- All Insurance

- Endowment PlansNew

- Savings PlansNew

- Term InsuranceNew

- Pension PlansNew

- Critical Illness Insurance

- ULIP PlanNew

- Group Insurance

- Protection Solutions

- Employer Employee

- Voluntary

- Affinity

- Credit Life

- Retirement Solutions

- Annuity Scheme

- Gratuity

- Leave Encashment

- Post Retirement Medical Benefits Scheme

- Superannuation

- Withdrawn Products

- NRI PlansNew

- Articles

- Where Do I?

- Term Insurance

- Manage My Policy

- Her Insurance

Connect

Aditya Birla Sun Life Insurance Company Limited

Aditya Birla Sun Life Insurance Company Limited

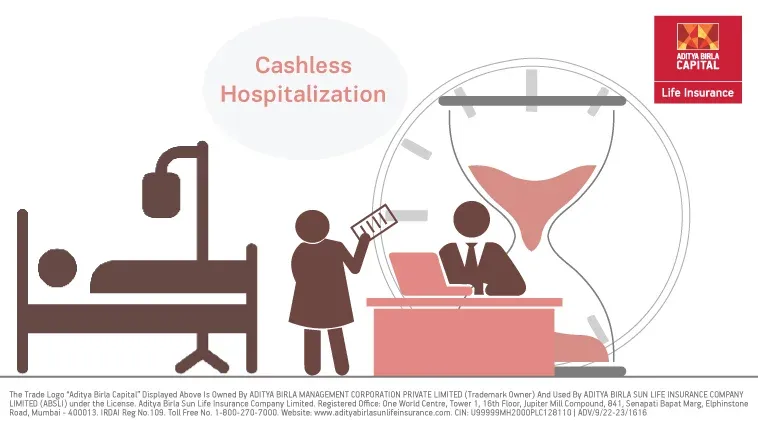

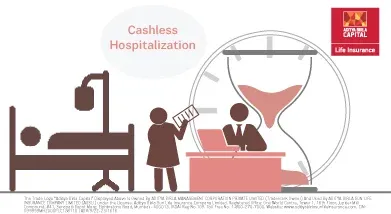

What Is a Cashless Hospitalisation Facility In Health Insurance?

Plan Smarter, Live Better!

Table of Contents

Table of Contents

How much helpful you found this article?

Rated by 0 reader

/ 5 ( reviews )

Not helpful

Somewhat helpfull

Helpful

Good

Best

Thank you for your feeback

FAQ Cashless Hospitalisation

Cashless health insurance is important because it provides immediate access to medical treatment without the need for upfront payment. This can be crucial during emergencies, ensuring that financial constraints do not delay or hinder necessary medical care for you and your loved ones.

Cashless health insurance is a feature that can be included in various types of policies, including individual and family floater plans. The key difference lies in the coverage and beneficiaries: individual plans cover only one person, while family floater plans extend coverage to the entire family under a single sum insured.

The tenure of a cashless health insurance policy is usually one year, after which the policy needs to be renewed. Some insurers may offer longer tenure options or multi-year policies.

Yes, most cashless health insurance policies cover pre-existing illnesses, but there is usually a waiting period before the coverage is applicable. This waiting period can vary from one policy to another, typically ranging from 2 to 4 years.

Most cashless health insurance policies can be renewed indefinitely, providing lifelong coverage. However, there may be change in terms of renewal and premium or coverage periodically and should be reviewed at each renewal.

Show All

Hide

Give ₹1,00,000 for 6 years

and Get ₹14.48 lakhs#

ABSLI Akshaya Plan

Whole Life Insurance with Cash Bonus

Flexible Bonus Payouts

Two options for benefit payouts

Life Cover

Tax Benefits

Give:

₹1 lakh for 6 years

Get:

₹14.48 lacs#

Recently Added Article

Most Popular Calculators

Most Read Articles

How to Calculate Gratuity for Private Sector Employees How to Calculate Gratuity for Private Sector Employees How to Calculate Gratuity for Private Sector Employees How to Calculate Gratuity for Private Sector Employees How to Calculate Gratuity for Private Sector Employees How to Calculate Gratuity for Private Sector Employees