- All Insurance

- Endowment PlansNew

- Savings PlansNew

- Term InsuranceNew

- Pension PlansNew

- Critical Illness Insurance

- ULIP PlanNew

- Group Insurance

- Protection Solutions

- Employer Employee

- Voluntary

- Affinity

- Credit Life

- Retirement Solutions

- Annuity Scheme

- Gratuity

- Leave Encashment

- Post Retirement Medical Benefits Scheme

- Superannuation

- Withdrawn Products

- NRI PlansNew

- Articles

- Where Do I?

- Term Insurance

- Manage My Policy

- Her Insurance

Connect

Aditya Birla Sun Life Insurance Company Limited

Aditya Birla Sun Life Insurance Company Limited

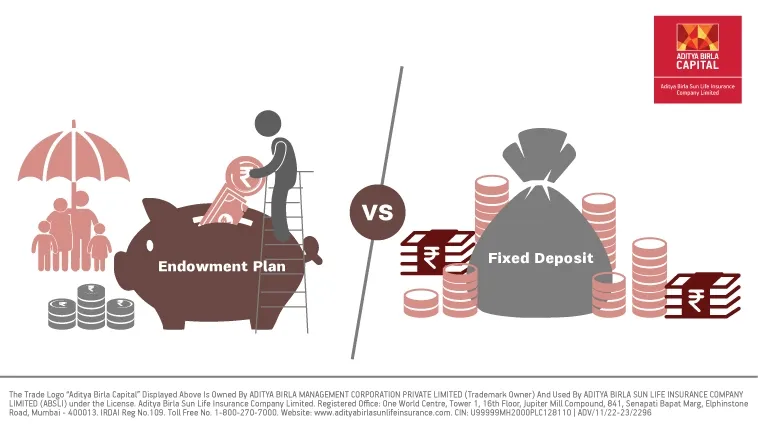

Endowment Plan vs Term Plan

Plan Smarter, Live Better!

Table of Contents

Table of Contents

How Much Helpful You Found This Article?

Rated by 0 reader

/ 5 ( reviews )

Not helpful

Somewhat helpfull

Helpful

Good

Best

Thank you for your feeback

FAQ for Term Insurance & Endowment Plan

Yes, an endowment plan provides both maturity and death benefits. If the policyholder survives the policy term, they receive a lump-sum maturity benefit, often along with bonuses. In case of the policyholder's untimely death during the policy term, the nominee will receive the death benefit, ensuring financial security for the beneficiaries.

The amount of life covered with term insurance should ideally be based on your financial obligations, future goals, and the standard of living you wish to provide for your dependents. A common rule of thumb is to have a life cover 10 to 15 times your annual income. However, considering factors like existing liabilities, future expenses (such as children's education), and inflation while deciding the cover amount is crucial.

The duration of life cover, or the policy term, is generally fixed at the inception of a term insurance policy and cannot be changed mid-term. However, some insurers offer term plans with adjustable policy terms, allowing policyholders to extend or reduce the term based on their changing needs. It's vital to check with the insurance provider for such options before purchasing the policy.

● Yes, endowment plans often come with various rider options that provide additional benefits and enhanced coverage. Common riders include: ● Accidental Death Benefit Rider: Provides an additional sum assured in case of death due to an accident. ● Critical Illness Rider: Offers a lump-sum benefit if the policyholder is diagnosed with a specified critical illness. ● Disability Rider: Provides financial support in case of permanent or temporary disability due to an accident. ● Waiver of Premium Rider: Reimburses future premiums if the policyholder is critically ill or disabled. ● Riders can be added to the base policy at an extra cost and are subject to the terms and conditions of the insurance provider.

Show All

Hide

Get immediate income payout after 1 day of policy issuance^

ABSLI Nishchit Aayush Plan

Guaranteed# income

Life Cover across policy term

Lumpsum Benefit at policy maturity, in addition to Income

Get :

₹33.74 lakhs~

Pay: ₹10K/month for 10 years

Recently Added Article

Most Popular Calculator

1Sec 10(10D) benefit is available subject to fulfilment of conditions specified therein.

2For further details regarding the above-mentioned rider, please refer to the respective rider brochure(s) available on our website.

ADV/5/22-23/252