Imagine you want to purchase an Air conditioner. Various types of air conditioners are available in the market, including split ACs, window ACs, and portable air conditioners. They differ in terms of their features, such as energy efficiency, cooling capacity, etc. Typically, you zero in on the type based on certain factors like room size, your budget etc. - to make the purchase worth your money and effort. Right?

Likewise, there are a variety of money-back plans designed to serve your needs. Since each individual's needs differ, these plans are tailored to best meet your requirements. It is imperative to know the key attributes of each of the types to be able to make an informed decision.

Without further ado, let's explore the different types of Money-back Plans.

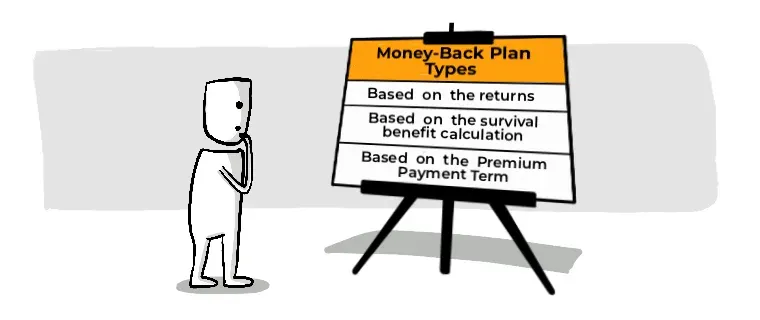

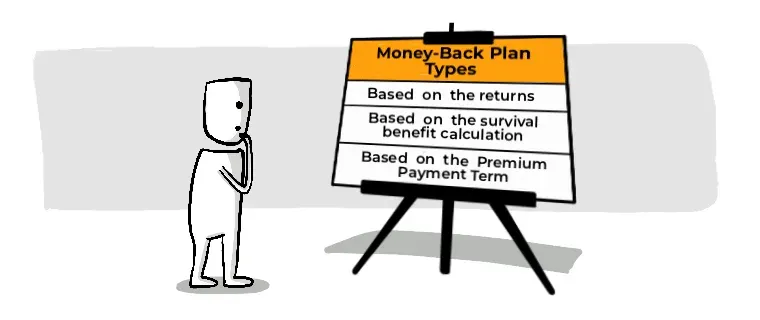

Types of Money-Back Plans

Money-back plans can be classified based on the returns you receive and the survival benefit calculation. Let's have a look.

Based on the returns

A money-back plan can be either Participating or Non-Participating.

Participating Money-Back plans

Under this policy, you will receive a variable bonus in addition to the guaranteed² returns. As the term implies, you participate in the company's profits which are distributed as bonuses or dividends. Your premiums are placed in different types of debt investments like government securities, corporate bonds, etc. The profits gained from these investments are given to you as bonuses.

Non-participating money-back plans

Non-Participating Money-back plans, comparatively, are very basic. They provide guaranteed² fixed benefits, i.e., the payout at the end of the policy term or in the event of the policyholder’s death. You do not participate in the insurance company's profits, i.e. you don't have any share in the company's profits. As a result, you are not entitled to a bonus.

Based on the survival benefit calculation

As long as all the premiums are paid on time, you'll get a specific percentage of either the annual premium or the sum assured back at regular intervals depending on the policy you choose. The policy can either be a sum assured front money-back plan or a premium front money-back plan.

Sum assured Front Money-back plan.

In this plan, you choose the sum assured first and then the premium is calculated accordingly. The survival benefit is a certain percentage of your sum assured, say 20%, etc. You will receive the survival benefit as per the predefined schedule laid down in the policy document. These regular payouts act as guaranteed1 side income that can be used to cover key milestones or goals in your life, such as EMI payments, education fees etc.

For example,

In 2022, Raj buys a Money-back policy with Rs 20 Lakhs coverage for a policy period of 25 years. The premium payment term is 10 years. He shall receive 10% of the sum assured every year for 10 years after the premium payment period is over.

- So, from the 11th year, i.e. 2031, he shall get a survival benefit of Rs 2,00,000.

10% of 20,00,000 = Rs 2,00,000.

- He shall get Rs 2,00,000 every year for the next ten years, i.e. till 2040.

- He shall receive the maturity benefit too in 2045.

- The death benefit will be paid to his nominee if Raj passes away during the policy term. It is exclusive of the survival benefit.

Premium front money-back plan

In premium front plans, you decide the premium amount you can invest and the sum assured is calculated accordingly. The survival benefit is a percentage of the premiums you pay each year. It depends on various factors like your age, gender, premium payment term, etc. You will receive the survival benefit as per the predefined schedule laid down in the policy document. These regular payouts act as guaranteed1 passive income.

Example - Kunal purchases a premium front money-back plan in 2022 and chooses to pay Rs 1 lakhs as the premium each year for the next 15 years. The sum assured will be calculated accordingly. The Survival benefit is equal to 10% of the annual premium paid and will be paid over a span of 10 years after the premium payment term ends. The policy term is 25 years.

- So, from the 11th year, i.e. 2031, he shall get a survival benefit of Rs 10,000 per year till 2040.

10% of 1,00,000 = Rs 10,000

- He shall receive the maturity benefit too in 2046.

- The death benefit will be paid to his nominee if Kunal passes away during the policy term. It is exclusive of the survival benefit.

Based on Premium Payment Term

Level Payment Money-back Policy

Depending on your income and comfort, you may pay the premium monthly, quarterly, or semiannually. In this plan, the premium is determined based on the duration of the policy you choose, and the amount will stay the same throughout the policy period.

The death benefit will be paid to your nominee if you pass away during the policy term. If you survive the policy term, the policy will pay you the maturity benefit.

Limited Payment Money-Back Policy

This plan requires you to pay premiums for a specified period of time. You are covered financially until the policy expires. The premium can be paid monthly, quarterly, half-yearly, or annually based on your convenience.

Instead of continuing to pay the premium until the end of the policy period, you can choose to pay them in faster, larger instalments. You can benefit from this type of plan if you believe you won't be financially stable later, for instance, if you're self-employed.

For example,

35-year-old Maneesh purchased a money-back plan with coverage of Rs 25 lakhs over a policy term of 25 years. He will need to pay a premium of Rs 35,000 per year for 25 years. Since he will retire at 50, he decides to finish paying the premiums within 15 years to avoid shouldering the financial burden in the future. His monthly payments will be adjusted accordingly.

Now that you are aware of all the types of money-back plans and their unique features, we are confident that you can go ahead and select the right one that best suits your needs. Ensure that you customise the plan according to your preferences in terms of the premium payment period, payouts, etc., to avoid financial hassles in the future. Read on to know more about the customisation options available!

Key takeaways from this chapter

Key takeaways from this chapter