Extra pepperoni on your pizza, some fudge sauce and whipped cream on ice-cream sundaes, the latest Marvel character on your t-shirt, and your favourite quotes on bookmarks. You like everything in your life customised as per your taste and choice.

Similarly, you get the option of customising your Endowment Plans with a variety of add-ons, known as Riders. They aim to make your life easier and more comfortable, by ticking all the right boxes containing your needs and requirements.

In the previous article, we talked about the various customization options under an Endowment Plan. In this one, let’s have a look at the riders available!

What is a Rider?

It is an add-on benefit or extra coverage that can be added to your endowment policy by paying an additional yet reasonable premium. It ensures a more stable and wide coverage. With riders, you can safeguard yourself and your family in every way possible.

Why are Riders beneficial?

To get a rider, you don’t have to go through any extra paperwork or medical tests. The procedures you have already done for your base endowment policy suffice. So, you will be able to pick more benefits without any additional effort or hassles.

Riders save time by not having you manage another insurance policy, and can get you the benefits of many in one.

Riders save time by not having you manage another insurance policy, and can get you the benefits of many in one.

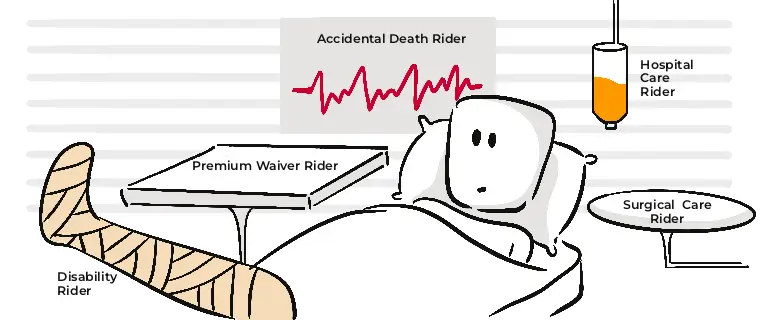

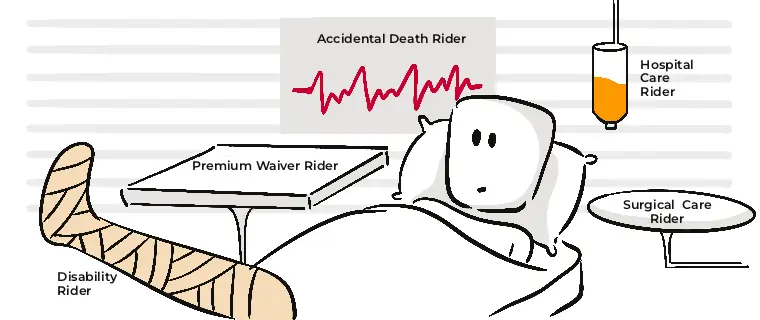

Riders available with an Endowment Plan

You can customise your endowment plan with the following riders -

1. Accidental Death Benefit Rider

It provides the sum assured and an additional rider benefit amount to your nominee, if you unfortunately pass away due to an accident during the policy term. Please note that the death should happen within 180 days of the accident for this rider to come into effect.

2. Accidental Disability Rider

An accidental disability can disrupt your whole lifestyle and financial status. In that situation, you will not be able to earn a living for yourself and your family. This rider will provide an additional sum of money, in case you meet with an accident that leads to disability.

Please note that this rider might only provide cover in limited cases - like in the cases of permanent and total disabilities only.

3. Waiver of Premium Rider

This rider is of 2 types -

a. Waiver of Premium due to Disability Rider

This rider waives off all the remaining payable premiums in case you undergo injuries that lead to disability. You will not need to pay any of the future premiums, during the policy term, but can still avail the insurance cover for the rest of it.

b. Waiver of Premium due to Critical Illness Rider -

This rider works in a similar fashion. The only difference is that the premiums will be waived off only if you contract one of the listed critical illnesses. This rider will waive off all the future premiums of the Endowment Plan, as well as the attached riders for the rest of the policy duration.

4. Surgical Care Rider

If you are hospitalised for undergoing any medical surgery for a minimum period of 24 hours and actually undergo that surgery, a lump sum benefit will be paid to you. The benefit amount will depend upon whether the surgery is classified as ‘major surgery’ or ‘other surgery’ in the policy document.

This ride comes with two conditions -

- Only people aged 18 years and above can opt for it

- The policy term of the rider should not exceed the policy term of your base endowment plan

5. Critical Illness Benefit Rider

This rider provides you and your family with financial aid in case you get diagnosed with any of the illnesses mentioned in the policy. This amount can be used by your family for all the additional expenses they will have to bear as a result of the disease/condition. It also ensures them a good lifestyle despite the unfortunate circumstances.

This rider is generally of two types -

- Accelerated Critical Illness Rider:

This will pay you an advance amount out of your total base cover. Under this rider, the benefits paid can reduce the death benefit of the base policy.

- Comprehensive Critical Illness Rider:

Unlike an accelerated rider, a comprehensive rider will not affect your base cover amount. Here, the sum assured under the critical illness cover is independent of the death benefit.

Let’s take an example to understand the difference between the two types better.

Mr. Gupta and Mr. Sharma are two individuals suffering from congenital heart defects. Mr. Gupta has purchased an Endowment Plan with a cover amount of 1.5 Crores and an Accelerated Critical Illness Rider with a cover of Rs. 50 Lakhs. Mr. Sharma has purchased an Endowment Plan of the same amount (i.e. 1 Crore 50 lakhs), but with a Comprehensive Critical Illness Rider of Rs. 50 lakhs.

Now, both of them need to undergo an open heart replacement surgery, as advised by their doctors. So let’s have a look at how the riders they have chosen will work in this situation -

| Mr. Gupta - with an Accelerated Critical Illness Rider | Mr. Sharma - with a Comprehensive Critical Illness Rider |

| The insurer will pay Rs. 50 Lakhs and Mr. Gupta’s Endowment Cover will be reduced by this amount, i.e., it will be reduced to Rs. 1 Crore. | The insurer will pay Rs. 50 Lakhs for Mr. Sharma’s surgery. This rider won’t affect his Endowment Cover - it will remain the same, i.e., Rs. 1.5 Crore. |

It is generally advisable to opt for a Comprehensive Critical Illness Rider as it does not affect your base policy cover amount. This gives you the protection of insurance, while taking care of expenses associated with a listed critical illness.

6. Hospital Care Rider

If you need to get hospitalised to undergo any treatment or surgery, with this rider in place, you will receive a daily Cash Benefit to take care of your expenses. To avail the benefit under this rider, you are required to be admitted to the hospital for a minimum period of 48 hours.

For instance,

Riya has been diagnosed with bronchiectasis and is required to undergo hospitalisation for a period of 5 days. She has an active hospital care rider along with her endowment plan, which mentions that the insurer will pay Riya a sum of Rs 8,000 (as per her policy) for each day that she is hospitalised. Therefore, due to this rider in her policy, Riya will receive a total sum of Rs. 40,000, over the span of 5 days of hospitalisation.

Pros and Cons of having Riders

Everything in life has its own advantages and disadvantages. Let’s see what riders have to offer, and what they don’t -

The pros

- They give you enhanced coverage and extra benefits without you having to buy and manage multiple policies.

- They are convenient and time-saving, since you don’t have to submit any additional documents or paperwork, besides the ones you have already submitted for your endowment plan.

- They are a part of the base insurance policy, which is why you don’t need to undergo any separate medical checkups or tests, apart from those you have already undergone at the time of taking the policy.

The cons

- According to the IRDAI regulations, the premiums of a rider cannot be higher than the premium of your base insurance policy.

- There may not be a lot of options available to customise your rider.

- There is no significant cost difference between a rider and standalone covers available for the same situation.

Life is beautiful, but unpredictable. Endowment plans make sure you and your family members are financially protected, no matter what. However, different people have differing financial situations and requirements, which further affect their insurance needs as well. Riders help you customise your policy in accordance to your specific needs and wants.

Key takeaways from this chapter

Key takeaways from this chapter