- All Insurance

- Endowment PlansNew

- Savings PlansNew

- Term InsuranceNew

- Pension PlansNew

- Critical Illness Insurance

- ULIP PlanNew

- Group Insurance

- Protection Solutions

- Employer Employee

- Voluntary

- Affinity

- Credit Life

- Retirement Solutions

- Annuity Scheme

- Gratuity

- Leave Encashment

- Post Retirement Medical Benefits Scheme

- Superannuation

- Withdrawn Products

- Articles

- Where Do I?

- Term Insurance

- Manage My Policy

- Her Insurance

Aditya Birla Sun Life Insurance Company Limited

Aditya Birla Sun Life Insurance Company Limited

When Should You Buy 100-year Term Insurance Plans?

Plan Smarter, Live Better!

Thank you for your details. We will reach out to you shortly.

Currently we are facing some issue. Please try after sometime.

Table of Contents

Table of Contents

The average life expectancy in India has been on the rise. Back in the 1950s, people only lived till the age of 35 or so. However, over the years, this number has seen a steady increase and today, the life expectancy stands at 69.96 years.#

Of course, this is just an average. Many people live way past the age of 69.96 - often right up to their 80s or 90s. If you have no family history of any hereditary illnesses, it's quite likely that you too may live well into old age. And who knows? You may also live to see 100 years!

Given this possibility, wouldn't you want to ensure that you are financially secure all your life? Well, if you're looking to secure your future, making the decision to buy life insurance could be one of the first big steps you can take in this direction.

But there are so many different kinds of life insurance available in the market. So, which one should you choose? If you want lifelong protection, there's only one right answer. And that is whole life insurance.

What Is Whole Life Insurance?

Whole life insurance is exactly what it sounds like. It is a kind of life insurance that provides coverage for the whole of the policyholder's life. In other words, the life cover lasts till the policyholder attains the age of 99 or 100, depending on the terms of the policy.

So, the bottom line is that if you purchase a whole life insurance plan, you remain insured throughout your life.

Primarily, there are two main kinds of whole life insurance plans you can choose from - participating whole life insurance plans and non-participating whole life insurance plans.

Participating whole life insurance plans

A participating whole life insurance plan pays you dividends. In other words, it allows you to participate in the profits of the life insurance company. These profits are generally earned from the investments made by the life insurer.

Keep in mind, however, that the dividends under a participating whole life insurance plan are not guaranteed. They are dependent on the profits and the performance of the company.

Non-participating whole life insurance plans

Non-participating whole life insurance plans do not pay out any dividends. As a result, the premiums for these plans tend to be more affordable.

How Does Whole Life Insurance Work?

Both term plans and endowment plans can offer you whole life coverage. So, depending on the kind of plan you choose, the insurer will either offer only death benefits, or both death and maturity benefits, as the case may be.

In the case of a whole life term insurance plan, the nominee will receive death benefits if the policyholder passes away before the age of 99 or 100, as applicable. However, if the policyholder survives past this age, the insurer does not make any payouts.

However, in the case of a whole life endowment plan, if the policyholder survives past the age of 99 or 100, the insurer pays out maturity benefits as guaranteed by the life insurance plan.

So, for example, let's say a policyholder has purchased a whole life insurance plan with the following parameters:

|

Particulars |

Details |

|

Age at the time of purchase |

25 years |

|

Age up to which coverage is offered |

100 years |

|

Policy term |

75 years |

|

Sum assured |

Rs. 1 crore |

Here, the policyholder's nominee will receive Rs. 1 crore if the former passes away before attaining the age of 100. This is true in the case of both term and endowment plans.

But if the policyholder survives the age of 100, they will receive maturity benefits only if the policy is an endowment plan.

What Are The Features Of Whole Life Insurance Plans?

Whole life insurance plans have several beneficial features. Before you purchase life insurance, it is important to get to know these features, so you can understand this kind of policy and make an informed decision. So, check out the main features of whole life plans below.

- Guaranteed life cover

The life cover offered by a whole life insurance plan offers guaranteed benefits to the policyholder and their family. This helps the surviving family members tide over tough times without much financial strain. - Lifelong coverage

These plans, as you have seen, offer lifelong coverage. This allows policyholders to put aside all worries about the financial security of their dependent family members, because the financial protection from these plans lasts right up to the age of 100. - Single or limited premium payment terms

Whole life insurance plans often give you the option to pay a single premium, or to pay premiums for a limited period of time. So, you can make use of this feature to pay premiums for a short period and enjoy lifelong protection in return. - Liquidity via the loan option

Whole life insurance plans also generally allow you to avail a loan against the policy. This means you have a readily available resource of accessible funds in case of any financial emergency.

When should you choose a life cover up to the age of 100? So, you now know all about how a whole life insurance plan operates. But when should you choose a life cover up to the age of 100? Let's take a closer look at the answer.

Scenario 1: You have a dependent spouse Your spouse may be dependent on you during your post-retirement phase. And while your pension or your income from any other source may be enough to sustain the two of you, your spouse could suffer financially strained in case something happened to you.

A whole life insurance plan can ensure that your spouse is well-protected financially, no matter what. Since the life cover extends till you reach 99 or 100 years of age, your spouse will always have the sum assured under the plan to fall back on.

Scenario 2: Your children are dependent on you in your senior years Before you purchase a life insurance plan, you also need to take your children into account. It helps if you can assess where they will be, financially, when you are ready to retire. If your children will likely be financially well-settled by the time you retire, a regular life insurance that gives you coverage till the age of 60 or 70 may be sufficient.

However, if you think your children may be dependent on you even in your senior years, you - and they - could benefit from a whole life plan that covers you up to the age of 100. That way, in case something untoward occurs, your children can rely on the payouts from the plan for their financial needs and life goals.

Scenario 3: You want to leave an inheritance for your family There are different ways to leave an inheritance. Some people purchase real estate properties like a residential house, others invest in gold, and yet others may leave behind bonds, stocks and other securities. All of these investments, however, take a significant amount of capital over the years. An easier way to leave an inheritance for your family is to buy a whole life insurance plan. The sum assured paid out by the plan can act as a good financial cushion for your surviving family members.

Scenario 4: You may need access to some liquid funds later in life Recall how one of the many features of whole life insurance plans is the loan against policy facility they offer? This loan can come in handy in case you face any financial emergency later in life. An unexpected illness, a sudden major vehicle or home repair, or any other big ticket expense like this could be heavy on your wallet. At such times, you can avail a loan against your whole life plan instead of breaking your investments or tapping into your savings. With a life cover up to the age of 100, you can rest assured that you have access to liquid funds all your life.

Summing Up

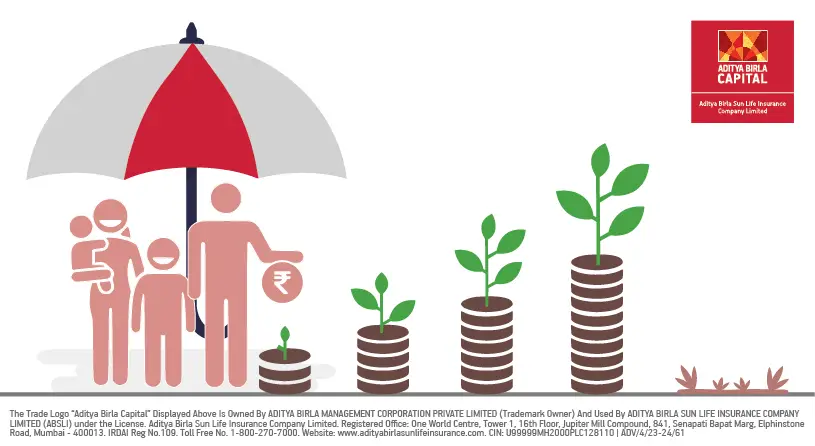

All things considered, a whole life insurance plan is an excellent way to secure your future financially. It allows you to live a worry-free life after you've retired. With additional riders, you can also enjoy other enhanced benefits from your plan throughout the policy term. So, if you think a whole life cover may be the ideal option for you, don't hesitate to take the leap and add a whole life insurance plan to your portfolio.

WHY IT'S NOT TOO EARLY TO BUY LIFE INSURANCE IN YOUR TWENTIES

A longer policy term could also mean higher premiums. But you can lock in a lower premium rate by purchasing your life cover earlier in life, in your twenties. Want to know why your twenties are not too early to buy life insurance? Our blog has all the details.

ENJOY A LIFE COVER UP TO THE AGE OF 100 + GUARANTEED REGULAR INCOME If it's whole life coverage that you need, the ABSLI Vision LifeIncome Plus Plan may just be the life insurance plan for you.

This policy gives you the option to enjoy a life cover up to the age of 100. And that's not all. You can also choose from three income payout options - short term, long term and whole life income.

Thanks for reaching out. We will reach out to you shortly.

Thanks for reaching out. Currently we are facing some issue.

Get immediate income payout after 1 day of policy issuance^

ABSLI Nishchit Aayush Plan

Guaranteed# income

Life Cover across policy term

Lumpsum Benefit at policy maturity, in addition to Income

Get :

₹33.74 lakhs~

Pay: ₹10K/month for 10 years

Recently Added Article

Most Popular Calculator

Guaranteed returns after a month¹

ADV/8/21-22/967