- All Insurance

- Endowment PlansNew

- Savings PlansNew

- Term InsuranceNew

- Pension PlansNew

- Critical Illness Insurance

- ULIP PlanNew

- Group Insurance

- Protection Solutions

- Employer Employee

- Voluntary

- Affinity

- Credit Life

- Retirement Solutions

- Annuity Scheme

- Gratuity

- Leave Encashment

- Post Retirement Medical Benefits Scheme

- Superannuation

- Withdrawn Products

- NRI PlansNew

- Articles

- Where Do I?

- Term Insurance

- Manage My Policy

- Her Insurance

Connect

Aditya Birla Sun Life Insurance Company Limited

Aditya Birla Sun Life Insurance Company Limited

Module 06 | Chapter 04

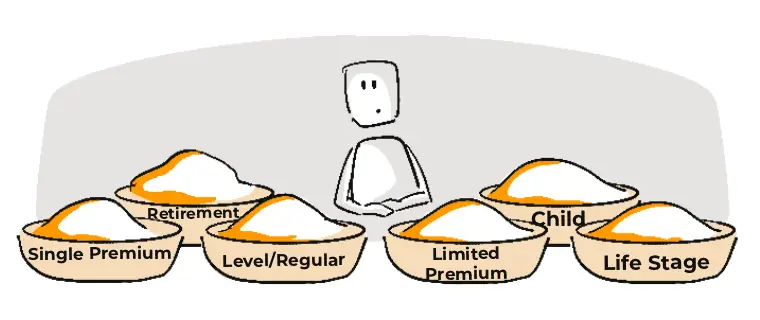

Ch. 4: Different Types Of ULIP Plans

What is ULIP PlanWhy You Should Invest in ULIP?ULIP Plan BenefitsDifferent Types of ULIP PlansConcept of Fund and NAVs in ULIPUlip Lock-In Period: Everything You Need To Know in 2023Types Of Charges In ULIPsWhat is Fund Switching and Types of Fund in ULIPKnow the Customization Options Available Under ULIP PlanRiders in ULIP PlanWhat are Exclusions & Inclusions of ULIP PlanSurrendering or Discontinuing The Ulip PlanHow to Claim ULIP Policy: Steps & Documents Required11 Things You Should Keep In Mind Before Investing In ULIP PlanWhere to Buy ULIP Plans From?

Key takeaways from this chapter

Key takeaways from this chapter

Looking to buy Ulip Plan

ABSLI Wealth Aspire Plan

Achieve your financial goals

2 plan and 4 investment option

Flexibility for partial withdrawals

Guaranteed additions1

Flexibility to add top-ups

Get:

₹3.04 lakhs @ 8% & ₹2.21 lakhs @ 4% at maturity^Give:

₹40,000 for 5 years¹ Provided all due premiums are paid.

^Age 35 Years invests in ABSLI Wealth Aspire Plan, Self Managed Investment Option, 100% in maximiser fund, Assured Plan Option, Basic annual premium: ₹40,000. Sum assured: ₹4,00,000, Premium Payment Term 5 years, Policy Term 10 years. You get ₹ 3,04 lakhs @ 8% or Rs 2,21@ 4% at maturity¹. Assumed rates of returns @4% and @8% p. a., are only illustrative scenarios at these rates after considering all applicable charges. These are not guaranteed and they are not higher or lower limits of returns. Unit Linked Life Insurance products are subject to market risks. The various funds offered under this contract are the names of the funds and do not in any way indicate the quality of these plans and their future prospects or returns. Refer to policy prospectus for more details.

ABSLI Wealth Aspire Plan is a non-participating unit linked life insurance plan. UIN:109L100V06

ADV/12/22-23/2466

Plan Smarter, Live Better!