Buying a life insurance policy is an investment that you make for a better and financially stable future. It spans decades and significantly alters the futures of your loved ones. You buy life insurance so your family doesn’t face any difficulties even when you are not around. This is why you should know how to buy a life insurance policy.

Here we are breaking down each step in the life insurance application process so you can go through it seamlessly -

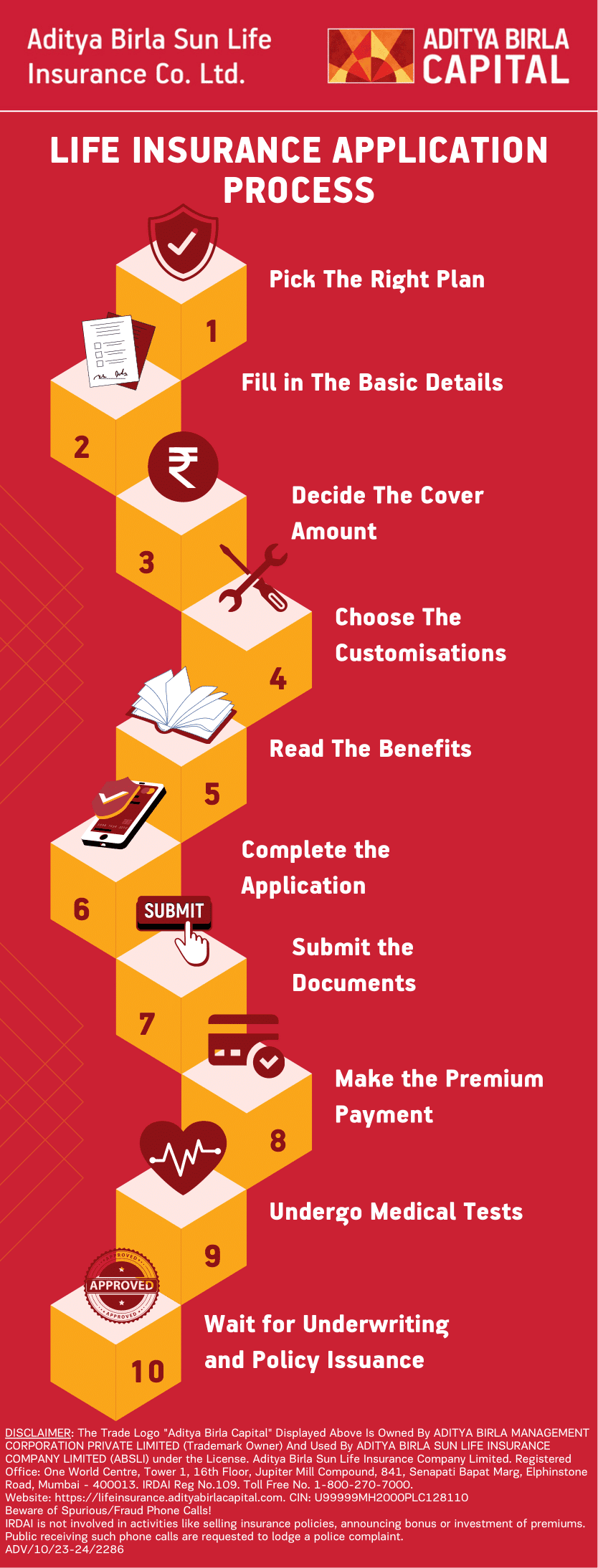

Steps Involved in Buying a Life Insurance Policy

-

Picking The Right Plan

The very first step is picking a plan that fits YOUR needs and requirements. Each person’s financial goals are different - some may want to save for retirement, some may want to build a fund for their child’s education, some may want to create a secondary source of income, etc. There are many plans available from various insurers that cater to different goals. Choose a plan that best fits your needs, financial goals, and requirements. The plan should be what you are looking for and not what others want you to buy.

-

Filling in The Basic Details

The next basic step will be for the insurance company to know you better. You will be required to give them a few personal details, which may primarily include:

- Personal details like your name, address for communication, date of birth, and any lifestyle questions.

- Contact details like your email ID, contact number, etc.

- Professional details like occupation, income, educational qualification, and so on.

These details are then used for calculating an estimate of your premium for the insurance policy you choose.

Please note that the details you’ll be asked will vary across insurers.

-

Deciding The Cover Amount

The most important stage in the life insurance application process is finalizing the coverage amount for your policy. On most websites, the cover amount is automatically filled for you. You can adjust the same as per your requirements and budget.

Make sure you choose a cover amount that covers the financial goals you have in mind. For instance, if you’re opting for a Retirement Plan, make sure the returns are enough to sustain you throughout your retirement. If you’re buying a Child Plan, the cover amount should be enough to support your child’s milestones. Ultimately you are buying a policy for yourself and nobody will know such needs better than you.

-

Choosing The Customisations

Now that you have chosen the type of insurance policy and its cover amount, you can go ahead and customize it according to your preference. You will be offered different options to tailor the insurance policy according to your unique needs.

Let’s have a look at the various customisation options -

? Premium Payment Term

You will also need to choose the premium payment term, i..e, the duration during which you can finish off paying the premiums of your plan.

Insurers generally offer you the following options:

a. Regular Pay Option

You pay the premium amount until the end of your term policy. In other words, the premium payment term and the policy term are the same.

b. Limited Pay Option

You can choose to pay your premiums within a lesser period of time in comparison to the policy term. This means that your premium payments, though higher than the regular, are completed sooner and you still get to enjoy the policy benefits until later.

Under this option Insurance providers offer different terms like 5-pay, 10-pay, 15–pay, etc. Here the number corresponds to the number of years you are willing to distribute your premium payments. Based on your choice, the premium amount is calculated and you can pay it within your preferred number of years.

c. Single Pay Option

Under this option, you pay the entire premium amount in one shot. The premium payment is made only once at the time of buying the insurance policy.

? Premium Payment Frequency

The next step in the life insurance application process is to decide how often you want to pay your premiums. This can be customized based on your financial stability and convenience:

a. Yearly

You can choose to pay the premium amount once a year.

b. Half-yearly

You can choose to pay the premium amount twice a year.

c. Quarterly

You can choose to pay the premium amount four times a year.

d. Monthly

You can choose to pay the premium amount twelve times a year.

? Policy Term

The policy term is the period of time during which you will be covered by the insurance plan. Choose a policy term that aligns with your financial goals. For example, if you’re buying a policy to meet the education expenses for your child’s higher studies 15 years later, then choose a policy term of 15 years.

? Increasing Cover Feature

If you aren’t eligible for the cover amount you want right now or want to ensure that your term insurance is protected from ever-rising inflation rates, there are options to increase the cover amount of your policy. If you choose this increasing cover feature, your cover amount will gradually keep increasing until it reaches a limit as set by the insurer.

Please Note: There are also options available to increase the payouts that you are entitled to receive in the future. Such returns can be increased by 5-10%.

? Benefit/Claim Payout Option

The next customization available in the life insurance application process is choosing the claim payout option. You get to decide how you want the maturity or death benefit to be paid to you or your family, based on the financial aptitude and goals of the recipient. It is to be noted that each insurance provider may have different payout options, but these are a few common ones -

a. Lumpsum Payout Option: Choosing this option will entitle you or your family to receive the entire amount in one single payment.

b. Monthly Income Payout Option: When you choose this option the cover amount is disbursed as monthly payments, over a specific number of years.

c. Lump-sum With Monthly Income Payout Option: Choosing this option will be a combination of both the above-mentioned payout modes. A part of the claim/ benefit amount is paid in lumpsum and the rest is paid in the form of monthly instalments over a period of years.

? Riders#

Riders# are add-ons that can be added to your policy at an extra cost. They enhance the coverage of your policy and give you payouts on the happening of a specified event. You can choose from the following riders# (this is an indicative list and may vary across insurers) -

a. Accidental Death Benefit Rider#

b. Waiver of Premium due to Critical Illness Rider#

c. Surgical Care Rider#

d. Critical Illness Rider#

e. Accidental Disability Rider#

f. Waiver of Premium due to Accidental Disability Rider#

g. Hospital Care Rider#

So, for instance, if you choose the waiver of premium due to a critical illness rider#, all your future premiums will be waived by the insurer if you contract any of the critical illnesses listed in the policy document.

- Reading The Benefit Illustration

The next stage in your life insurance application process is reading the benefit illustration, which is like a user manual for your insurance policy. This document can be downloaded from the website itself or may be mailed as a PDF by your insurance provider. This illustration will give you end-to-end information on how things work with your policy, its coverage, and its premiums.

The benefit illustration document contains details like the policy features, available rider# options, etc. On reading this, you will be able to understand how your premium payments are invested, how the fund value gradually grows over the years, the charges that are deducted by the insurer, and much more. The document includes details on

• Guaranteed3 and Non-Guaranteed benefits that are payable

• Loyalty and Guaranteed3 additions, if applicable

• Maturity and Death Benefits as payable by the insurance company, etc.

The benefit illustration document is your guide to each and every component of the policy, for every year. It also depicts how the invested money will gradually grow year after year.

- Application Process

The next step is completing the life insurance application process. You will be required to enter your details on the insurance company’s website, including your personal, communication, medical, and lifestyle details.

(Please note that this is an indicative list and may vary across insurers.)

? Personal details

• Name

• Mobile number

• Email id

• Income

• Educational qualification

• Occupation

• Temporary and permanent address, etc.

? Medical Details

This is a mandatory clause that you have to provide to the insurance company. It has details that help in knowing your health conditions.

These details include -

• Past medical history

• Illness or disease that you may have been treated for

• Any medical conditions that the insurer must know about

• Surgeries and treatments that you have undergone in the past

• Your family’s medical history

• Basic BMI and body measurements like your height, weight, sugar level, BP level, etc.

? Lifestyle-related details

This includes details about a few of your lifestyle choices that may affect your health, like smoking, drinking, and other such habits.

For instance,

• If you are a smoker, you will have to update how often you smoke and the number of cigarettes that you smoke in a day.

• If you drink alcohol, the insurer would want to know what type of alcohol you consume, how often you consume it, and the quantity you consume in a day or a week.

? Other Details

• Nominee details

The nominee is the person entitled to receive the claim amount if you happen to pass away during the policy term. You can choose any member of your family as the nominee for your policy - your spouse, mother, father, child, or siblings. You will be required to provide details about them too.

• Participation in adventurous activities

Though fun to participate in, insurance companies consider adventurous activities like rock climbing, scuba diving, kayaking, paragliding, etc. a red flag. You will need to inform your Insurance provider about your past participation in such activities and also if you intend to do them in the future.

• Travel plans

Insurance providers may also require you to furnish details about your immediate travel outside India, if any.

• Covid-19 details

As a recent development after the pandemic, insurance companies may also ask you about your Covid-19 vaccination and whether you have received both doses. It may also be compulsory to update the insurance company if you were ever diagnosed with Covid-19 before or if any of your family members were diagnosed with the same.

- Submitting The Documents

Along with the application, you will be required to submit a few documents to verify the information furnished. These documents are considered proofs to be eligible to apply. They include

• KYC documents such as PAN Card, Aadhar Card, Passport, Voting Card, etc.

• Income proof documents such as Salary Slips of the last 3 months, Employer's Certificate, Bank Statement of the last 6 months, Income Tax Returns, Form 16, etc.

- Making The Premium Payment

The next step in the life insurance application process is to pay the first premium. The premium payable is calculated on the basis of various factors like -

• The cover amount you have selected

• The policy tenure

• The premium payment term (limited pay, regular pay, or single pay)

• The riders# you have added

• Your age and gender

• Your health and lifestyle habits

These factors may vary across different insurance companies.

You will also see an e-SI (electronic standing instruction) option on some insurance websites. If you select this option, your premiums will be transferred directly to the insurance company on every due date. This ensures that you don’t miss out on payments.

Some insurers may require you to pay the first premium due before you complete your life insurance application process. Others might require you to pay the premium after you complete the application and document submission. It depends on the policy type chosen which varies from insurer to insurer.

- Undergoing Medical Tests

To support the medical information shared by you regarding your past medical history, your family’s medical history, the type of insurance policy chosen by you, and the coverage amount opted for, you will be required to undergo medical tests. A few of them are:

• TMT or a treadmill test

• Blood test results to know if you have cholesterol, diabetes, any heart diseases, and your haemoglobin levels.

• Drug test for knowing about any drug usage, alcohol consumption, or regular smoking habits.

• Other tests like HIV tests, ECG, kidney, and liver functionality tests, etc.

-

Underwriting

The next stage involved in the life insurance application process is the evaluation of your application by a team of underwriters. They will thoroughly analyze your financial and medical conditions. Based on the documents submitted, they will check your eligibility for the cover amount. They will also check the submitted documents and give a report on how risky your application is to the insurance company.

-

Policy Issuance or Rejection

Based on the report submitted by the underwriting team, your application may be:

• Accepted and the policy issued.

• Rejected, if they find your profile to be too risky to cover

• Counter-offered, by asking you to pay a “loading” - a higher premium amount. If you agree with an extra premium payment, then the policy is issued to you.

- Checking The Policy Details in The Free Look Period

Once the policy is issued to you, you will get a copy of the policy papers in both hard and soft copies.

• The hard copy will be sent to your communication address.

• The soft copy will be mailed to your email id.

You then a get period of 15 days, known as the free look period, to read through and check if all your customizations, add-ons, and features are correctly mentioned in the documents. In case you find errors or corrections, you can get them rectified during this period.

Ensure that the limitations, terms, and conditions are as agreed upon with the insurance provider. If you find any misrepresentation or incorrect information in the documents or are unhappy with the policy, you can use this period to return the policy to the insurer. While doing so, you will not be charged any penalty or cancellation charges - except stamp duty, administration charges, etc.

Summing Up!

We have covered all the key points and topics that you need to know in completing your life insurance application process. If you have read through the entire article, then you are now ready to go buy the policy that best suits your needs.

Table of Contents

Table of Contents