- All Insurance

- Endowment PlansNew

- Savings PlansNew

- Term InsuranceNew

- Pension PlansNew

- Critical Illness Insurance

- ULIP PlanNew

- Group Insurance

- Protection Solutions

- Employer Employee

- Voluntary

- Affinity

- Credit Life

- Retirement Solutions

- Annuity Scheme

- Gratuity

- Leave Encashment

- Post Retirement Medical Benefits Scheme

- Superannuation

- Withdrawn Products

- NRI PlansNew

- Articles

- Where Do I?

- Term Insurance

- Manage My Policy

- Her Insurance

Connect

Aditya Birla Sun Life Insurance Company Limited

Aditya Birla Sun Life Insurance Company Limited

Module 03 | Chapter: 12

Ch. 12: Customization in Term Plans?

What is Term Insurance? - Definition & MeaningWhen To Buy Term Plan?Why Should You Buy Term PlanWho Should Buy Term InsuranceWhere to Buy Term Insurance From?How to Buy Term Insurance?How Much Term Insurance Cover Do I Need?Saral Jeevan Bima?Term Life Insurance Riders?Term Insurance ExclusionsTerm Insurance Claims Process?Customization in Term Plans?Benefits of buying Term InsuranceDecreasing Term InsuranceGroup Term InsuranceMarried Women’s Property ActClaim payout optionsEligibility RequirementsHow Does It Work?Increasing CoverLife Stage BenefitThings To Keep In Mind IGTypes of Term Insurance PlansWhole Life Term InsuranceTerm Insurance Tax Benefits*

Key takeaways from this chapter

Key takeaways from this chapter

Customize Term Insurance Plans

- Premium Payment Frequency

- Payout Options

- Premium Pay Model

- Riders

Premium Payment Frequency

Claim Payout Options

Premium Pay Model

- Want to get the payment liability off your chest quickly.

- Have, or expect to have unpredictable income in the future (eg - if you’re self-employed or a businessperson).

- Want to take an ultra long-term cover, beyond retirement age

Does Limited Pay save money?

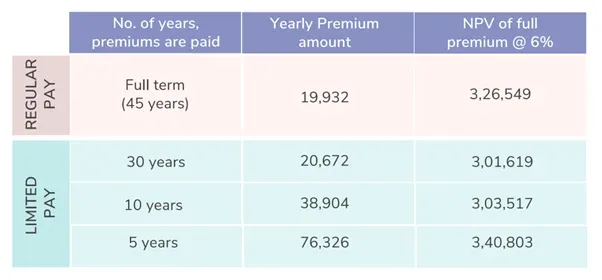

The usual argument is that the sum of the premiums you pay in Limited Pay is lower than the aggregate premium you pay in the case of a regular payment term. But this calculation does not take into account the 'time value of money'. When we calculate the Net Present Value of the premium paid in both the cases, the answer could vary depending on the insurer and the payment term.

Let us explain with an example -

Raman is a Male, 30 year old, non-smoker who is buying a Rs. 1 Crore policy until age 75. Here is the comparison of the present value of premiums he will pay in both cases - Limited pay and Regular pay.

- Use the Limited Pay option if it is a strong preference based on your financial life. For example, if you think your business income can be very erratic in the future

- Do not blindly follow any thumb-rules. Ask your advisor to calculate NPV on the cash outlays before taking a decision.

Insurance Riders

- Critical illness rider

- Accidental death benefit rider

- Waiver of premium rider

- Accidental disability rider

You will find alternatives to most riders that can provide more comprehensive coverage - but, at a higher overall cost.

Like for example, the Critical Illness rider can be a cheaper alternative to a comprehensive critical illness cover which can become very expensive in the long term. However, the Rider might have limitations such as only providing a cover in case of advanced stages of the disease, etc.

You should read our detailed article on Riders before you make a decision on which Riders to pick, and which ones to skip.

Looking to buy Term Plan

ABSLI Salaried Term Plan

Exclusively For Salaried Individuals

Optional Accelerated Critical Illness benefit

Inbuilt Terminal Illness Benefit

Life Cover upto 70 years

4 Plan Options

Life Cover

₹1 crorePremium:

₹576/month*ABSLI Salaried Term Plan (UIN:109N141V04) is a non-linked non-participating individual pure risk premium life insurance plan; upon Policyholder’s selection of Plan Option 2 (Life Cover with ROP) this product shall be a non-linked non-participating individual savings life insurance plan.

*LI Age 21, Male, Non Smoker, Option 1: Life Cover, PPT: Regular Pay, SA: ₹ 1 Cr., PT: 10 years, Annual Premium: ₹ 6400/- ( which is ₹ 576/month) Premium exclusive of GST. On death, 1 Cr SA is paid and the policy terminates.

ADV/4/22-23/79

Plan Smarter, Live Better!