- All Insurance

- Endowment PlansNew

- Savings PlansNew

- Term InsuranceNew

- Pension PlansNew

- Critical Illness Insurance

- ULIP PlanNew

- Group Insurance

- Protection Solutions

- Employer Employee

- Voluntary

- Affinity

- Credit Life

- Retirement Solutions

- Annuity Scheme

- Gratuity

- Leave Encashment

- Post Retirement Medical Benefits Scheme

- Superannuation

- Withdrawn Products

- NRI PlansNew

- Articles

- Where Do I?

- Term Insurance

- Manage My Policy

- Her Insurance

Connect

Aditya Birla Sun Life Insurance Company Limited

Aditya Birla Sun Life Insurance Company Limited

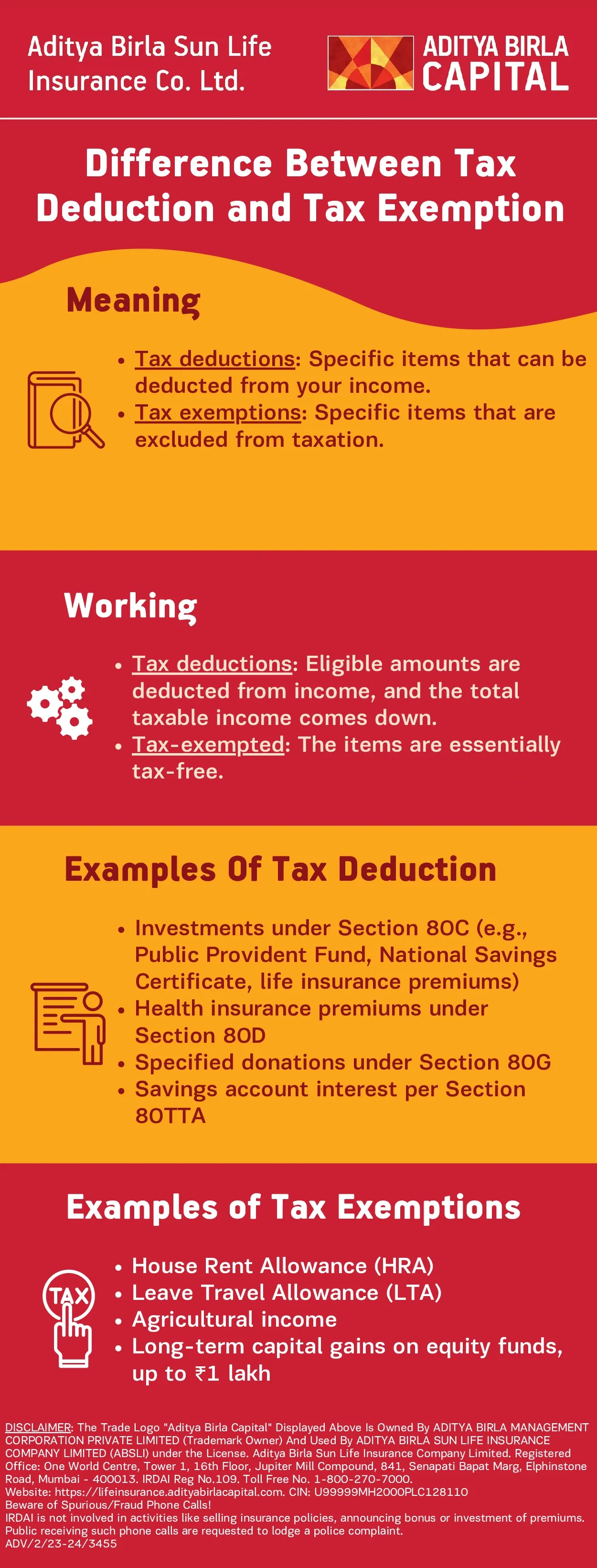

Difference Between Tax Deduction and Tax Exemption

Plan Smarter, Live Better!

Table of Contents

Table of Contents

Conclusion

How Much Helpful You Found This Article?

Rated by 0 reader

/ 5 ( reviews )

Not helpful

Somewhat helpfull

Helpful

Good

Best

Thank you for your feeback

Buy ₹1 Crore Term Insurance at Just ₹575/month1

ABSLI DigiShield Plan

Life cover up to 100 years of age.

Joint Cover Option

Inbuilt Terminal Illness Benefit

Tax Benefit^

Return of Premium Option~

Life Cover

₹1 crore

Premium:

₹575/month1

Most Popular Calculator

ADV/2/23-24/3689