Ever find yourself pondering how much of your hard-earned money you should be setting aside for investments each month? It's a common question that floats around in the minds of many, especially when trying to navigate the fine balance between living in the moment and planning for the future. Investing is like planting seeds for a garden you want to grow years down the line. But how much should you be watering these seeds monthly? Let’s embark on a journey to uncover a golden figure that aligns with your financial landscape. Ready to dive in?

How Much Should You Invest Each Month?

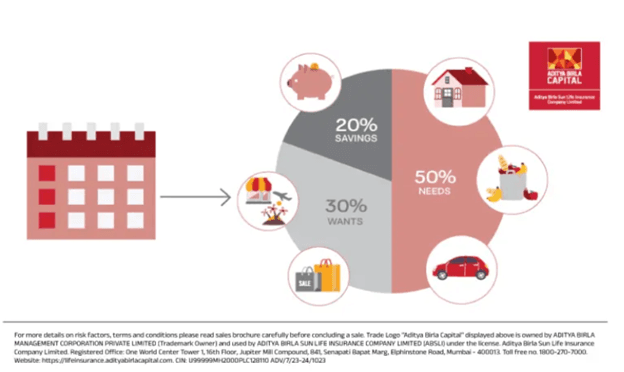

The amount you should invest each month doesn't come with a "one-size-fits-all" answer. It varies. It hinges on a mix of factors such as your financial goals, risk tolerance, and especially, your monthly income. A popular rule of thumb is the 50/30/20 budgeting rule, which suggests allocating 20% of your net income towards savings and investments. This means if you bring home ₹50,000 a month, aiming to invest about ₹10,000 could be a solid starting point.

However, life isn't always that straightforward, is it? The key is flexibility. For some, squirrelling away 20% might be a breeze, while for others, it could be a stretch. The goal should be to strike a balance that doesn't leave you strapped at the end of the month but still pushes you closer to your financial dreams.

Your Monthly Income

Your monthly income serves as the foundation of your investment plan. It's the soil from which your financial garden grows. Here’s how you can approach it:

-

Start with a Budget: Before you decide on the amount, take a good look at your monthly budget. How much are you earning, and where is your money going? Understanding your cash flow is crucial.

-

Fixed vs. Variable Income: If you have a fixed income, setting a consistent monthly investment amount is more straightforward. For those with variable incomes, consider a percentage-based approach, adjusting the amount you invest based on your earnings for the month.

-

Leave Room for Flexibility: Life throws curveballs. Some months you might find it easier to invest more, while during others, less. The idea is to keep investing something, no matter how small.

-

Increase Over Time: As your income grows, aim to increase the amount you invest. Getting a raise? Consider funnelling a portion of that extra income only into your investments.

Investing is a personal journey, influenced by your unique financial situation and goals. Whether it's ₹5,000 or ₹50,000 a month, the act of consistently setting money aside for the future is what counts. Remember, the best time to start investing was yesterday; the next best time is today. So, take a step, no matter how small, and begin your journey towards financial freedom.

Settle on Your Investing Goals

Before diving into the depths of monthly investments, it's crucial to anchor yourself to your investing goals. Are you saving for a dream vacation, your child’s education, a comfortable retirement, or maybe a down payment on a home? Each goal demands a different strategy and, likely, a different monthly investment amount. Short-term goals may require a more conservative approach, keeping funds accessible and in lower-risk vehicles. Long-term goals, on the other hand, allow you to weather the ups and downs of riskier investments, like stocks, with the potential for higher returns.

Breaking down your goals into short, medium, and long-term can help you allocate your resources more effectively. For instance, you might decide to invest ₹3,000 monthly towards a vacation fund for the next two years, while allocating ₹7,000 for long-term retirement savings. Remember, the clarity of your goals directly influences the effectiveness of your investment strategy.

Re-evaluate Periodically

The only constant in life is change, and this holds for your financial journey as well. What works today might not work tomorrow, and as such, it’s essential to re-evaluate your investment strategy periodically. This doesn’t mean you need to overhaul your plan every month but consider a check-in on your financial health and goals at least annually or after significant life events (like a new job, marriage, or the birth of a child).

During these check-ins, ask yourself:

● Have my financial goals shifted?

● Has my risk tolerance changed?

● Am I on track to meet my goals based on current investments?

● Can I afford to increase my monthly investments?

Adjustments might include increasing your monthly investment amount, diversifying your portfolio, or even changing your investment vehicles to better align with your current goals and financial situation.

Conclusion

Determining how much to invest each month is a personal decision that balances your current financial situation with your future aspirations. By setting clear goals, starting with what you can afford, and committing to regular re-evaluations, you’re laying down a path towards financial growth and security. Remember, the journey of investing is a marathon, not a sprint. It’s about consistent effort over time, adapting as you go, and keeping your eyes on the prize—your financial goals. Start where you are, use what you have, and do what you can. Your future self will thank you for the seeds you plant today.

Table of Contents

Table of Contents