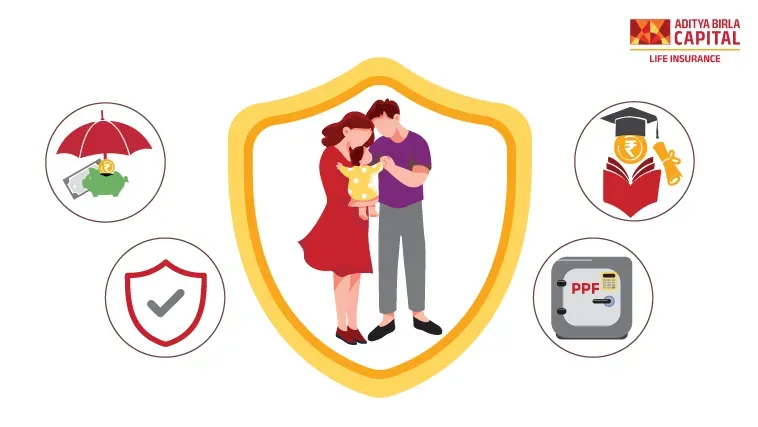

Ever since your child was born, you have done everything in your power to keep your child happy and satisfied. You encourage them to dream big, and no dream is so big that you cannot make it come true but at the same time, higher education expenses continue to climb at astonishing rates per year at an estimated 15 to 20% every year. It is important to look up suitable child investment planswhile your child is still young. Consider the following.

Child education insurance plan

Child insurance plans help pay the high costs of future education, even if the parent is absent from the child's life. It is designed to take care of higher education costs. If the child loses their parent before the plan matures, the child insurance plan provider will normally waive off the remaining premiums but keep the policy active.

Sukanya Samruddhi Scheme

This is a Government-floated savings scheme for the girl child in India. Parents of girl children are encouraged to save for their daughters by opening an account and depositing money in it for a period of 14 years. The deposit limits are Rs 1,000 (minimum) and Rs 1.5 lakh (maximum) per year. The deposit matures 21 years after the date of starting the account, and earns a high interest rate of 9.2%.

Personal term insurance

Perhaps the best investment for your child comes from ensuring that their dreams are taken care of in large measure even in your absence. Taking a term insurance policy is the best way to safeguard your child's higher education dreams. The high sum assured provided by the life insurance pays for your child's every need, apart from making provisions for their wedding as well.

PPF

This is one of the most reliable investments for your child. You can open a Public Provident Fund (PPF) account in your child's name from a bank that offers PPF services. The minimum yearly deposit per year is Rs 500, while the maximum is Rs 1.5 lakh. The money is deposited for a period of 15 years, while partial withdrawals are allowed after the seventh year of the deposit has elapsed. PPF pays interest at 8.5%.

Short term funds

It is always advisable to have a long window of maturity when investing for your child's education, but there are short-term education-related expenses such as paying school fees for secondary school, clothes and books, etc. which can be paid from debt instruments like short term funds and bond funds with a lower maturity tenure. You can expect returns in the range of 6 to 8% for these instruments.

Table of Contents

Table of Contents