Term insurance is one of the most crucial investments you will make for your family’s financial protection. And, given the long-term impact it has on your family’s financial stability, it is important that you understand how it works. Why? So you don’t make any mistakes while buying the policy. And, because a small mistake on your part now could cost your family dearly in the future.

So, how does term insurance actually work? Let’s have a look!

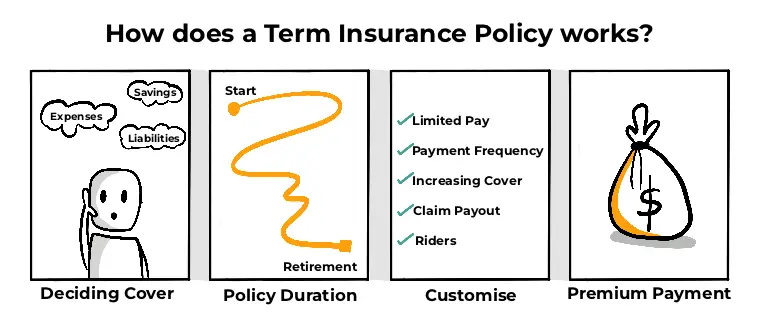

How Does A Term Insurance Policy Work?

Deciding the cover amount

If you don’t want your family to end up with insufficient cover after you’re gone, ensure you buy a term plan with the right coverage. For calculating the appropriate cover amount for your family, take into account four aspects -

- Living Expenses Fund (short-term expenses like basic needs, groceries, monthly bills, etc.)

- ADD Major Expenses Fund (long-term goals like children’s education, wedding, etc.)

- ADD Major Liabilities Fund (any large loans you’ve taken)

- MINUS Existing Funds (money that you already have - your savings, fixed deposits, etc. multiplied by the appropriate risk factors)

Learn in detail about how you can calculate the term insurance cover amount in this article:

While you calculate the cover, you’ll also have to factor in inflation so that the cover amount is sufficient for your family in the future. For this, you can multiply the calculated cover amount by 2.5 to 3X. The sum you arrive at will represent the gap in your family’s protection. You’ll have to subtract this with the amount of life insurance cover you already hold (if any), and then buy a term cover for the difference amount.

You can either do this entire calculation manually or use our Human Life Value (HLV) Calculator - where you can find out the cover amount that will be appropriate for your family, in just two minutes.

Choosing the policy duration

While deciding the term insurance policy duration, take into account your current income, savings, and future expenses. Then, estimate the age by which you’d have fulfilled all your financial obligations and created enough wealth to take care of the remaining part of your life. Basically, estimate the age by which you plan to retire.

This is the age till which you should buy the term insurance plan (perhaps with an additional buffer of 5 years).

Customising the policy

There are a lot of customisation options available with a term insurance policy. Some of these customisations include -

-

Limited pay

If you don’t want to continue paying your premiums till the end of the policy duration, you can choose the limited pay option. With this, you can finish paying your premiums in faster and bigger instalments to get the premium paying liability off your chest quickly.

-

Premium payment frequency

You also get to customise the premium payment frequency under your term insurance. Meaning, you can choose how frequently you want to pay your term insurance premiums.

Generally, there are 4 options available. Based on your convenience, you can choose to pay your premiums -

- Annually

- Semi-annually

- Quarterly

- Monthly

Increasing cover

Your expenses and liabilities are likely to increase as you grow older and take up more financial responsibilities. As a result, you will need to upgrade your term insurance cover too. Why? So that your family is adequately covered, always.

The increasing cover option allows you to seamlessly upgrade your term insurance cover. With this option, your sum assured will keep on increasing gradually at specific intervals, until it reaches a maximum limit.

You can learn in detail about the increasing option in term insurance here:

-

Claim payout options

Term insurance also allows you to customise how you want your family to receive the claim amount. Based on your family’s financial aptitude, you can choose from the following claim payout options -

-

Lump-sum payout option:

Here, the insurance company will pay the entire claim amount in one go. This option will be suitable if you have unsettled loans/ liabilities.

-

Monthly income payout option:

Under this option, your family will receive the claim amount in monthly instalments for a certain period of time. This option could be beneficial if you don’t have any loans or liabilities, and you are buying the term plan to provide for your family’s everyday needs.

-

Lump-sum with monthly income payout option:

This is a combination of the above two options. Here, a part of the claim will be paid as a lump sum, and the remaining claim will be paid in monthly instalments for a specific period.

You can learn in detail about the claim payout options in term insurance here:

Riders

With most term insurance policies, insurers also offer riders at a certain extra cost. Riders are easy-to-buy add-ons that provide an additional payout under certain circumstances.

For example -

- An accidental death benefit rider will pay an additional sum of money to your nominee if you pass away due to an accident.

- A waiver of premium due to critical illness rider will waive off all your future policy premiums if you’re diagnosed with an illness listed in your policy document.

Here’s a list of some riders you can purchase with a term insurance plan -

- Critical Illness Rider

- Accidental Disability Rider

- Accidental Death Benefit Rider

- Waiver of Premium due to Critical Illness Rider

- Waiver of Premium due to Accidental Disability Rider

- Hospital Care Rider

- Surgical Care Rider

Please note: This is just an indicative list. There can be other types of riders available with term plans, depending on the insurer you buy from.

Ensure you check the relevant policy documents so you’re well-informed before making the purchase.

You can learn about riders in detail in this article:

Paying the premium and policy issuance

The insurance company will calculate your premium on the basis of several factors, like -

- Age, gender, health, lifestyle habits, etc.

- The cover amount you decide

- The policy duration you select

- The premium paying option you choose (limited pay or regular pay)

- The riders you pick, etc.

After you provide your basic information, select all the customization options, and make the initial premium payment, the underwriting process will begin. If your application is accepted, the insurance company will issue the policy to you.

Paying the renewal premium

After the policy is issued, you will be required to pay the premiums regularly to keep it active. If you miss even a single premium due date, there are chances of your policy lapsing, i.e., ending. And, if that happens, all benefits under your term insurance policy will cease.

Hence, ensure you pay your premiums on time. To streamline this, you can -

- Put standing instructions on your bank account, and not on a credit/ debit card. Because the cards come with an expiry date, during which your payment might not go through smoothly.

OR

- Select the e-SI (electronic standing instruction) option at the time of buying the term insurance. With the e-SI option, your premiums will be transferred directly to the insurer.

When and how will the policy pay?

If you pass away while the policy is active, the insurance company will pay the death benefit, i.e., a fixed amount of money to your family. Your family will receive this money as per the claim payout option you chose while buying the policy.

What if you survive the policy term?

Term insurance is a pure risk insurance cover. If you survive till the end of the policy duration, it won’t pay any benefits to you.

Example

Let’s understand how a term insurance policy works with the help of Avneet’s example.

Avneet, 25, buys a term insurance policy with a sum assured of Rs. 1 Crore. She buys the policy for a duration of 50 years and opts for limited pay with a premium payment term of 15 years. So, she is supposed to complete all her premium payments in the next 15 years. Avneet also chooses the lump sum claim payout option and appoints her younger sister Tanya as the nominee.

So -

| Sum Assured | Rs. 1 Crore |

| Policy Duration | 50 Years |

| Premium Payment Term | 15 Years |

| Claim Payout Option | Lump-sum Payout Option |

Let’s see how Avneet’s term plan will work in the following two scenarios -

1. Avneet passes away in the middle of the policy tenure.

2.

3. Avneet survives until the end of the policy duration.

Scenario 1: Avneet passes away in the middle of the policy tenure.

Let’s say Avneet has completed all her premium payments under the policy. And, in the 30th policy year, she passes away due to a heart attack.

In this case, the insurance company will pay a claim of Rs. 1 Crore to Tanya (Avneet’s nominee). And, because Avneet selected the lump sum claim payout option, the claim amount will be paid as a lump sum, in one go.

Scenario 2: Avneet survives until the end of the policy duration.

If Avneet survives the entire policy term of 50 years, her policy will terminate. And, she won’t be paid anything.

Wrapping up!

Term insurance is a pure risk policy that works in a very simple manner. Based on your financial obligations, you can choose the cover amount and policy duration. Then, you will have to make timely premium payments in order to make sure your policy remains active. If you pass away while the policy is in force, it provides your family with a death benefit, i.e., a fixed sum of money. And, in case you survive, there is no payback.

Key takeaways from this chapter

Key takeaways from this chapter