

- Critical Illness Insurance

- ULIP PlanNew

- Group Insurance

- Protection Solutions

- Employer Employee

- Voluntary

- Affinity

- Credit Life

- Retirement Solutions

- Annuity Scheme

- Gratuity

- Leave Encashment

- Post Retirement Medical Benefits Scheme

- Superannuation

- Withdrawn Products

- NRI PlansNew

- Articles

- Where Do I?

- Term Insurance

- Manage My Policy

- Her Insurance

Connect

Aditya Birla Sun Life Insurance Company Limited

Aditya Birla Sun Life Insurance Company Limited

ABSLI DigiShield Plan

Think Term Plan. Smart Financial Security For Loved Ones

Covid-19 covered

10 Plan Options

Buy ₹1 Crore Term Insurance @ ₹575/month1

Why Buy ABSLI DigiShield Plan?

Key Features

Not 1 but 10 plan options to choose from. Opting for the most suitable option based on coverage needs has never been so easy.

This Comprehensive Term Insurance Plan covers policyholders till 100 years of age.

Flexible death benefit payouts as a monthly, lump sum or both.

Option to avail monthly income for a worry-free retired life. Survival benefit for policyholders to ensure financial security after 60 years of age.

Benefits Of ABSLI DigiShield Plan

A quick, simple, stress-free way to assure financial security for the family in case of policyholder’s unfortunate demise.

Death Benefit

This is the cushion for those who depend on you financially. In case of policyholder’s death during the policy term, we care to pay the death benefits to the nominee(s) or legal heir(s) a lump sum or monthly income according to the plan option.

Terminal Illness Benefit

We wish you to always stay healthy! But in case a terminal illness is diagnosed when you are below 80 years, the policy will immediately pay you 50% of the applicable sum assured up to Rs. 2 Cr. All future premiums will be waived off, provided the policy is in force.

Plan Options

10 plan options of ABSLI DigiShield Plan. A wide range of options to suit different needs.

Level Cover Option

Option 1

This option pays the nominee the sum assured in lump-sum in case of the unfortunate death of the life insured during the policy term, provided all the premiums are paid. You will have to choose the nominee, sum assured, policy term, premium payment term and mode of payment during the inception of the policy.

Increasing Cover Option

Option 2

Under this term insurance option, the sum assured increases every year during the policy term by a simple escalation rate of 5% or 10% per annum. At the inception, you have to choose the sum assured escalation rate. In case of death of the life insured during the policy term, the nominee gets the sum assured as applicable on that date in a lump sum.

Term Plan Without Riders Is Like having Tea Without Snacks.

Riders offer additional benefits that are not included in the base policy at a nominal additional premium. There are exclusions attached to the riders. Please refer rider prospectus for more details

ABSLI Accidental Death and Disability Rider

(UIN: 109B018V03)

Get additional protection for accidents leading to death or disability at a nominal cost.

ABSLI Critical Illness Rider

(UIN: 109B019V03)

Get benefit amount as a lump sum upon diagnosis of any of the 4 specified critical illnesses.

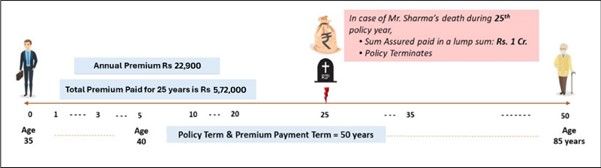

How Does The ABSLI DigiShield Plan Work?

Learn with an example. Lead by an example.

Use Case 1

Use Case 2

Mr. Sharma, 35 years old opts for ABSLI DigiShield Plan – Level Cover Option for a Sum Assured of Rs. 1 crore.

He chooses a Policy Term of 50 years and Premium Payment Term of 50 years.

Unfortunately, he dies during the 25th Policy year. His Nominee is paid a lump-sum equal to Rs. 1 crore and the Policy terminates.

At the inception of the policy, the policyholder has the freedom to choose the sum assured, policy term, premium payment term, and mode of premium payment. The maximum maturity age allowed is 85 years.

Eligibility Criteria For ABSLI DigiShield Plan

|

Coverage |

Minimum Entry Age |

Maximum Entry Age |

Premium Payment Terms |

Minimum Policy Term |

Maximum Policy Term |

Premium Payment Mode |

Minimum Maturity Age |

Maximum Maturity Age |

Sum Assured Limits |

|

Male | Female | Transgender |

18 years |

65 years |

Regular Pay |

10 years |

55 years |

Annual | Semi- Annual | Quarterly | Monthly |

28 years |

85 years |

Min: Rs. 30 lakhs Max: No Limit, subject to Board approved Underwriting Policy |

Sure of buying a Term Plan?

Do it in less than 5 minutes.

Things We Can’t Promise Under a ABSLI DigiShield Plan.

It costs the emotions and courage of a family when the policyholder passes away. But the ABSLI DigiShield Plan does not cover the family in these circumstances.

If the policyholder was diagnosed with pre-existing diseases 36 months prior to the effective date of the policy issued by the insurer.

When the policyholder (whether medically sane or insane) suffers from self-inflicted injury or makes an attempt to suicide, no Terminal Illness Benefit will be paid.

No protection for critical illness or accidental death benefit if the death of the policyholder happens due to alcohol consumption, hazardous activity, an act of war, or child-birth.

Death of the policyholder due to lifestyle disease because that has been the choice to live.

How To Initiate Claim?

3 quick steps, everything online.

1

Fill basic details

2

Claim intimation

3

Document submission

ABSLI DigiShield Plan FAQs

We are constantly trying to simplify the ABSLI DigiShield Plan!

ABSLI Digi Shield plan is the term plan-best financial support for the family especially when the policyholder dies.

- 10 Plan Options to suit varied protection need.

- Flexibility to choose term cover as per the need. Coverage up to 100 years is available.

- Ensure financial stability for the dependents in the absence of life insured with multiple payout options - lump-sum, monthly income or a combination of both.

- Unique benefit – Receive Survival Income in a Term Plan – Guaranteed Monthly payouts post attaining Age 60 years for a stress-free retired life. -Get all your premium back with Return of Premium (ROP) option in case you outlive the policy term.

- Acceleration of base sum assured in the event of diagnosis of any Terminal Illness.

- Acceleration of Critical Illness sum assured through Accelerated Critical Illness Benefit option (ACI) where a lumpsum payout will be made to the life insured on diagnosis of any one of the covered 42 critical illness.

- Include your loved one’s in the policy with Joint Life Protection option.

- Additional protection through multiple Riders

Depending upon the smoking status of the life insured, he/she will be classified as Non-Smoker or Smoker. The proposed life insured will be classified as Non-Smoker, if he/she has not consumed tobacco products in the last 12 months. This includes any nicotine products like cigarette, cigars, chewable tobacco or any other classified stimulants.

No, Plan Option once chosen at inception; cannot be changed anytime during the Policy Term.

Retirement Age is applicable under Plan Option 3 Sum Assured Reduction Option and Plan Option 5 Whole Life Option (Sum Assured Reduction Cover). Policyholder has the option to select 60 years, 65 years, 70 years or 75 years as Retirement Age at inception, at which the Sum Assured reduces by the chosen Sum Assured Reduction Rate. The Retirement Age should be at least 10 years more than the age of the Life Insured at inception of the policy and less than the maturity age.

Income Benefit Period is applicable under Plan Option 6 Income Benefit, during which the monthly installments are paid to the Nominee after the death of the Life Insured. Policyholder has the option to select 10 years, 15 years or 20 years as Income Benefit Period at inception.

Other Insurance Plans

ABSLI Salaried Term Plan

ABSLI Salaried Term Plan is an exclusive comprehensive protection solution designed for Salaried individuals. It gives you the freedom to design your own plan that suits your protection needs.

¹ Scenario for Female, Non Smoker, Age: 21 years, Plan Option: Level Cover, Premium paying Term: Regular pay, Policy Term: 25 years, Pay Frequency: Annual, Premiums are exclusive of GST. (Annual Premium of Rs. 6900/12 months(On Average Rs.575/month) (offline premium)

This policy is underwritten by Aditya Birla Sun Life Insurance Company Limited (ABSLI). This is a non-linked non-participating individual pure risk premium life insurance plan; upon Policyholder’s selection of Plan Option 9 (Level Cover with Survival Benefit) and Plan Option 10 (Return of Premium [ROP]) this product shall be a non-linked non-participating individual life savings insurance plan. All terms & conditions are guaranteed throughout the Policy Term. GST and any other applicable taxes will be added (extra) to your premium and levied as per extant tax laws. An extra premium may be charged as per our then existing underwriting guidelines for substandard lives, smokers or people having hazardous occupations etc. For further details please refer to the Policy contract. Tax benefits are subject to changes in the tax laws. For more details and clarification call your ABSLI Insurance Advisor or visit our website and see how we can help in making your dreams come true. UIN: 109N108V13

ADV/11/24-25/2185