Why Updating Your Nominee is Important

Life is full of changes—marriage, children, aging parents, or even a shift in financial planning. While we diligently update addresses, contact numbers, and bank details, one critical detail often gets overlooked—our life insurance policy details.

Your nominee is the person who will receive the policy benefits in case of an unfortunate event. But what if the nominee you originally named is no longer the best choice? Maybe you've gotten married and want to include your spouse, had children and want to secure their future, or need to remove someone due to changed circumstances. Updating your nominee ensures that your loved ones are financially protected, just as you intended under your life insurance plan.

Yet, many policyholders forget to review this simple but crucial detail. And when the time comes, an outdated nominee can lead to unnecessary complications, delays, and legal hurdles for your family.

When Should You Update Your Nominee?

You should consider updating your nominee in these situations:

Marriage or Divorce – If your spouse wasn’t originally added or if you need to change your nominee after a separation.

Birth of a Child – To ensure your children are financially secure under the best life insurance policy in India.

Loss of an Existing Nominee – If your original nominee has passed away.

Aging Parents – If they are no longer financially dependent on you.

Change in Financial Plans – If you wish to designate a trust or a different family member as the beneficiary.

Failing to update your nominee could mean that your hard-earned savings from your life insurance plan don’t go to the right person when they need it the most.

How to Update Your Nominee

Step 1:

Open the Aditya Birla Sun Life Insurance website : https://lifeinsurance.adityabirlacapital.com/

Step 2:

Click on ‘Manage My Policy’ tab on the top right of your screen

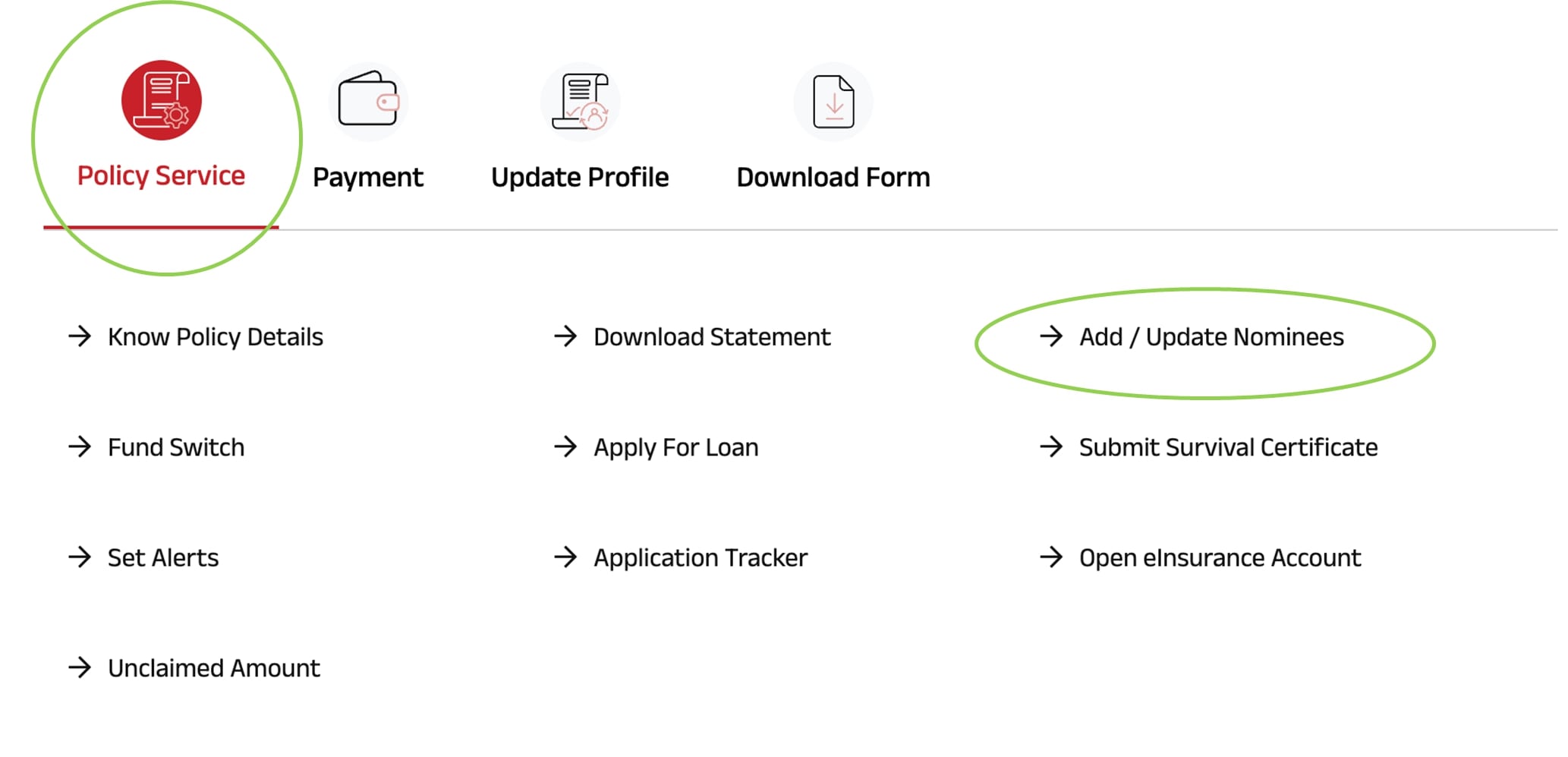

Step 3:

Under the policy service tab you will see ‘Add/Update Nominee’ option. Click on it.

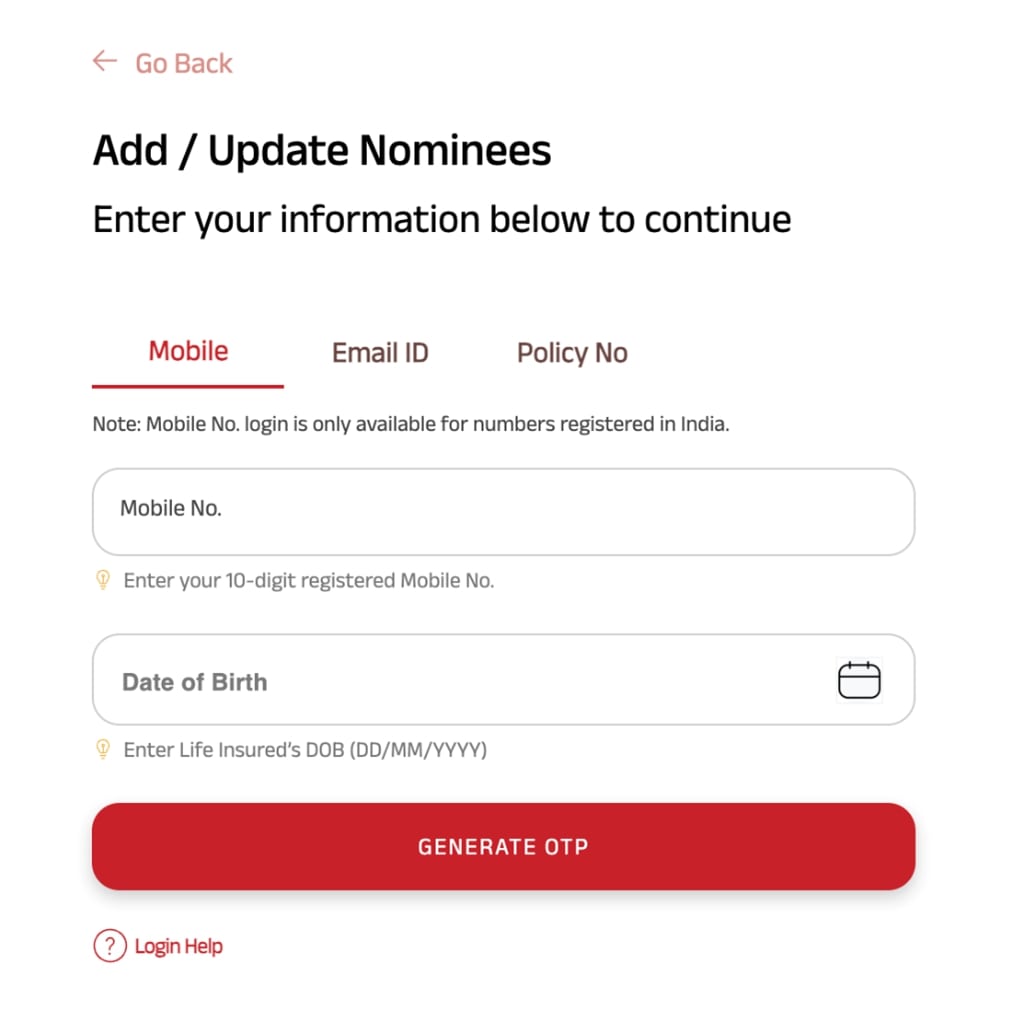

Step 4:

Now you will see a small form asking for your details. Enter your details, generate the OTP and then edit/add Nominees to your Life Insurance policy details.

Common Mistakes To Avoid While Choosing A Nominee -

Here are some of the most common mistakes you need to avoid when appointing a new nominee for your life insurance policy -

-

Not Updating Nominee’s Details

You must update the nominee’s existing details such as name, address and other relevant information regularly. in case these details change in the future, you should update the insurer and if the existing nominee passes away during the policy tenure, make sure you update that detail as well and assign a new nominee.

-

Assigning Only One Nominee

Many people make the mistake of naming only one nominee. The claim settlement process can face a roadblock if you fail to update the nominee details after the existing nominee dies unexpectedly. This is because the insurer may find it difficult to identify the insured's legal heir. Hence, you should update the insurer if the nominee passes away, especially if there's only one nominee. Or you can appoint more than one nominee and also allocate a certain percentage of the sum assured to each - thereby preventing this needless delay in the future.

-

Not Informing the New Nominee

Make sure you inform the new nominee that they’ve been nominated. Also, share the policy documents with them so they’ll be able to file the claim in the future - with all details upfront.

-

Not Appointing A Custodian

In the absence of an appointed custodian, the claim process for the minor nominee (less than 18 years old) cannot proceed, and the minor cannot make use of the death benefit. It is therefore crucial that you not only appoint a custodian but also provide the insurance provider with fully verified details of the custodian.

-

Mentioning A Legal Heir Who Is Not Your Nominee

If you want to appoint a nominee who isn’t your legal heir, your legal heir will have precedence over them to claim the death benefit. Hence, make sure you draw up a will that gives the nominee you appoint absolute authority over the death benefit.

What Happens If You Don’t Update Your Nominee?

Many policyholders assume that their life insurance payout will automatically go to their legal heirs. However, an outdated or incorrect nominee can create legal disputes, delays in claim settlement, and financial stress for your loved ones. In cases where a nominee is no longer valid or alive, the claim process can become lengthy and complex, often requiring legal intervention.

Common Myths About Nominee Updates

• “I named a nominee once; that’s enough.” – Life changes, and so should your policy details. Regular updates ensure your money reaches the right person.

• “My legal heir will automatically get the benefit.” – Not always! If your nominee isn’t updated, your family might face legal hurdles.

By keeping your nominee details current, you’re ensuring a smooth financial transition for those who depend on you.

Summary

Your life insurance policy is more than just a policy—it’s a promise to your family’s future. And just like any promise, it needs to be kept up-to-date.

A quick nominee update today could save your loved ones from unnecessary stress tomorrow. So, take a few minutes to check your life insurance policy details, make the necessary changes, and rest assured that your financial safety net is secure for the people who matter the most.

Table of Contents

Table of Contents