- All Insurance

- Endowment PlansNew

- Savings PlansNew

- Term InsuranceNew

- Pension PlansNew

- Critical Illness Insurance

- ULIP PlanNew

- Group Insurance

- Protection Solutions

- Employer Employee

- Voluntary

- Affinity

- Credit Life

- Retirement Solutions

- Annuity Scheme

- Gratuity

- Leave Encashment

- Post Retirement Medical Benefits Scheme

- Superannuation

- Withdrawn Products

- NRI PlansNew

- Articles

- Where Do I?

- Term Insurance

- Manage My Policy

- Her Insurance

Connect

Aditya Birla Sun Life Insurance Company Limited

Aditya Birla Sun Life Insurance Company Limited

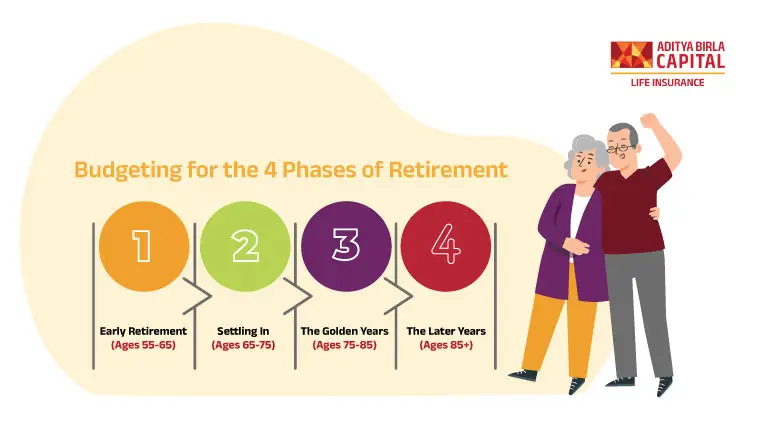

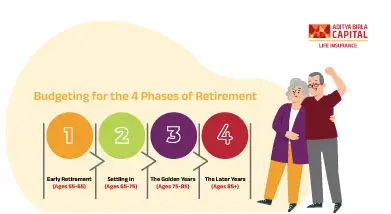

Budgeting for the 4 Phases of Retirement

Plan Smarter, Live Better!

Table of Contents

Table of Contents

How Much Helpful You Found This Article?

Rated by 0 reader

/ 5 ( reviews )

Not helpful

Somewhat helpfull

Helpful

Good

Best

Thank you for your feeback

Budgeting for the 4 Phases of Retirement FAQs

There's no one-size-fits-all answer. It depends on your desired lifestyle, healthcare needs, and planned activities. An ABSLI advisor can help you estimate your retirement expenses and create a personalized budget.

Not necessarily, especially in the initial years. However, review your budget and eliminate unnecessary expenses to free up funds for potential healthcare costs or travel.

Factor in health insurance premiums and potential out-of-pocket expenses. Consider health insurance, if eligible, to save for healthcare costs tax-efficiently.

Research assisted living or nursing home costs in your area. Explore long-term care insurance options if possible, and factor potential costs into your budget for later retirement phases.

Review your budget at least annually. Do it more frequently if your healthcare needs change, you experience a significant life event, or economic conditions shift.

Research Social Security, Medicare, and Medicaid eligibility requirements. Explore additional programs you might qualify for based on your income and circumstances.

ABSLI advisors can assess your financial situation, analyze your income sources and expenses, and develop a personalized budget that aligns with your desired lifestyle throughout retirement.

ABSLI advisors can help you explore options like delaying Social Security benefits, optimizing your withdrawal strategy, or finding part-time work to supplement your income.

Absolutely not! Developing a budget and saving habits early allows you to track expenses, identify areas for improvement, and plan for a more secure retirement.

ABSLI advisors offer expertise and objectivity to create a realistic and flexible budget. They can help you account for future uncertainties and adapt your plan as needed, ensuring your golden years remain financially secure.

Show All

Hide

Give ₹1 lakh/ month for 5 years and Get ₹ 4.01 lakhs every year till your life1

ABSLI Guaranteed Annuity Plus

Multiple annuity options, Regular income stream.

Guaranteed# lifelong income

Top-up option for annuity

Single/Joint Life cover option

Deferred annuity option

Give :

₹ 1 lakhs/Month for 5 year¹

Get :

₹4.06 lakhs/-

Recently Added Article

Most Popular Calculator

%Tax benefits are subject to changes in tax laws. Kindly consult your financial advisor for more detail.

ADV/4/24-25/79