Insurance at its core is a very simple concept - it is the concept of spreading a large financial risk that each member of the community faces, amongst themselves.

If bought right, insurance can save people from several financial catastrophes. One of the biggest, and most impacting risks and financial catastrophes a family faces is the risk of losing its primary earning member. Ask anyone who has lost an earning member, usually a father in their childhood, and they will have stories to share about how one single incident ruined their entire lifestyle, goals, and dreams. A life insurance policy primarily covers this critical risk.

In this article, let’s understand what this crucial product called life insurance exactly is, how it works, and more. So, let’s dive right in!

What Is Life Insurance?

Life insurance is designed to provide financial security to dependent family members in the event of the untimely demise of the primary earning member.

Apart from covering family members and protecting their future lifestyle and goals, life insurance is also used to cover loans/liabilities, or plan for long-term financial goals like retirement, a child's higher education or wedding, etc.

Life insurance is basically a financial product where a fee (called the premium) is charged based on the probability of the risk of death of certain demographics of people. It is either sold by the insurance company's employees or by distributors like agents, banks, and brokers in the market.

How Life Insurance Policy Works?

Let’s understand with the help of an example.

Imagine it is the 1920s. There are 10 earning members in a small town. Through past trends, they know for sure that every 5 years one earning member dies in a family in that town - and that family needs Rs. 10,000 to continue their lifestyle without the earning member. Now, either each earning member can provide Rs. 10,000 as an emergency fund to their family or pool Rs. 10,000 every 5 years amongst all members, which means paying a fixed amount of Rs. 400 every year (equal to Rs. 2000 for 5 years), instead of the risk of having to save and keep Rs. 10,000 forever.

In the example above -

- The Rs. 10,000 that the earning member needs to ensure their family continues to live their lifestyle is the cover amount or in technical terms - the sum assured.

- The Rs. 400 paid to the community every year instead of saving the entire risk amount of Rs. 10,000 is nothing but the premium.

The earning member covered under the policy is called ‘life assured’ or ‘insured’ in insurance parlance.

- The dependent family members whose lifestyle is protected are called ‘nominees’ or ‘beneficiaries’.

So, life insurance is simply a contract where your financial risks are covered in exchange for payment of a premium.

How is the life insurance premium determined?

Although the example we used above to explain the concept of insurance was very simple, the real world of insurance can be quite complicated. Estimating the death rate for a group of people over decades requires sophisticated mathematics. This estimation is done by a team of professionals called ‘Actuaries’.

An actuary’s job is to use mathematics, statistics, and financial theory to estimate the risk covered under a life insurance product and calculate the premium amount to be charged by insurance companies. All life insurance products are designed and priced by insurance companies assuming a standard profile with a certain degree of risk - called ‘standard risk’.

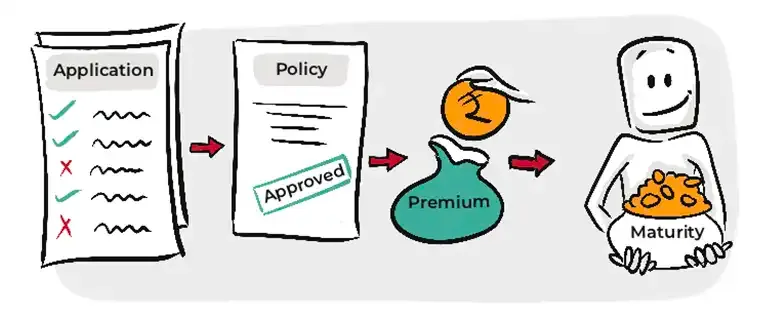

Buying Process Of Life Insurance Policy

Insurance is not bought like a commodity - like, say, a soap, where you go to the market and simply pick your favourite brand and pay for it. When a customer is interested in buying a product, s/he has to apply for the product. Only when the application is approved by the insurance company, the policy is issued to the customer and the risk cover actually starts.

1. Evaluation Of Your Application

When you apply for an insurance policy, the insurance company will evaluate your risk and eligibility.

● Risk: The risk you carry will be compared to the standard risk assumed by the insurance company. Here, the insurance company will look at two things -

➔ Your profile

The insurance company will ask you to provide details related to your occupation, income, location, etc. They will compare your profile against the standard profile they have defined in the policy. They will then determine whether the degree of risk you carry is higher than what was assumed when the product was designed.

➔ Your health

Similarly, the insurance company will want to know your health status. They will then understand if you have a lifestyle or a health condition that puts you in a higher risk zone than a standard healthy individual as assumed when designing the policy.

● Eligibility: Next, your eligibility will be evaluated too. The insurance company will want to ensure that you are buying the insurance policy clearly for the financial security of your family, and not to simply make a gain from the product or the scheme.

Your risk and eligibility will be evaluated by a team of professionals at the insurance company called underwriters. The underwriter’s job is to -

➔ Evaluate every application or proposal that the insurer receives.

➔ Decide whether to provide the cover or not, after the application for the policy is made.

➔ Define whether a particular customer’s risk is higher than the standard risk defined.

➔ Determine the additional premium that must be charged in the form of loading, if a customer carries a higher risk than usual.

2. Policy Issuance

If the underwriter approves your application, the operations team at the insurance company will issue the insurance policy to you. As soon as the policy is issued, the risk coverage will begin.

3.Paying The Premiums

Based on the premium payment terms under your policy, you will have to continue paying the premiums. Make sure you don’t miss your premium payment due dates because the policy and the coverage will only remain active as long as you complete all your premium payments on time.

4. Making A Claim

In the unfortunate event of your death during the policy term, your nominee or family will have to inform the insurance company. They will have to submit several documents and provide details of the death, etc. Then, based on the terms and conditions of the policy, the claims team of the insurance company will evaluate the claim. If approved, the claim payout will be made to your nominee.

How Does Life Insurance Company Make Money

When you complete your application, and it is approved, the life insurance policy is issued to you. You then start making periodic premium payments to the life insurance company to keep your policy active. If you pass away in the middle of the policy term, the life insurance company will pay the claim amount to your nominee.

The insurance company's profitability depends on how it manages those premiums between its receipt and payment of the claim amount (if any). They generally make money in three ways -

1. Operating Income

Insurance companies employ actuaries to calculate the premiums that will be charged to customers in order to meet the liability of paying them claims in case of death and also earn a specific profit. They make money in the long run from the extra premiums collected over claims

2. Interest Income

Insurance companies may make money off of premiums directly, but the money they make from investing that money is even more substantial. Insurance companies collect premiums in advance before providing insurance coverage to the insured person. This advance premium is invested by insurance companies in investment avenues allowed as per insurance regulations. Insurers profit from this investment.

3. Income From Lapsed Policies

Although insurance companies lose future revenue from lapsed (expired) policies, they also profit from them. How? Well, when an insurance policy lapses, it is no longer a liability for the insurance company. They don’t need to pay out the entire maturity or death benefit on that policy.

We hope this article gives you a better understanding of how life insurance policies and life insurance companies work. We also hope the buying process we mentioned above will help make your life insurance purchase journey much easier.

Key takeaways from this chapter

Key takeaways from this chapter