Wouldn't you agree that comparing your options is an essential part of shopping? Think about your regular trip to the local market, for instance. You compare the different fruits and vegetables available to you, and you select the ones that you need the most. Or, think of your online shopping sprees. Don't you spend hours going through reviews and comparing different versions of the same product?

When it comes to shopping for life insurance too, a bit of due diligence can go a long way. This is all the more essential because there are different types of life insurance plans. Life insurance can be categorized into different groups based on various parameters.

One such parameter of difference is whether or not a life insurance plan passes on the profits of the insurer to the policyholder. Based on this factor, we have two types of life insurance plans, namely participating and non-participating life insurance policies.

Wondering what the difference between participating and non-participating insurance plans is? We'll give you all the details.

What is a participating life insurance policy?

A participating life insurance policy, also referred to as a par policy, allows the policyholder to participate in the profits of the life insurance company. The life insurance company, like all organizations, will earn profits over the course of a financial year, isn't it? In a participating plan, the benefits of these profits are passed on to the policyholder.

These benefits are paid out to the policyholder in the form of bonuses or dividends. Typically, the payments are made every year, on an annual basis. If you hold a participating policy, you can receive or make use of the bonuses and/or dividends in the following ways:

- You can receive the payouts as and when they are made by the insurer.

- You can make use of these payouts to pay the premium due on your policy.

- You can deposit the bonuses or dividends with the insurer and allow those funds to earn interest.

These participating benefits are in addition to the regular maturity benefits guaranteed# by the life insurance plan.

What is a non-participating life insurance policy?

As you may have figured out by now, a non-participating insurance plan - also known as a non-par plan - does not offer any dividend payouts. In other words, the policyholder does not participate in the profits of the life insurance provider.

Unlike a participating insurance policy, a non-participating policy does not pay out any bonuses or dividends based on the insurer's profits. However, these life insurance plans do pay out guaranteed# benefits on maturity.

Participating vs. non-participating insurance: Key areas of difference

Now that you know the meaning of both participating and non-participating plans, let's take a look at how these two kinds of policies differ from one other. Here are the key points of difference between participating and non-participating insurance plans.

Share in profits

A participating life insurance policy allows you to participate in the profits of the life insurance provider, while a non-participating insurance plan does not come with any such feature.

Guaranteed# vs. non-guaranteed# benefits

A non-participating insurance plan provides only guaranteed# benefits to the policyholder. This is the sum assured payable on the policyholder's demise, or the maturity benefits payable when the plan matures. On the other hand, a participating life insurance policy pays both guaranteed# benefits and non-guaranteed# bonuses or dividends based on the insurer's profits.

To offer better clarity on the key points of difference between participating and non-participating insurance plans, we've summed up the details in the table below.

|

|

Participating policy

|

Non-participating policy

|

|

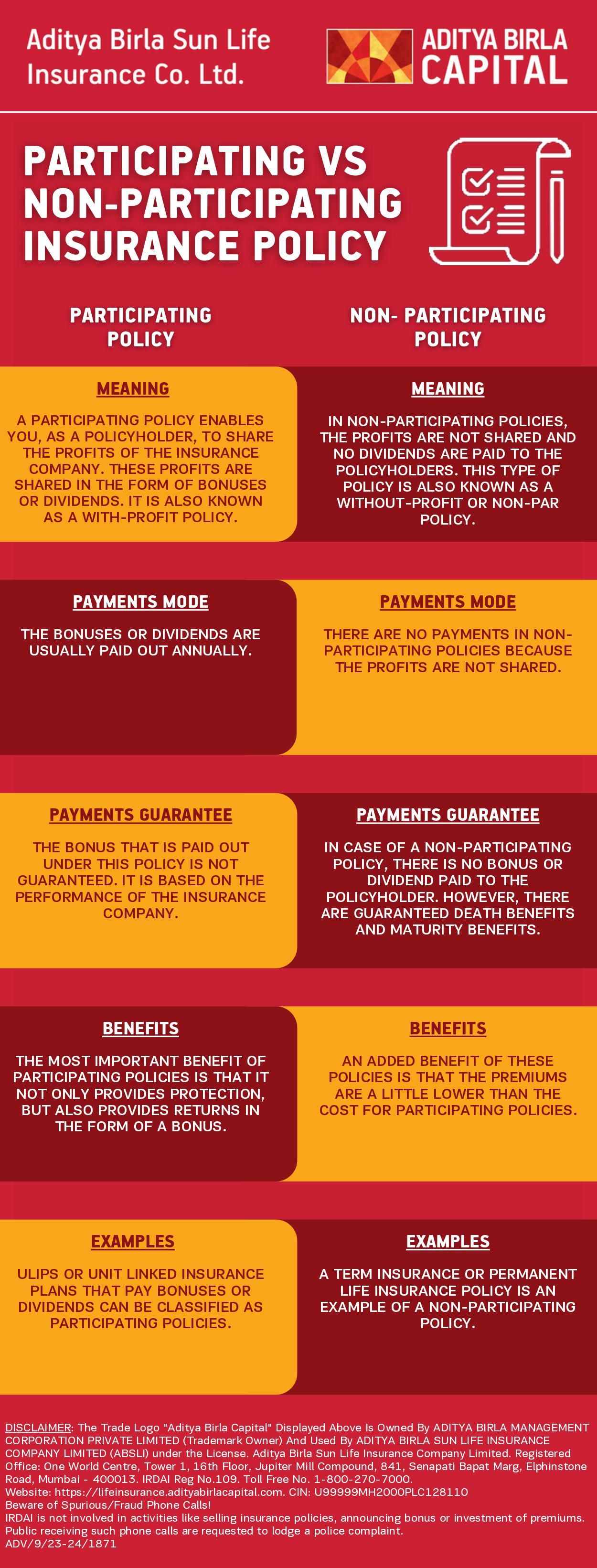

Meaning

|

A participating policy enables you, as a policyholder, to share the profits of the insurance company. These profits are shared in the form of bonuses or dividends. It is also known as a with-profit policy.

|

In non-participating policies, the profits are not shared and no dividends are paid to the policyholders. This type of policy is also known as a without-profit or non-par policy.

|

|

Payments made

|

The bonuses or dividends are usually paid out annually.

|

There are no payments in non-participating policies because the profits are not shared.

|

|

Payment guarantee

|

The bonus that is paid out under this policy is not guaranteed#. It is based on the performance of the insurance company.

|

In case of a non-participating policy, there is no bonus or dividend paid to the policyholder. However, there are guaranteed# death benefits and maturity benefits.

|

|

Benefits

|

The most important benefit of participating policies is that it not only provides protection, but also provides returns in the form of a bonus.

|

An added benefit of these policies is that the premiums are a little lower than the cost for participating policies.

|

|

Examples

|

ULIPs or [Unit Linked Insurance Plans](https://lifeinsurance.adityabirlacapital.com/ulip-plan/) that pay bonuses or dividends can be classified as participating policies.

|

A term insurance or permanent life insurance policy is an example of a non-participating policy.

|

|

Table of Contents

Table of Contents