Before you set out to buy something crucial, say an electronic gadget, a house, a car, etc. - you spend hours scrolling through various websites, watching YouTube reviews, researching all the nitty gritty details like the configuration, specs, and most importantly, the product that fits your needs, requirements, and budget.

Following a similar approach before opting for an insurance policy shall go a long way. The market offers different types of whole life insurance, and it is crucial to understand the differences before jumping on to buying one.

Whole life insurance is basically a policy that provides coverage for your entire life. In a nutshell, a whole life policy allows you to live a worry-free life while being able to leave a remarkable legacy to their loved ones. As a result, when you make this decision, it's vital that you choose a suitable whole life plan that fulfils your financial needs and preferences.

In general, there are different types of whole life insurance based on the policy features. In this article, we’ll see what participating and non-participating whole life plans are and how they differ.

Without further ado, let’s get started!

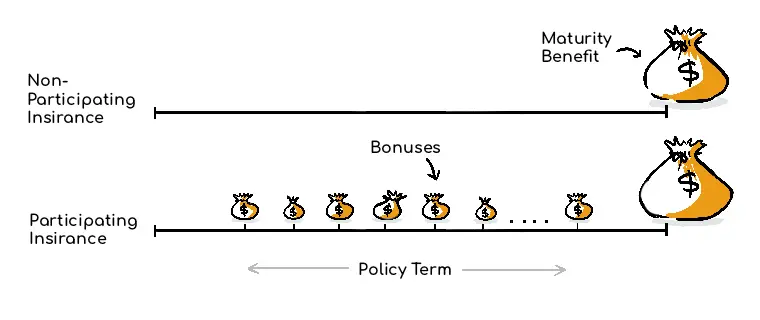

What is Non-Participating Whole Life Insurance?

Non-Participating Insurance are the plain vanilla variety of insurance plans. They offer guaranteed benefits, i.e, assured payouts at the end of the policy duration or in the event of the insured's death.

It’s like when you join a company that offers only a fixed salary and there is no variable component like a bonus in your CTC, that is linked to your performance or the company’s performance. What you see is what you get.

Similarly, as the term implies, in a Non-Participating plan, you do not participate in the insurance company's profits, hence there is no variable benefit like dividends or bonuses in this plan. What is promised when you buy the plan is exactly what you get.

What is Participating Whole Life Insurance?

Participating Insurance offers variable bonus in addition to the benefits paid, whether it is paid at policy maturity or as a death benefit.

This bonus is linked to the profits a company makes from such participating policies.

Picking the same salary example we took earlier, a participating insurance is like when you have a fixed component and a variable component in your CTC. A variable component that is linked to your performance and probably to the company’s performance. If the company does well in the said period, the bonus would be different compared to when the company didn’t do that well.

The overall profit is earned by the company by selling more policies in a year, receiving lesser claims, returns from investing the premiums collected into approved investment products like government bonds, stock market, equity instruments, debt instruments, depending on product to product.

You receive these benefits in the form of bonuses or dividends.

The dividend can be used in different ways -

- it can be used to pay the insurance premium.

- it can be accumulated with the policy or insurance company itself to generate interest like a regular savings account, or

- you can take a cash payment

Of course due to the variable nature of returns, Participating Insurance will have higher premiums compared to Non-Participating policies.

Note to Remember

- Guaranteed Benefits – Sum assured at policy maturity and/or sum assured at insured's death

- Additional Bonus – Bonuses or Dividends offered by the insurance company.

Comparison of Participating and Non-Participating Whole Life Insurance Policy

Here are the aspects that are similar between Participating and Non-Participating policies:

- Death Benefit - Provide a death benefit to the nominee.

- Customization - Customising the plans with riders and reducing premium paying terms is possible.

- Tax Benefits - Offer tax benefits under sections 80C and 10(10D) of the Income Tax Act.

- Loan Provision - Provide an option of taking a loan against your policy.

And here are the aspects, where these two policy types differ from one another

Here’s a simple table to understand the differences -

|

|

Participating Whole Life Insurance

|

Non-Participating Whole Life Insurance

|

|

Profit sharing with policyholder

| The profits earned by the Insurance company are shared with you in the form of bonuses. | The profits earned by the Insurance company are not shared with you. |

|

Benefits

| Both guaranteed as well as Non-Guaranteed benefits (in the form of bonuses) are offered. | Only guaranteed benefits on the death of the insured or policy maturity is offered. |

Let’s understand the difference better with an example:

30-year-old Mr Ram buys a Whole life insurance with a cover of Rs 15,00,000/-. The premium payment tenure for the same is 10 years and he will start to receive benefits right after he finishes his payment tenure for the next 40 years, on an annual basis, which shall be 3% of the sum assured.

Scenario 1 - If it’s a Non-Participating Whole Life insurance Plan

Mr Ram buys a non-participating whole life insurance plan of Rs 15,00,000 coverage. He chose this policy because the premium is relatively cheaper and meets his monthly budget. When his premium payments gets over by the time he turns 40, he shall start receiving the benefit payout as guaranteed annual income as per the following criteria:

3% of the sum assured = 3% of 15,00,000/-

= 45,000/-

He shall get this annual payout of Rs 45,000/- till the benefit payout period of 40 years i.e from age 40 to age 80.

As per the policy prerequisites, he shall receive the sum assured of Rs 15,00,000/- as maturity benefit once the plan ends when he turns 100 years or as death benefit to his nominee if he passes away during the policy period. He shall not receive any accrued bonuses or dividends as this is a Non-Participating policy.

Scenario 2 - If it’s a Participating Whole Life Insurance Plan

Mr Ram buys a participating whole life insurance plan of Rs 15,00,000/- coverage. He chose this plan because he has sufficient income to pay off the higher premiums and wanted to earn an upside, beyond plain guaranteed returns.

Under this policy, once Mr. Ram hits age 40, he shall get the same annual benefit for the next 40 years ,i.e., 45,000/- as guaranteed annual income from age 40 till he turns 80.

In a participating plan, the policy will pay Rs 15,00,000/- as either maturity benefit or death benefit along with accrued bonuses or dividends declared, depending on the overall profits made by the insurance company.

Both participating and non-participating policies have their own advantages and limitations. Unlike Non-participating plans that offer fixed returns, a participating plan is ideal for those individuals who do not want plain benefits and want an upside in the form of bonuses and dividends.

Ensure you have understood the variable nature of this benefit, and that past history of bonuses may not be indicative of any future benefits.

Key takeaways from this chapter

Key takeaways from this chapter