Why Start Investing From Your First Salary?

Your first salary may be Rs. 1,000 or Rs. 1,00,000. Or anything in-between, or even something higher. Irrespective of what your first income is, it is essential to set aside a little bit each month for your future goals.

Here are the top reasons to invest a portion of your income, right from your first salary itself.

- You have time on your side

The first reason to start investing early is simply the fact that you have time on your side. It goes without saying that you can save or invest more over 40 years than you can in 20 years. So, if you start investing at the age of 25, and you plan to retire at 65, you have four decades to invest for your long-term goals.

On the other hand, if you only start investing seriously at the age of 35, you have just three decades in which to invest for your life goals. This means you will have to invest a larger portion of your income to build a sizable corpus. And that may not always be feasible, particularly if you already have loans to repay by then.

- You can take on more investment risks

When you are younger, you can afford to take on more investment risks in your portfolio. This is a huge advantage because most high-risk investment options like equity and real estate have the potential to offer benchmark-beating returns. In case the markets perform well, you can benefit from the significant gains on your investment.

On the other hand, even if the markets do not perform as well as you expected them to, you have years ahead of you in which you can recover your losses and make up for them. On the other hand, if you start investing much later in life, you lose the luxury of investing in high-risk-high-return investments.

- You benefit from the power of compounding

The power of compounding essentially allows you to earn interest on your interest - or returns on your returns. Your money is reinvested in the investment vehicle, thereby leading to capital appreciation rather than mere capital preservation. And the longer you invest, the more the benefits from the power of compounding.

For instance, if you invest Rs. 1,000 per month at a compounding rate of 8%, your total investments will grow to Rs. 15 lakhs at the end of 30 years.

However, if you start investing later in life, let's say you have just 20 years to achieve the same goals. So, even if you double your monthly investment to Rs. 2,000 at 8%, you can only build a corpus of Rs. 11.86 lakhs by the end of 20 years.

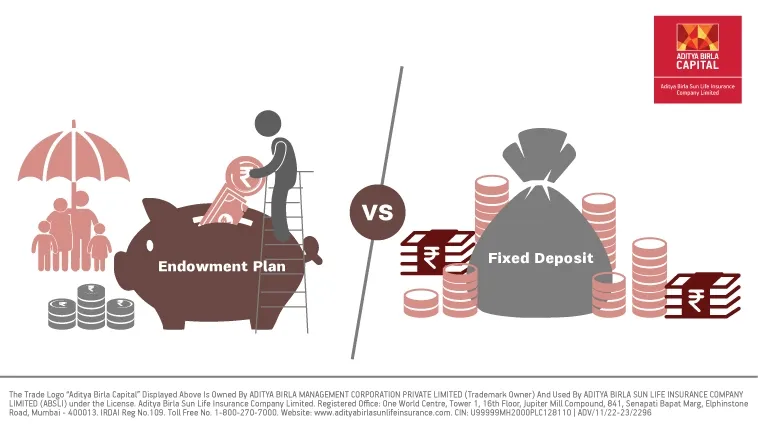

What Is An Endowment Plan?

One of the best investments to make with your first salary is an endowment plan. It is a kind of life insurance plan that combines the benefits of insurance and savings. So, like all life insurance plans, an endowment offers a life cover. This means that in case the insured person passes away during the policy term, the insurance provider pays out a death benefit to the nominee registered under the plan.

However, an endowment policy also comes with a savings component. So, if the insured person survives the maturity period, the insurer pays out maturity benefits to the policyholder. This is what makes up the savings component of an endowment plan.

The savings received at the time of maturity can be used to achieve various life goals like paying for your children's higher education, buying your dream home or even simply enhancing your retirement corpus.

This should give you a good idea of how an endowment plan works. But why does an endowment plan make for a good investment with your first salary? Let's find out more about that in the following section.

5 Reasons To Buy A Life Insurance Endowment Plan With Your First Salary

If you have just earned your first paycheck, chances are, you may already be contemplating buying a life insurance plan to protect your dependents and your future. But the question remains - what kind of insurance plan should you buy?

We think an endowment plan would make a good choice. Here are the top reasons to buy an endowment plan with your first salary.

-

Dual Benefit

The foremost reason to purchase an endowment plan with your first income is the fact it offers dual benefits. As you saw above, you get the advantage of a life cover as well as guaranteed savings. So, even if you do survive the policy term, you can rest assured that your premium payments will not have been in vain. The maturity benefits paid out by endowment plans can be a sizable addition to your corpus.

-

Financial Discipline

Merely saving up each month without having any due date to meet can be challenging for most people. It takes a great deal of discipline to be diligent with your savings. An endowment plan can help you build this effective habit of investing consistently, because you need to pay your premiums on time to keep your life cover intact. You can choose to pay your premiums on a monthly, quarterly, semi-annual or annual basis too, making it more customizable for you.

-

Low Risk

While it is true that you can afford to take on a higher degree of investment risk when you are younger, the fact remains that you need to balance your investment portfolio with some low risk investments too. An endowment plan fits the bill perfectly, since it comes with a comparatively lower level of risk. This helps minimise the overall portfolio risk while simultaneously optimising your portfolio returns.

-

Guaranteed Returns

Endowment plans offer guaranteed returns whether the insured person survives the policy term or passes away during the period. The amount of returns due are also specified at the time of purchase, so you know exactly what the outcome of your investments will be. This is in stark contrast with market-linked returns, which are neither guaranteed nor predictable. So, you can add some stability to your financial situation with an endowment plan.

-

Tax Benefits2

Another key reason to buy an endowment plan with your first salary is the fact that you get tax benefits right from the first premium you pay. As per section 80C of the Income Tax Act, 1961, the premiums you pay are deductible from your total taxable income up to Rs. 1.5 lakhs per financial year.

This effectively brings down your taxable income and therefore, your tax liability too. As you move up in your career and earn pay hikes, this tax benefit can be very useful since it lessens the burden of tax even as your tax rates increase.

Section 80 C tax benefits

Conclusion

An endowment plan has a lot to offer you, as you can see from the benefits outlined above. It's no wonder then that it makes for a very good investment, right from the time you start earning. Remember to prepare a budget and to only buy an endowment plan you can afford. That way, you reduce the risk of missing your premium payment and causing the policy to lapse.

Read Next: Life Insurance Riders You Can Consider

When you buy an endowment plan, you will also have the option to enhance the benefits offered with optional life insurance riders. What are these riders? And what are the benefits they offer? We have a blog that gives you all these answers. You can check it out to make your endowment plan more beneficial for you.

Read it here

DO YOU WANT YOUR INSURANCE BENEFITS PAID OUT AS INCOME INSTEAD OF AS A LUMP SUM AMOUNT?

The ABSLI Assured Income Plus Plan can give you exactly what you are looking for. It offers the benefit of long term income, over a period of 20, 25 or even 30 years. You only need to pay your premiums for a limited period in order to enjoy this advantage.

But that's not all. In addition to the income benefit, this plan also offers you a life cover with guaranteed# benefits and loyalty additions! So, you can put your first salary to good use by considering this life insurance plan from Aditya Birla Sun Life Insurance.

Know More

Table of Contents

Table of Contents