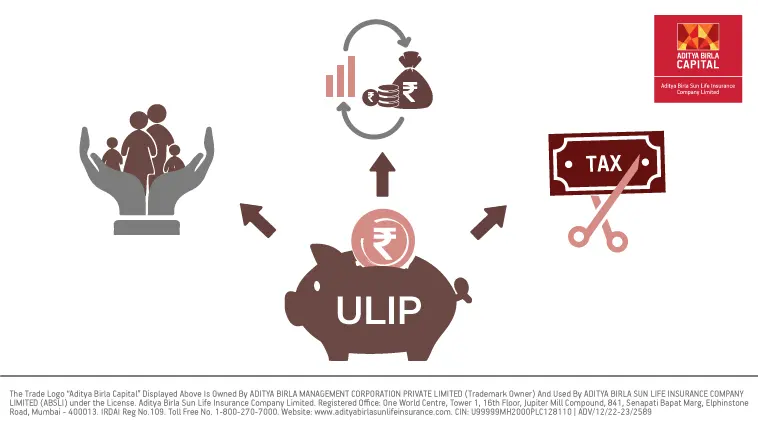

Unit-linked insurance plans, or ULIPs as they are popularly called, allow you to explore the securities of the capital market along with life insurance protection. You can create a market-linked corpus for your financial goals and earn attractive returns on your investments. Moreover, the flexibility offered by ULIPs allows you to manage your investment at your discretion so that it keeps pace with your changing investment strategies.

A ULIP can be a good addition to your financial portfolio. Here are some reasons why –

1. Insurance + Investment in one

One of the main benefits of a unit-linked plan is its ability to generate investment returns while allowing life insurance coverage. Thus, you can fulfil two needs with one plan – the first one being the need for financial security in the event of an unforeseen contingency and the second being the need for corpus creation for your financial goals.

As you allocate your premium towards the available funds with a view to earning market-linked returns, the plan ensures that your family stays financially protected if you are not around. This gives you financial security as you plan for your goals.

2. Different types for different goals

There are different types of ULIPs available in the market to meet the different financial goals that you might have. Have a look –

- Basic ULIP

These are savings-oriented ULIPs that help in creating a corpus for any financial goal that you might have in mind. You can pay the premium and accumulate a corpus for your needs.

- Whole life ULIPs

These are protection-oriented ULIPs that allow coverage till 99 or 100 years of age. Thus, you can enjoy lifelong protection while creating a corpus for your goals.

- Child ULIPs

These ULIPs are specifically designed to cater to the financial needs of your child in your absence. Most child ULIPs insure the parent and come with an inbuilt premium waiver benefit. Under the premium waiver benefit, if the parent dies, the plan does not stop. Instead, the insurance company pays the premium on the parent’s behalf to continue to create the corpus till maturity. On maturity, the ULIP pays a financial benefit to the child for his/her higher education, marriage, or any other financial needs.

Child ULIPs, thus, help you create a dedicated corpus for your child’s financial security.

- Pension ULIPs

These ULIPs are retirement-oriented plans that help you save up a retirement corpus. The premiums paid to get accumulated over the policy tenure attract market-linked returns. On maturity, you can withdraw a part of the corpus in cash while the remaining part is used to pay annuities. The annuities create a source of steady and guaranteed⁷ income, lifelong, thus creating a source of income after retirement.

3. Good return potential

Since ULIPs invest your premium in the capital market, you can earn market-linked returns. These returns are inflation-adjusted and help you create a good corpus. In fact, if you invest in equity-oriented funds, you can enjoy a high return potential so that you can grow your savings into a good corpus

4. Flexibility in managing the investment

ULIPs are extremely flexible plans that give you the reins to manage your investments as you see fit. Here are the flexible features that ULIPs offer –

- Policy details

You can choose the premium that you want to pay, the term, the premium paying term, and its frequency.

- Fund allocation

ULIPs offer different types of funds broadly classified as equity funds, debt funds, and balanced funds. You have the flexibility to choose the investment fund for your premium. You can select one or more funds and invest based on your risk profile and investment strategy.

- Switching

Besides allowing you to choose your investment funds, ULIPs also allow you to switch funds if needed. Switching means changing the investment funds and you can do so during the policy tenure based on the changing market dynamics and your investment needs. For instance, if you have invested in equity funds and the equity market is in turmoil, you can switch to debt funds to protect your capital and earned returns. As the markets stabilise, you can switch back to equity funds for their return potential.

- Partial withdrawals

After the first five years are over, ULIPs allow partial withdrawals from the fund value. As such, if you face any financial difficulty, you can withdraw from your ULIP’s fund value.

- Top-up premiums

Top-up premiums allow you to make additional investments into your ULIP, over and above the premium that you pay. If you want to enhance your investments, you can resort to top-ups that not only increase the fund value but also the coverage offered by the plan.

5. Tax benefits

The tax angle of a ULIP makes it all the more rewarding allowing you to create a tax-efficient corpus for your goals. Here’s a look at the overall tax benefits⁶ that ULIPs offer –

The premium that you pay towards the ULIP is allowed as a deduction from your taxable income. This deduction is allowed under Section 80C¹ up to Rs.1.5 lakhs. The deduction also lowers your tax liability.

- The premium that you pay towards the ULIP is allowed as a deduction from your taxable income. This deduction is allowed under Section 80C¹ up to Rs.1.5 lakhs. The deduction also lowers your tax liability.

- Partial withdrawals, after the lock-in period of five years, are tax-free².

- Switching between funds attracts no tax³ as you stay invested under the plan.

- The death benefit is always tax-free⁴

- In the case of maturity, if you have bought the policy before 1st February 2021 and the premium is up to 10% of the sum assured, the maturity benefit will be tax-free under Section 10(10D)⁸.

- If you buy the plan on or after 1st February 2021 and the aggregate premium under all ULIPs is up to Rs.2.5 lakhs, the maturity benefit will be tax-free under Section 10(10D)⁸.

- However, if the premium is more than Rs.2.5 lakhs, the maturity proceeds would be subject to capital gains tax⁵.

The tax benefits add to the overall benefits of ULIPs making them a must in your portfolio.

The bottom line

The unique combination of insurance and investment along with the aforementioned factors make ULIPs a must-buy. So, assess the variety of ULIPs available in the market, compare and select plans that align with your financial goals and then invest in suitable plans. Add ULIPs to your financial portfolio and enjoy the benefits that they can provide.

Table of Contents

Table of Contents