Aditya Birla Sun Life Insurance Company Limited

Aditya Birla Sun Life Insurance Company Limited

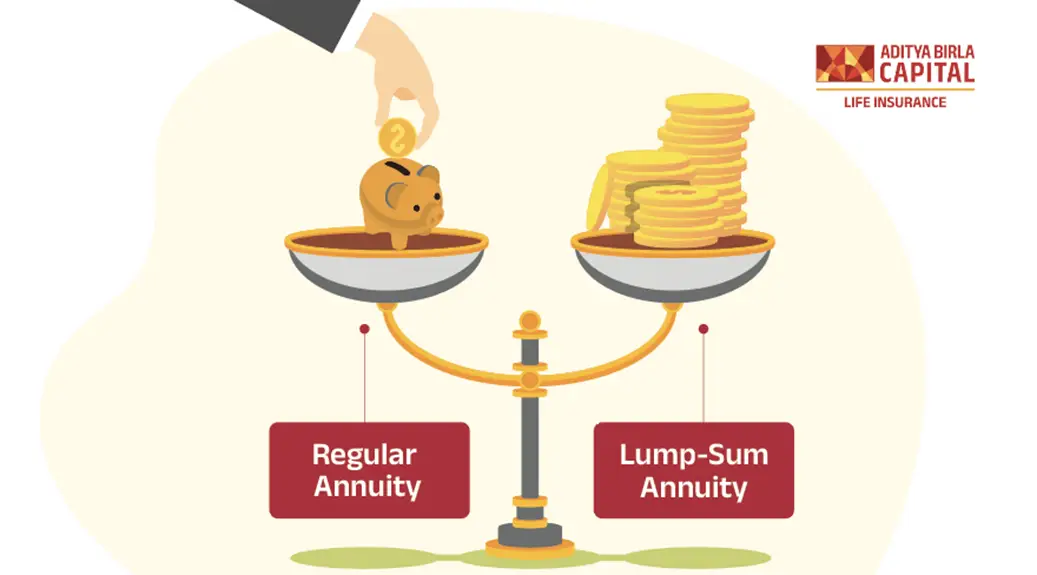

Regular Annuity or Lump-Sum - What is the Right Choice?

Plan Smarter, Live Better!

Table of Contents

Table of Contents

How Much Helpful You Found This Article?

Thank you for your feeback

FAQs

A regular annuity is a financial product that pays out a fixed amount of money at regular intervals, such as monthly or annually, often used as a steady income stream during retirement.

A lump sum annuity refers to a one-time payment received from an annuity plan, instead of receiving regular periodic payments.

A regular annuity is ideal for retirees who want a predictable and steady income stream to cover their living expenses and prefer not to manage large sums of money.

A lump sum might be suitable for individuals who are comfortable managing large amounts of money and believe they can achieve a higher return through other investment avenues.

The main advantages include guaranteed# income, lower immediate tax burden since payments are spread out, and reduced financial management responsibilities.

The primary advantages are immediate access to funds, flexibility to invest or spend as needed, and the potential for higher returns if invested wisely.

Receiving a lump sum could push you into a higher tax bracket, resulting in a significant tax liability in the year you receive the payment, unlike regular annuity payments, which are taxed more gradually.

Generally, once you choose an annuity payout option and the annuity is annuitized, you cannot change from regular payments to a lump sum. It’s crucial to make the right decision at the outset.

Inflation can erode the purchasing power of fixed annuity payments over time, while interest rates can affect the return on invested lump sum amounts. High inflation might make a lump sum more appealing if you can invest it further at higher returns.

A regular annuity typically offers less flexibility for estate planning since the income usually ceases upon death unless specific provisions are made. A lump sum, however, can be managed within your estate and passed on to your heirs according to your wishes.

Give ₹1 lakh/ month for 5 years and Get ₹ 4.01 lakhs every year till your life1

ABSLI Guaranteed Annuity Plus

Multiple annuity options, Regular income stream.

Guaranteed# lifelong income

Top-up option for annuity

Single/Joint Life cover option

Deferred annuity option

Give :

₹ 1 lakhs/Month for 5 year¹

Get :

₹4.06 lakhs/-

Most Popular Calculator

*Tax benefits are subject to changes in tax laws. Kindly consult your financial advisor for more details

ADV/7/24-25/809