As someone who cares about their family, you’ve probably heard about life insurance. However, have you paused to consider whether you need to get yourself an insurance policy? And if you do, what will that policy cover? Many people shy away from this topic even though it’s really important because it often sounds complex. But don’t worry, we’re here to help you understand everything you need to know.

How Life Insurance Works

What is life insurance all about? Think of it as a promise, a promise from an insurance company to support your family financially if you're not around. When you buy a life insurance policy, you agree to pay a certain amount of money, called a premium, regularly. In return, the insurance company promises to pay a sum of money to your loved ones if you pass away during the term of the policy. This money is known as the death benefit. The idea is simple: it's about securing the financial future of your family even when life throws unexpected curveballs.

What Deaths Does Life Insurance Cover?

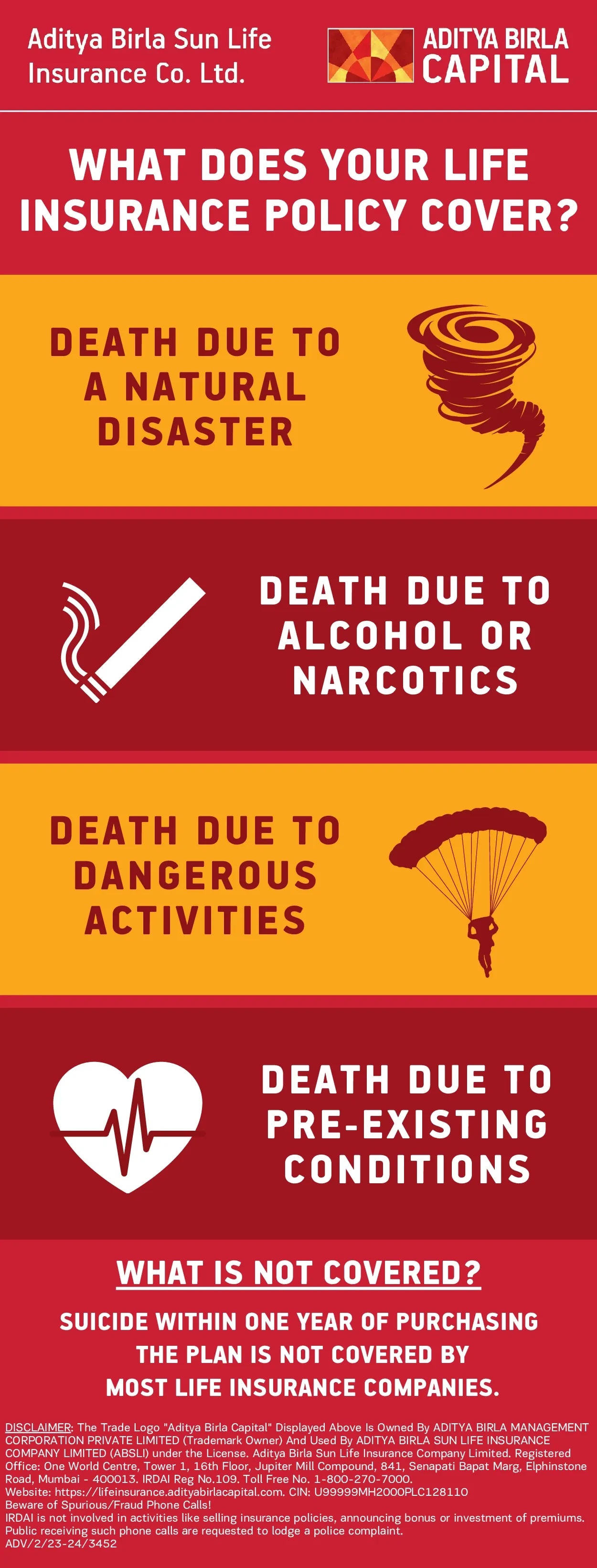

Now, you might be wondering: What kind of deaths are covered by life insurance? Generally, life insurance policies cover most causes of death - be it natural causes like illness or age, or unexpected events like accidents. But, there are a few exceptions.

For example, most policies do not cover deaths due to extreme risk activities like skydiving or deaths resulting from illegal activities. Also, if the policyholder hides important health information while buying the policy, there could be issues with the claim. It's always best to read the fine print and understand the specific terms of your policy.

What is Life Insurance Used For?

Life insurance is much more than just a financial tool; it's a way to show love and care for your family. The payout from a life insurance policy can be a lifeline for your loved ones in your absence. It can help them manage daily expenses, pay off debts, fund their children's education, or even help in maintaining their lifestyle.

Some people also use life insurance as a form of savings, thanks to policies that offer maturity benefits if you outlive the policy term. Plus, it's a great way to leave behind a legacy for your children or contribute to a cause you care about.

In essence, life insurance is a versatile tool designed to provide peace of mind, knowing that your family will be financially secure, no matter what the future holds.

Expenses Beneficiaries Can Help Cover Using the Life Insurance Death Benefits

When a loved one leaves us, it's not just an emotional loss but also a financial challenge. That's where life insurance death benefits come as a ray of hope. These benefits can be used in several ways to help beneficiaries manage their financial needs. Let’s take a look at what these funds can typically cover:

-

Daily Living Expenses:

The death benefit can help cover everyday costs like groceries, utilities, and rent. This support is crucial, especially if the departed was the primary earner in the family.

-

Children’s Education:

Parents always dream of a bright future for their children. Life insurance benefits can ensure that your children's education goals are not compromised, covering school fees and higher education expenses.

-

Debts and Loans:

If there were any outstanding debts or loans, like a home loan or personal loan, the death benefit could be used to pay these off, reducing the financial burden on the family.

-

Medical and Funeral Expenses:

Unfortunately, medical bills can be substantial, especially if there is a prolonged illness. Life insurance can cover these costs, along with funeral expenses.

-

Future Goals and Plans:

Whether it’s buying a home or starting a business, life insurance benefits can help keep those dreams alive for your family, even in your absence.

How Quickly Does Life Insurance Pay Out?

One common question about life insurance is: “How fast can my family get the money after I’m gone?” Usually, life insurance companies in India try to make the process as quick and hassle-free as possible. Once the claim is filed with all the necessary documents, the payout typically happens within a few weeks. However, the exact time can vary based on the policy terms and the company's procedures. It’s always good to check with your insurance provider about their specific timelines and requirements.

What Is Not Covered By Life Insurance?

While life insurance offers broad coverage, there are a few things it usually doesn't cover. Knowing these exclusions helps in understanding and choosing the right policy:

-

Suicide:

In most cases, if the policyholder commits suicide within a specific period (usually a year) after the policy start date, the death benefit might not be payable.

-

Death Under the Influence:

Deaths due to driving under the influence of alcohol or drugs are often excluded.

-

Illegal Activities:

If the policyholder dies while committing an illegal act, the claim might be denied.

-

Certain Hobbies and Professions:

High-risk activities like skydiving or certain hazardous professions might be excluded or require additional premiums.

-

Pre-existing Medical Conditions:

If not disclosed at the time of purchasing the policy, deaths due to undisclosed pre-existing conditions may not be covered.

It’s always important to read your policy document carefully and ask your insurance advisor about any specific exclusions or conditions.

Do Life Insurance Riders Offer The Same Coverage?

So, you've heard about life insurance riders and are wondering what they are? Think of riders as the extra toppings on your pizza, enhancing the base policy just like how extra cheese or toppings enhance your pizza experience. Riders are additional benefits that you can add to your basic life insurance policy, but they come at an extra cost.

Now, the big question: Do they offer the same coverage as the main policy? Not exactly. Riders are meant to provide additional coverage for specific situations that the main policy might not cover. For instance, there are riders for critical illness, accidental death, and waiver of premium, among others. Each of these riders addresses a specific need:

-

Critical Illness Rider:

This pays out a lump sum if you're diagnosed with one of the critical illnesses specified in the policy, like cancer or heart attack.

-

Accidental Death Rider:

This offers an additional payout if death occurs due to an accident.

-

Waiver of Premium Rider:

If you become disabled and can't earn an income, this rider waives off future premiums while keeping the policy active.

So, while riders don't provide the same coverage as the main life insurance policy, they complement it, offering more comprehensive protection tailored to your needs.

Conclusion

To wrap it up, life insurance is a key element in securing the financial future of your family. It’s about ensuring that your loved ones are taken care of, even when you’re not around. From covering daily expenses and debts to securing your children’s education and future dreams, life insurance offers a safety net for various needs.

Remember, choosing a policy and riders that suit your unique situation is key. And while no one likes to think about life’s uncertainties, being prepared can make all the difference. So, take that step today – your family’s tomorrow may depend on it. Here's to making wise choices for those we care about!

Table of Contents

Table of Contents