1800-270-7000

1800-270-7000Aditya Birla Sun Life Insurance Company Limited

Aditya Birla Sun Life Insurance Company Limited

3 Things to Check Before Buying a Deferred Annuity Plan

Plan Smarter, Live Better!

Table of Contents

Table of Contents

How Much Helpful You Found This Article?

Thank you for your feeback

FAQs on Deferred Annuity Plan

A deferred annuity plan is an insurance product that allows you to make contributions (either lump sum or periodic payments) wherein you receiving payouts at a future date, typically during retirement.

Deferred annuities are ideal for individuals who are currently earning and want to secure a stable income for retirement, particularly those who have maxed out other tax-advantaged retirement accounts.

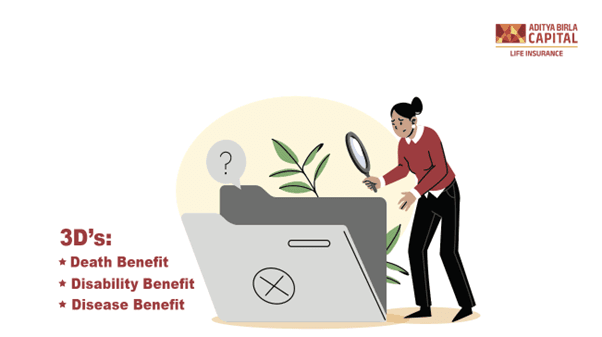

The key benefits include tax-deferred growth, a guaranteed# income stream during retirement, and potential death benefits for beneficiaries.

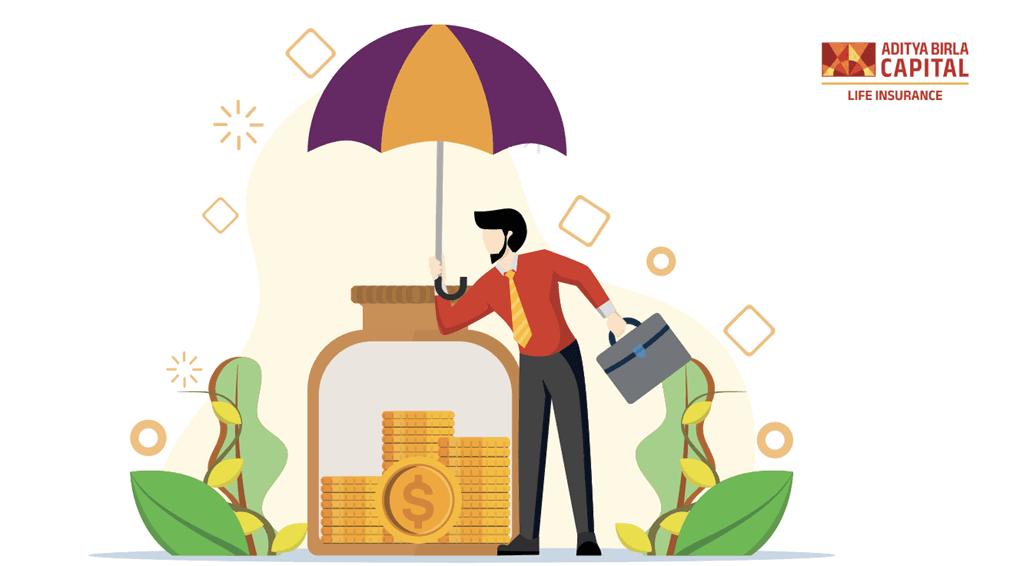

Deferred annuities may come with several fees, such as administrative fees, mortality and expense charges, and surrender charges for early withdrawals.

The money you invest grows tax-free until you start making withdrawals, at which point the earnings are taxed as ordinary income. This potentially allows the investment to grow more quickly than it might in a taxable account.

Yes, but doing so may result in surrender charges and tax penalties, especially if the withdrawal is made before the age of 60 years.

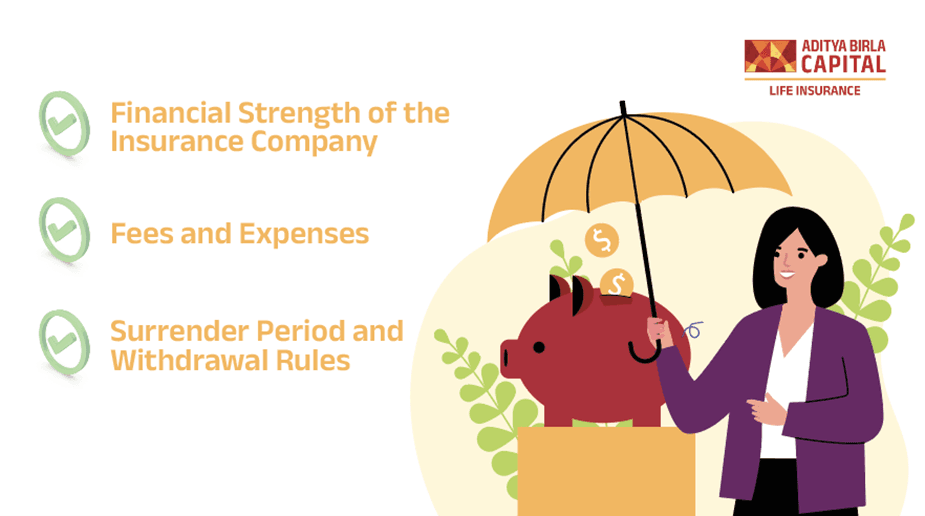

Look for an insurance company with a strong financial rating, good customer service, and a reputation for reliability, as these factors are crucial for long-term security.

Consider your financial goals, the fees involved, the flexibility of withdrawal options, and the financial strength of the insurance provider. Comparing different products and consulting with a financial advisor can also help.

Most deferred annuities come with a death benefit, which means that if you die before receiving payments, the money you've invested (and sometimes more, depending on the terms) will go to your designated beneficiaries.

Yes, risks include the fees and surrender charges that may diminish returns, the credit risk of the insurance company, and the possibility that the returns may not keep pace with inflation.

About Author

Buy ₹1 Crore Term Insurance at Just ₹576/month*

ABSLI Salaried Term Plan

Exclusively For Salaried Individuals

4 Plan Options

Life Cover upto 70 years

Optional Accelerated Critical Illness benefit

Inbuilt Terminal Illness Benefit

Life Cover

₹1 crore

Premium:

₹576/month*

Most Popular Calculator

ABSLI Salaried Term Plan (UIN:109N141V04) is a non-linked non-participating individual pure risk premium life insurance plan; upon Policyholder’s selection of Plan Option 2 (Life Cover with ROP) this product shall be a non-linked non-participating individual savings life insurance plan.

*LI Age 21, Male, Non Smoker, Option 1: Life Cover, PPT: Regular Pay, SA: ₹ 1 Cr., PT: 10 years, Annual Premium: ₹ 6400/- ( which is ₹ 576/month) Premium exclusive of GST. On death, 1 Cr SA is paid and the policy terminates.

ABSLI Guaranteed Annuity Plus Plan is a Non-Linked, Non-Participating, General Annuity Plan (UIN: 109N132V14).

^Tax benefits are subject to changes in tax laws. Kindly consult your financial advisor for more details

#Provided all due premiums are paid.

ADV/7/24-25/804

Subscribe to our Newsletter

Get the latest product updates, company news, and special offers delivered right to your inbox

Thank you for Subscribing

Stay connected for tips on insurance and investments