- All Insurance

- Endowment PlansNew

- Savings PlansNew

- Term InsuranceNew

- Pension PlansNew

- Critical Illness Insurance

- ULIP PlanNew

- Group Insurance

- Protection Solutions

- Employer Employee

- Voluntary

- Affinity

- Credit Life

- Retirement Solutions

- Annuity Scheme

- Gratuity

- Leave Encashment

- Post Retirement Medical Benefits Scheme

- Superannuation

- Withdrawn Products

- NRI PlansNew

- Articles

- Where Do I?

- Term Insurance

- Manage My Policy

- Her Insurance

Connect

Aditya Birla Sun Life Insurance Company Limited

Aditya Birla Sun Life Insurance Company Limited

Types of Annuity Plans: How to Choose the Right One?

Plan Smarter, Live Better!

Table of Contents

Table of Contents

How Much Helpful You Found This Article?

Rated by 0 reader

/ 5 ( reviews )

Not helpful

Somewhat helpfull

Helpful

Good

Best

Thank you for your feeback

FAQs

An annuity plan is a financial product that guarantees a fixed income immediately or at a future date, typically after retirement.

Annuities are suitable for individuals who want to secure a stable income for their retirement, particularly those who do not have other substantial pension benefits and wish to manage the risk of outliving their savings.

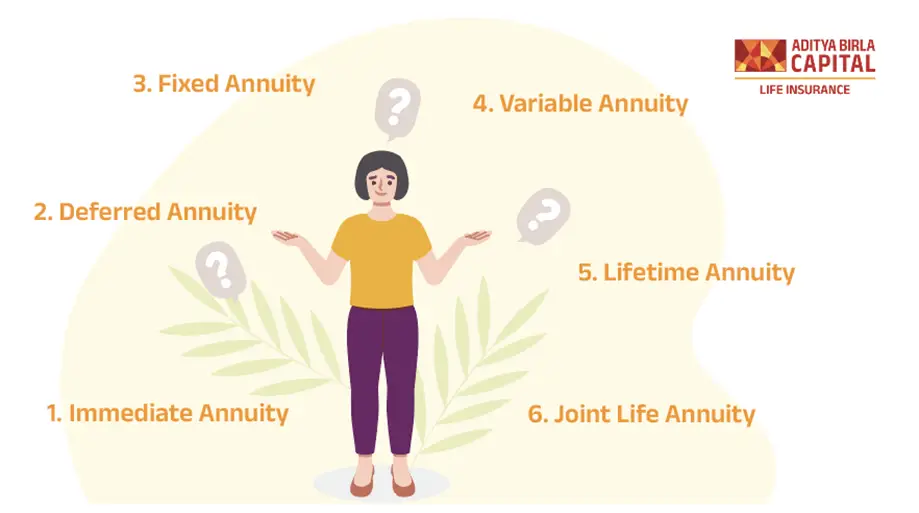

The main types of annuities include immediate annuity, deferred annuity, fixed annuity, variable annuity, lifetime annuity, and joint-life annuity.

An immediate annuity begins paying out shortly after a lump sum investment is made, ideal for those already at retirement age. A deferred annuity starts paying out at a future date, allowing your investment to grow, suited for those still in their working years.

Yes, annuity returns are taxable in India. The income from an annuity is taxed under the head "Income from Other Sources" according to the individual's applicable income tax slab rates.

Withdrawals from annuity plans before maturity can be restrictive and are usually subject to penalties. It’s important to check the specific terms and conditions of your annuity contract.

The treatment of annuity funds after the holder's death depends on the type of annuity. Some annuities offer a death benefit or return of premium to beneficiaries, while others may cease payments upon death.

Variable annuities provide payments linked to the performance of investment options chosen by the annuitant. The return can vary, offering higher potential returns but also greater risks compared to fixed annuities.

A joint life annuity continues to provide income for the surviving spouse after the death of the first spouse, ensuring that the partner is financially secure in their later years.

Yes, consulting a financial advisor is highly recommended when considering an annuity. An advisor can help you understand complex details, align the annuity with your financial goals, and choose the best type based on your circumstances.

Show All

Hide

Give ₹1 lakh/ month for 5 years and Get ₹ 4.01 lakhs every year till your life1

ABSLI Guaranteed Annuity Plus

Multiple annuity options, Regular income stream.

Guaranteed# lifelong income

Top-up option for annuity

Single/Joint Life cover option

Deferred annuity option

Give :

₹ 1 lakhs/Month for 5 year¹

Get :

₹4.06 lakhs/-

Recently Added Article

Most Popular Calculator

$For further details regarding the above-mentioned rider, please refer to the respective rider brochure(s) available on our website.

ADV/7/24-25/795