- All Insurance

- Endowment PlansNew

- Savings PlansNew

- Term InsuranceNew

- Pension PlansNew

- Critical Illness Insurance

- ULIP PlanNew

- Group Insurance

- Protection Solutions

- Employer Employee

- Voluntary

- Affinity

- Credit Life

- Retirement Solutions

- Annuity Scheme

- Gratuity

- Leave Encashment

- Post Retirement Medical Benefits Scheme

- Superannuation

- Withdrawn Products

- NRI PlansNew

- Articles

- Where Do I?

- Term Insurance

- Manage My Policy

- Her Insurance

Connect

Aditya Birla Sun Life Insurance Company Limited

Aditya Birla Sun Life Insurance Company Limited

Module 03 | Chapter: 24

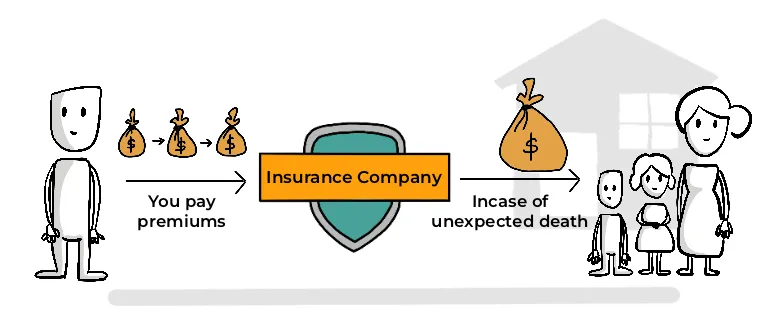

Ch. 24: Whole Life Term Insurance

What is Term Insurance? - Definition & MeaningWhen To Buy Term Plan?Why Should You Buy Term PlanWho Should Buy Term InsuranceWhere to Buy Term Insurance From?How to Buy Term Insurance?How Much Term Insurance Cover Do I Need?Saral Jeevan Bima?Term Life Insurance Riders?Term Insurance ExclusionsTerm Insurance Claims Process?Customization in Term Plans?Benefits of buying Term InsuranceDecreasing Term InsuranceGroup Term InsuranceMarried Women’s Property ActClaim payout optionsEligibility RequirementsHow Does It Work?Increasing CoverLife Stage BenefitThings To Keep In Mind IGTypes of Term Insurance PlansWhole Life Term InsuranceTerm Insurance Tax Benefits*

Key takeaways from this chapter

Key takeaways from this chapter

Looking to buy Term Plan

ABSLI Salaried Term Plan

Exclusively For Salaried Individuals

Optional Accelerated Critical Illness benefit

Inbuilt Terminal Illness Benefit

Life Cover upto 75 years

4 Plan Options

Life Cover

₹1 crorePremium:

₹576/month*ABSLI Salaried Term Plan (UIN:109N141V05) is a non-linked non-participating individual pure risk premium life insurance plan; upon Policyholder’s selection of Plan Option 2 (Life Cover with ROP) this product shall be a non-linked non-participating individual savings life insurance plan.

*LI Age 21, Male, Non Smoker, Option 1: Life Cover, PPT: Regular Pay, SA: ₹ 1 Cr., PT: 10 years, Annual Premium: ₹ 6400/- ( which is ₹ 576/month) Premium exclusive of GST. On death, 1 Cr SA is paid and the policy terminates.

ADV/4/23-24/72

Plan Smarter, Live Better!