Imagine you wake up in the morning feeling fine but then, out of nowhere, you get an unexpected health issue. A nagging headache, a persistent cough, or perhaps an upset stomach. Health issues can be unpredictable, striking us when we least expect them. That is why having health insurance is crucial. It provides you with financial support during medical needs, ensuring that your hospital bills don't drain your savings.

However can you claim health insurance if you don’t require hospitalisation? What if you’re simply prescribed a treatment that spans a few hours and does not requires a hospital stay?

Let’s discuss - in this article!

What Is A Claim In Health Insurance?

A health insurance claim refers to the formal request you make to your insurer when you need coverage for your medical expenses. If you receive medical treatment or services covered by your insurance policy, you can submit a claim to the insurance provider, seeking reimbursement or financial coverage for the expenses incurred for your medical needs.

Types Of Health Insurance Claims

Health insurance claims are generally of two types –

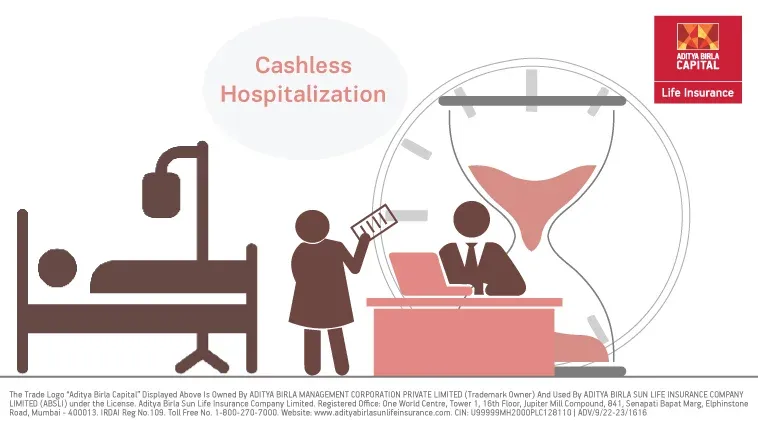

Cashless Claims

With cashless claims, the insurance company directly settles the medical bills with the hospital. For this, you must be admitted or treated at a network hospital, i.e., one that has a tie-up with your insurance company.

For example, Rakesh is having eyesight issues and consults with his doctor, who suggests cataract surgery (a part of day-care procedures). Rakesh then visits a network hospital of his insurer for the surgery. As Rakesh gets treated at a network hospital, the insurance company directly settles the surgery expenses with the hospital.

Reimbursement Claims

In reimbursement claims, you must pay the medical expenses from your pocket and later request the insurer for reimbursement. These claims can be made for treatments received at both network and non-network hospitals.

For instance, Rita met with an accident and the treatment cost her Rs. 15,000. She paid the hospital bills herself and submitted all required documents to her insurance company. After reviewing her claim and the insurer reimbursed Rs. 12,500 for the eligible expenses incurred during her hospital stay.

Can You Claim Health Insurance Without Hospitalisation?

Health insurance goes beyond just covering expenses related to hospitalisation – it provides coverage for various medical services and treatments that don’t always necessitate a hospital stay. These plans are designed to support you in times of medical need, regardless of whether you require hospitalisation or not.

Health insurance plans usually cover the following medical costs where hospitalisation isn’t necessary –

Outpatient Department

The Outpatient Department (OPD) is a hospital/medical facility section where patients can receive various healthcare services without being admitted to the hospital. It treats patients who don't need to stay overnight but still require medical attention like consultations, examinations, treatments, etc.

Health insurance plans often include coverage for diagnostic tests that are performed on an outpatient basis including blood tests, X-rays, ultrasounds, CT scans, MRIs, and other imaging procedures. However, only some insurance companies offer coverage specifically for OPD services.

Outpatient coverage can come with certain conditions and limitations, like

- Number of treatments covered

You can avail of outpatient benefits only once or twice per policy year.

- Coverage for treatments at network hospitals

You will be eligible for outpatient coverage only if you get treated at a network hospital, i.e., one that has a tie-up with your insurer.

- An upper limit on OPD coverage

There may be percentage limits or the insurer may fix a certain amount as the limit for outpatient coverage. You will not be able to make a claim for any expenses beyond this specified limit.

- Non-coverage of certain procedures

Some expenses like cosmetic dental treatments, therapy sessions with a counsellor, spectacles or other aids, etc. may not be covered.

- Geographical limitations

Your health plan may not cover OPD procedures availed of outside India.

And so on.

These conditions may vary across insurers and health insurance products. Read your policy wording carefully to be aware of the same.

Preventive Health Checkups

These are checkups that motivate you to take responsibility for your health and identify possible medical problems at an early stage. Different health insurance companies will have different terms for the frequency and extent of the covered checkups.

There can be certain conditions associated with the coverage of preventive health checkups

- Cashless service

Some insurers will allow you to claim this benefit on a cashless basis only. So, if you need to undergo any kind of health checkup, you will first have to intimate your insurer about the same and get approval for it. The expenses will be settled between the insurer and the hospital or lab where you avail of the tests - if your request is approved.

- Specific limits

Certain insurers may offer a ‘health checkup package’. Only the tests listed in the package will be covered. Some insurers may also lay down specific limits up to which health check up expenses will be covered.

- Age-related limit

Some health insurance plans may come with the condition that you can undergo health checkups only if you’re 18 years old or more. Furthermore, some family floaters may allow only adults to avail of health checkups, whereas some may allow both adults and children.

- Number of times you can use the benefit

Certain insurers may allow you to undergo health checkups only once per policy year, whereas some may not limit the same. This cap will depend on the insurer and the type of health insurance plan you own.

- Insurer’s network provider

Some insurers may cover health checkups only if you avail of them at a network hospital or lab, i.e., with whom they have a tie-up. If you get the checkup done at any other facility, you will have to bear the expenses.

- Other conditions

Insurers may also impose other miscellaneous conditions like letting you avail of health check ups only if you haven’t made any claims in the past year, etc.

And so on.

These conditions may vary across insurers and health insurance products. Read your policy wording carefully to be aware of the same.

To conclude

Health insurance is an essential tool that provides coverage for various medical treatments, even without the need for hospitalisation. It ensures that you can thus seek necessary medical care and receive financial support for treatments whether or not it mandates a hospital stay. It is the best way to get access to quality healthcare while also protecting yourself from exorbitant healthcare costs.

Table of Contents

Table of Contents