There is a wide range of investments that you can choose from when you are getting started with building your portfolio. Some investments are better suited for short-term goals, while others may have a more long-term horizon. The risk associated with some instruments may be on the higher side, while others may be more low-risk.

Another major area of difference between various investment options is the nature of the returns they offer. Based on this criteria, you can choose to invest in market linked products or fixed income investments.

What are these investments though? And how do you know which one to choose? Let's find out.

What Are Fixed Income Investments?

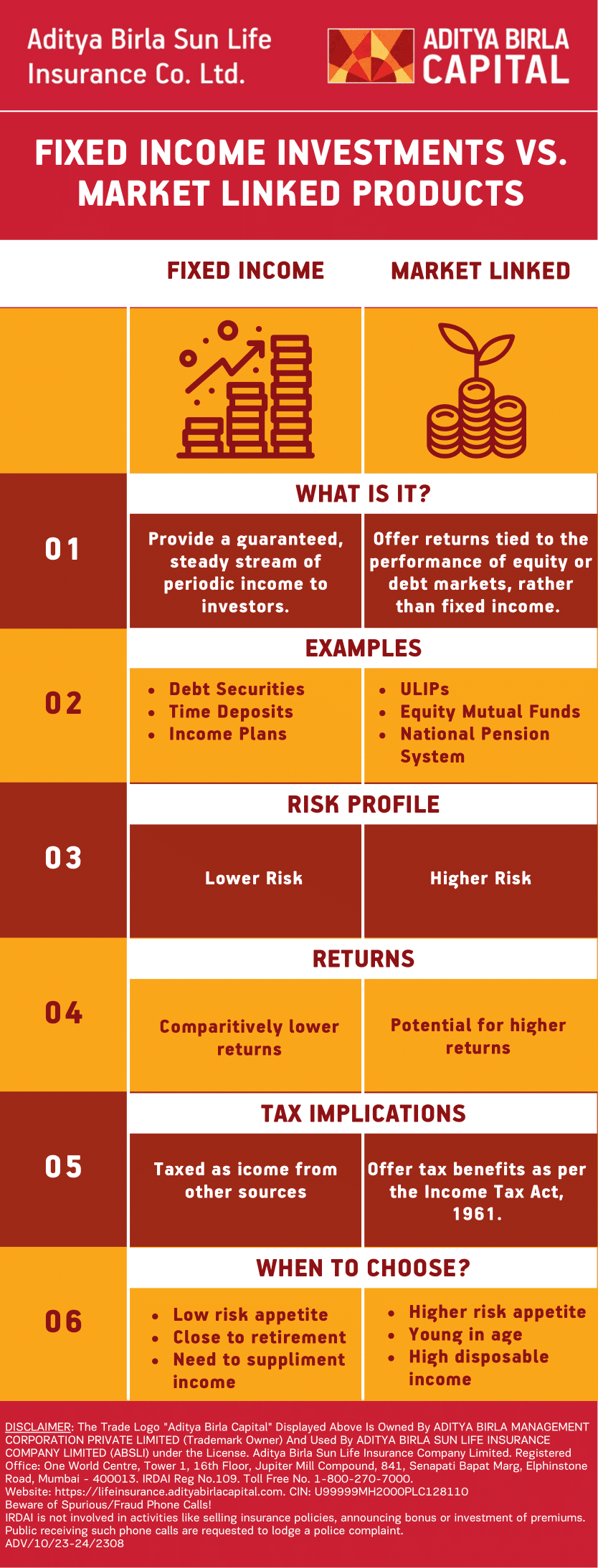

Fixed income investments, as the name indicates, are schemes or instruments that offer a steady stream of periodic income to the investor. The returns from these investments are guaranteed# and measurable. There are several different fixed income options that you can choose from for your portfolio. Here are the top choices.

-

Debt securities

Debt securities like government bonds and corporate bonds are long term fixed income investments. When you invest in these bonds, the government or the corporate entity that issued the instrument pays out interest to you at periodic intervals. The rate of interest is typically fixed.

-

Time deposits

Time deposits or fixed deposits are among the most popular fixed income options. You can deposit a specified sum with a bank or a financial institution for a predetermined period. Over that period, you earn interest at a specific rate. The interest can be paid out to you at periodic intervals, thereby acting as a source of extra income.

-

Income plans

Income plans are a kind of life insurance that give you the dual advantage of a life cover as well as periodic payouts. You need to pay premiums for a limited period, after which the insurer will pay out the income benefits periodically. This frequency can be monthly, quarterly, semi-annual or annual.

What Are Market Linked Products?

Market linked products, on the other hand, do not offer any fixed income. Again, as the name indicates, these investments give you returns that are linked with the performance of the equity or debt markets. So, if the markets perform well, the returns from these products are on the higher side. However, poor market performance brings down the returns or leads to losses.

Here are some examples of market linked products.

-

Unit Linked Insurance Plans (ULIPs)

ULIPs are life insurance plans that also offer the benefit of market linked returns. You need to pay a premium for the cover, just like in the case of other life insurance plans. However, in addition to this, you can also choose to invest in equity funds, debt funds or hybrid funds. The returns you get from these funds depend on the performance of the markets.

-

Equity mutual funds

Equity mutual funds are simply MFs that invest in a set portfolio of equity stocks. Based on the kind of stocks they invest in, equity mutual funds can be classified into different categories, such as large cap funds, mid cap funds, small cap funds and multi cap funds. There are also sectoral funds that invest in stocks of companies belonging to specific sectors.

-

National Pension System (NPS)

The NPS is an often overlooked market linked product. It is a government-backed scheme that helps investors with varying risk appetites secure their post-retirement life. By investing in NPS, you can choose to allocate your capital to debt or equity assets. These assets offer returns based on how the respective markets perform.

Fixed Income Investments Vs. Market Linked Products: A Comparison

Now that you've learned the fundamentals of fixed income investments and market linked products, let’s quickly see how they compare against one another. This way, you can make a more informed decision on which category is right for you.

-

Risk Profile

Market linked products are, by far, riskier investments than fixed income options. This is because the returns in market linked assets are neither specified nor guaranteed#.

-

Returns

In this area, market linked products have the potential to outperform fixed income instruments by a large margin. In some cases, the former can also offer inflation beating returns.

-

Tax

The earnings from fixed income investments are typically taxed as income from other sources. Market linked products like ULIPs and NPS, on the other hand, offer more tax benefits^.

So, Which One Should You Choose?

Fixed income products are better suited for investors with a low risk appetite. So, if you are inching closer to retirement, or if you have a very low tolerance or ability to take risks, these may be the ideal options for your portfolio. Keep in mind though, that the returns will be average at best.

On the other hand, market linked products are better for investors who can afford to take more risks. Younger investors and people who have some disposable funds can redirect their capital to the markets.

Conclusion

All things considered, it is a prudent idea to include both fixed income investments and market linked products in your portfolio. This way, you get the advantage of capital appreciation as well as capital preservation. You can adjust the asset allocation among these categories as you move from one age group to the next.

How to invest in equity through ulips?

If you have read the guide above and figured that market linked products are right for you, ULIPs can be the ideal choice for your portfolio. You can enjoy the benefits of a life cover. Plus, you can invest in equity through ULIPs. Want to know how? Our blog can give you all the details.

Also Read:

How Can You Grow Money With the Help of Insurance?

How Life Insurance Can Help You Earn Extra Income?

Table of Contents

Table of Contents