- All Insurance

- Endowment PlansNew

- Savings PlansNew

- Term InsuranceNew

- Pension PlansNew

- Critical Illness Insurance

- ULIP PlanNew

- Group Insurance

- Protection Solutions

- Employer Employee

- Voluntary

- Affinity

- Credit Life

- Retirement Solutions

- Annuity Scheme

- Gratuity

- Leave Encashment

- Post Retirement Medical Benefits Scheme

- Superannuation

- Withdrawn Products

- NRI PlansNew

- Articles

- Where Do I?

- Term Insurance

- Manage My Policy

- Her Insurance

Connect

Aditya Birla Sun Life Insurance Company Limited

Aditya Birla Sun Life Insurance Company Limited

7 Things To Know Before Buying an Endowment Plan

Plan Smarter, Live Better!

Table of Contents

Table of Contents

How Much Helpful You Found This Article?

Rated by 0 reader

/ 5 ( reviews )

Not helpful

Somewhat helpfull

Helpful

Good

Best

Thank you for your feeback

FAQs - 7 Things To Know Before Buying an Endowment Plan

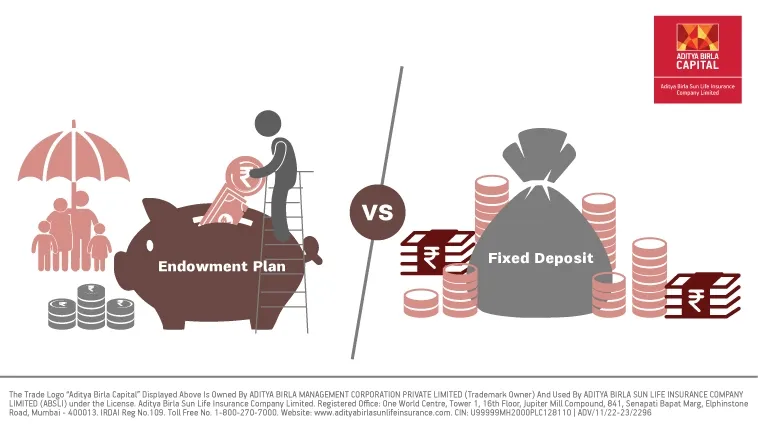

An endowment plan can be a good investment for those seeking a low-risk financial product that combines life insurance coverage with a savings component. It provides guaranteed# returns and helps in disciplined long-term savings, making it suitable for specific financial goals like retirement or children's education. However, it's important to compare the returns with other investment options and consider your risk tolerance and financial objectives.

Getting an endowment plan in your 20s is beneficial because: ● Lower Premiums: Premiums are generally lower at a younger age, making it more affordable. ● Long-Term Savings: Starting early gives you a longer time horizon to save, allowing your funds to grow and compound. ● Financial Discipline: It instils a habit of regular savings from an early age, which is crucial for long-term financial planning. ● Life Cover: Provides financial security to your loved ones in case of any unforeseen events.

Advantages:

● Guaranteed Returns: Offers guaranteed# returns at maturity, providing financial certainty.

● Life Cover: Provides life insurance coverage, ensuring financial protection for your family.

● Tax Benefits: Premiums paid and maturity benefits are eligible for tax benefits* under Sections 80C and 10(10D)1 of the Income Tax Act.

Disadvantages:

● Lower Returns: Compared to pure investment options, endowment plans may offer lower returns due to their conservative investment nature.

● Less Flexibility: Once chosen, altering the policy terms or premium payment frequency may be difficult.

● Long-Term Commitment: Requires a long-term commitment and regular premium payment to reap the full benefits.

Yes, you can have multiple endowment plans in your name. Multiple plans can help you diversify your investments and achieve different financial goals. However, ensure that the total premiums are affordable and aligned with your financial objectives.

An endowment policy is suitable for: ● Risk-Averse Investors: Those who prefer a conservative investment with guaranteed# returns. ● Long-Term Savers: Individuals looking to save for future financial goals like education, marriage, or retirement. ● Seekers of Financial Discipline: Those who need a structured savings plan to ensure regular contributions. ● Individuals Needing Life Cover: Those who want to combine life insurance coverage with savings.

Show All

Hide

Get immediate income payout after 1 day of policy issuance^

ABSLI Nishchit Aayush Plan

Guaranteed# income

Life Cover across policy term

Lumpsum Benefit at policy maturity, in addition to Income

Get :

₹33.74 lakhs~

Pay: ₹10K/month for 10 years

Recently Added Article

Most Popular Calculator

*Tax benefits are subject to changes in tax laws. Kindly consult your financial advisor for more details

1Sec 10(10D) benefit is available subject to fulfilment of conditions specified therein.

2Tax benefits may be available as per prevailing tax laws. For more details and clarification call Your ABSLI Insurance Advisor or visit our website and see how we can help in making Your dreams come true.

ADV/3/21-22/2513