- All Insurance

- Endowment PlansNew

- Savings PlansNew

- Term InsuranceNew

- Pension PlansNew

- Critical Illness Insurance

- ULIP PlanNew

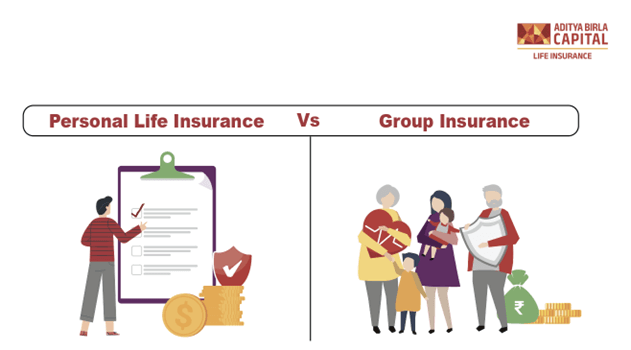

- Group Insurance

- Protection Solutions

- Employer Employee

- Voluntary

- Affinity

- Credit Life

- Retirement Solutions

- Annuity Scheme

- Gratuity

- Leave Encashment

- Post Retirement Medical Benefits Scheme

- Superannuation

- Withdrawn Products

- NRI PlansNew

- Articles

- Where Do I?

- Term Insurance

- Manage My Policy

- Her Insurance

Connect

Aditya Birla Sun Life Insurance Company Limited

Aditya Birla Sun Life Insurance Company Limited

Beginners Guide To A Healthy Life Insurance Portfolio

Plan Smarter, Live Better!

Table of Contents

Table of Contents

How Much Helpful You Found This Article?

Rated by 0 reader

/ 5 ( reviews )

Not helpful

Somewhat helpfull

Helpful

Good

Best

Thank you for your feeback

Buy ₹1 Crore Term Insurance at Just ₹575/month*

ABSLI Super Term Plan

Term plan designed for salaried individual.

3 Plan Options

Health Management Service Worth ₹74000

100% return of premium

Life Cover

₹1 crore

Premium:

₹575/month*

Recently Added Article

Most Popular Calculator

@In the Unit Linked Policy, the investment risk in the investment portfolio is borne by the Policyholder.

#Provided all due premiums are paid.

%Tax benefits are subject to changes in tax laws. Kindly consult your financial advisor for more detail.