We always have the choice of directly investing into markets.

However if you speak to any expert, they will agree that investing in dynamic capital markets is an art as well as a science. Learning the art and the science of capital market investment will require investment in another invaluable resource: “time” to learn and experience the twists and turns of the market. One needs to give significant time to study the workings, the market’s history, and keep a tab on the multiple external and internal, micro and macro variables that constantly impact it.

The alternative way to invest in the market is to rely on professional fund managers in regulated institutions like Mutual Funds or Insurance companies who pool money from small and medium investors and professionally invest and manage them on your behalf. Their aim is to achieve the goal of the specific fund you have invested in - whether is capital conservation or return maximisation.

What Are Funds In ULIP

A fund is a professionally managed pool of money collected from several investors who share a common financial goal. The funds are invested in different asset classes like equities, bonds, money market instruments, and other securities, depending on the investor’s goal, life stage, choice and risk appetite.

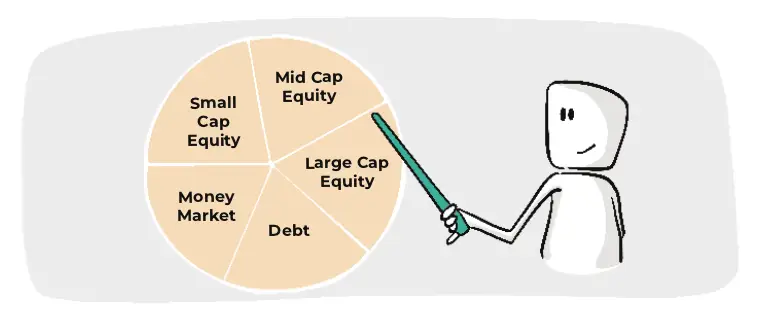

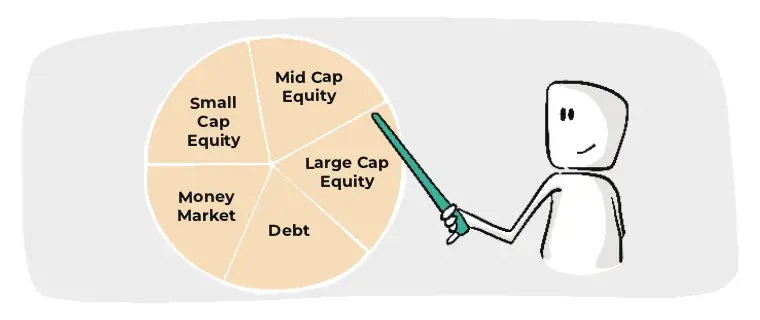

What Are The Types Of Asset Classes You Can Invest In Through a ULIP?

Following are the different asset classes that funds invest in

- Equity Instruments : Here, the premium you pay is invested in the equity or stock market. These funds offer you a really high return over an investment period. However, please note that they subject you to a higher risk, and are extremely volatile. There are three types of equity funds that you can choose from on the basis of market capitalization. Market capitalization is the value of a company on the stock market. It is calculated by multiplying the current share price with the total number of outstanding shares the company holds.

- Large Cap Funds: Invest in stocks of established and stable companies - with a large market capitalization and credible financial track record over a long period of time. It is sometimes also called Blue Chip Funds. Blue Chip Funds are a subset of Large - Cap funds.

- Mid Cap Funds: Invest in stocks of companies with a medium market capitalization - with a consistent progress graph and a good track record. They are riskier than Large Cap Funds, but can generate comparatively higher returns. Also known as emerging equity funds, because they have the potential to surpass the growth of established larger businesses.

- Small Cap Funds: Invest in stocks of companies with a small market capitalization. So, it is likely that they may become large capital businesses and deliver profitable returns. However, they are the riskiest of the lot. Even the slightest market fluctuation can have a huge impact on the share price.

-

Debt Instruments: Here, the premium is invested in debt instruments, like - corporate bonds, government securities, and other low-risk investment tools. With a lower risk, you may also get a comparatively lower return.

-

Money-Market Instruments: Invest in short-term instruments like commercial papers, bank deposits, treasury bills, etc. They are a type of debt funds and possess high liquidity. You can expect good returns. The average maturity of a money market fund is 1 year, whereas the average maturity of a debt market instrument could be longer, say 5 years. Also known as Cash Fund or Liquidity Fund.

Most popular funds:

Many funds blend two or more asset classes to offer the right balance of returns and capital protection.

Balanced Fund:

Now most ULIPs offer this “balanced fund” as a fund the customer can choose to invest in. Here the fund will invest in a combination of Debt and Equity instruments

- to provide an endeavour giving better returns than debt to the investor, a tad lower at risk than investing only in Equity. The maximum and minimum allocation in debt and equity instruments would be mentioned in the plan’s brochure or prospectus. These funds are suitable for investors who want to “balance” the risk and return - not too aggressive returns, nor too aggressive risk!

Here are few examples of funds, how they work, and who they’re a good choice for -

| Fund Name | Type | Objective | Strategy | Persona |

| Liquid Plus | Money Market Fund | Invests in short-term and top-notch money market instruments. It has a maturity of 1 year and aims towards low volatility, high safety and liquidity. | Optimise returns while trying to ensure liquidity and safety. Low risk. | 1) You prefer lower risks, or

2) You have accrued enough gains and want to invest in a liquid fund for the remainder of the policy term. |

| Assure | Debt Fund | Invests in debt funds that are top-quality and have a maturity of up to 5 years. Aims to protect your capital, while being highly safe and liquid. | Provide better returns by investing in fixed interest securities. | You don’t want to participate in equity instruments, and wish to invest in government bonds and securities. It’s a good option if you want to invest in an FD and/or are above 45 years old. |

| Creator | Balanced Fund | Invests in both high quality equity securities and debt instruments (fixed income securities) to achieve a balance between growth and stability and ensure long-term capital growth. | Investing in fixed income securities, creating a diverse equity portfolio, active fund management - for a long period. | You are okay with taking a medium level of risk to accrue good returns over a long span of time. |

| Maximiser | Equity Fund | 1) Long-term capital appreciation by investing in diverse and strong blue chip companies.

2) Aims to build a safety net against sudden instability by investing in short-term market instruments. | 1) Building a well-diverse and strong equity portfolio.

2) Maximising risk-return payoff for long-term benefits.

3) Primary investment in blue chip companies with the option of mid-cap stocks. | You can tolerate a high level of risk, especially if you’re young and/or have a disposable income. |

Note - This is just an indicative list of the types of funds. There can be more types of fund options, depending on the product you choose. Go through the product brochures and policy wordings carefully or consult with a financial advisor before making a decision!

Ok. So now you have understood what a fund is. So, let’s understand the two other important technical terms in the ULIP space - NAV and Fund Value - in a much simpler way

What Is NAV In ULIP?

So by now you know, that just like you, several other investors also invest in a ULIP. The insurer collects the money to create one large investment pool.

Now, in return for the investment made, the insurer issues an instrument, called “units” to the investor. Initially, when the insurance company is launching the fund, the units are usually issued at a standard NAV of Rs. 10.

Once the money collected is invested into a specific fund, the NAV of this fund changes every day based on the market value of the underlying investments.

How Is NAV (Net Asset Value) Calculated In ULIP?

NAV is simply the market value of a single unit on a particular day. Since it is a market value, it is calculated on each business day by calculating the market value of the total pool of investments in the fund, subtracting the expenses incurred to manage the fund and then dividing it with the number of units in the market

Confused? Here is the formula:

NAV = is the market value of a single unit issued in the fund.

NAV = (Market value of the fund - charges to manage the fund)/Total units collectively held in the market

Let’s take a simple example to understand this better

Suppose there are only two investors in a specific fund before the launch a few days ago.

Varsha has invested Rs. 50,000.

Rahul invested Rs. 20,000.

Total funds collected = Rs. 70000/-

Say the NAV of this fund is Rs. 10. Hence, the total units to be issued will be 7000. Varsha will hold 5000 units and Rahul will hold 2000 units.

Now, the money collected of Rs 70000 after the launch is invested into market instruments based on the funds strategy.

Say on Day 1, the value of the fund invested goes up to Rs 80000. Also, strictly for this example, say there are fund management charges of Rs 3000.

The NAV of the fund will now be Rs. 77000 (80K market value - 3K charges)/ 7000 (no. of units) = Rs. 11.

The fund value of the investment of the two investors will be

Varsha: 5000 units X 11 NAV = Rs. 55000

Rahul: 2000 units X 11 NAV = Rs. 22000

What Is The Fund Value In ULIP?

Fund value is nothing but the value of your investment on the particular day. It is the money you will get if you decide to redeem all the units issued on that particular day (subject to lock-in conditions of the policy, of course).

Fund value of a ULIP on a particular day is simply the NAV of that fund on that day multiplied by the number of units of the fund you hold.

Fund Value = NAV of that day X No. of Units you hold in the fund.

That’s all about funds and NAVs in ULIP.

We hope this article helped you understand the two main concepts of Unit Linked Investment Plans. You can minimise risks by choosing the fund that suits you, and generate substantial profits in the long run. Now, the next time you plan for resources to finance your life goals, we hope you consider ULIP in your book.

Key takeaways from this chapter

Key takeaways from this chapter