Home Loans

Home Loans

Personal

Loans

Personal

Loans

SME Loans

SME Loans

Business Loans - Udyog

Plus

Business Loans - Udyog

Plus

Loan against Securities

Loan against Securities

Mutual Funds

Mutual Funds

Stock and

Securities

Stock and

Securities

Portfolio

Management Services

Portfolio

Management Services

Pension Funds

Pension Funds

Life

Insurance

Life

Insurance

Health

Insurance

Health

Insurance

Wellness

Solutions

Wellness

Solutions

Pay Bills

Pay Bills

Pay anyone

Pay anyone

Pay on call

Pay on call

Payment

Lounge

Payment

Lounge

ABC Credit

Cards

ABC Credit

Cards

1800-270-7000

1800-270-7000

FAQs

Have questions? We’ve got the answers.

-

To whom will the claim money be paid?

The claim money will be paid to the beneficiary who generally is the nominee / assignee / appointee (in case of a minor) as mentioned by the Life Assured in the Application Form for Insurance.

-

What happens if there is no nomination on death of the Life Assured? Or What happens if both the Life Assured and the Nominee expires in the same event?

In such an eventuality, a "Succession Certificate" will have to be submitted by the Claimant. A Succession Certificate is issued on application by a competent court on the question of the right to the property of the deceased. The Succession Certificate should specifically provide for disbursement of policy monies. If, however, the deceased has left a will, a probate of the will is required along with the copy of the will.

-

If the nominee dies during the tenure of the Policy, what action should be taken by the Life Assured?

The Life Assured should nominate some other person in place of the deceased Nominee under section 39 of the Insurance Act.

-

After how many days from the date of an incident should a claim be intimated?

Except in some type of claims (e.g. Critical Illness Rider), where a waiting period is involved, all claims including death claims should be intimated as soon as possible.

-

Who should inform ABSLI about the claim and how?

The claimant or the family members of the Life Assured should inform the ABSLI Branch Office about the death of the Life Assured. Alternatively, they can directly intimate the Claims Section at:

The Claims Section,

Aditya Birla Sun Life Insurance Company Limited

G Corp Tech Park,

5th & 6th Floor,

Kasar Wadavali, Ghodbunder Road,

Thane - 400 601. -

Where should one submit the claim forms?

The claim forms can be submitted at the nearest ABSLI Branch Office or could be sent directly to the Claims Section at:

The Claims Section,

Aditya Birla Sun Life Insurance Company Limited

G Corp Tech Park,

5th & 6th Floor,

Kasar Wadavali, Ghodbunder Road,

Thane - 400 601. -

All you need to know about Grief Counselling

Losing someone is a difficult time for anyone. At such times, it may help to talk to empathetic experts who can help cope with loss. With this in mind, we at Aditya Birla Sun Life Insurance (ABSLI), offer a wellness program in partnership with MPower. Through this program, nominees or family members of the insured can opt for grief counselling sessions after their demise. During these sessions, a trained team of professionals will guide and help them cope with loss and emerge stronger. Through this first-of-its-kind program, we have already helped 100+ families overcome their grief.

-

All you need to know about our Sapling Plantation program

To honor the memory of the members of our life insurance family, we plant a tree for every deceased member in the Sundarbans Forest. The nominee and the family members get a certificate along with pictures of the sapling planted in the name of the insured. So far, we have successfully planted 3,500 trees through Grow Tree since the inception of the initiative.

-

Exclusions not covered by life insurance policies

Deaths due to the below causes are usually not covered by life insurance policies:

1) Pre-existing diseases

2) Suicide

3) Adventure sports like skydiving

4) War/war-related acts

5) Pregnancy or pregnancy-related complications

6) Participation in illegal, unlawful or criminal activities like driving under the influence of drugs or alcohol

7) Incorrect or wrong information declared during life insurance application like wrong age, smoking habits, medical information, etc.

Life insurance policies can also have other exclusions, which can differ from policy to policy. Read the policy document carefully to understand what is covered and what is not. -

How are Life insurance payouts taxed?

There are three types of life insurance payouts: Claims, maturity payouts and bonus payouts.

Claim payouts, often called the death benefit, are paid out after the demise of the insured. These payouts are usually exempt from income tax. However, the total sum assured should be at least 10 times that of the annual premium. Otherwise, a TDS (Tax Deducted at Source) of 1% will be levied.

Maturity and bonus payouts can also be exempt from any income tax if it follows the below terms:

- For policies issued before 1st April 2012: The premium paid on the policy is less than 20% of the sum assured

- For policies issued after 1st April 2012: The premium paid on the policy is less than 10% of the sum assured

You can read the details of the exemptions under Section 10(10D) of the Income Tax Act. -

How do I communicate my concerns in connection with a Claim decision

We have a Grievance Redressal Committee that is chaired by an internal and external member. If you wish to represent your case, you can send a letter addressed to the committee at the address given below:

Claims Grievance Redressal Committee

The Claims Section,

Aditya Birla Sun Life Insurance Company Limited

G Corp Tech Park,

5th & 6th Floor,

Kasar Wadavali, Ghodbunder Road,

Thane - 400 601

Considering all the facts and circumstances, the committee takes a decision on every representation. -

How the Claimant will come to know that the claim proceeds has been electronically transferred to Customer’s Account?

Once the payment is credited to the Beneficiary's Account successfully, Claims Dept would send a communication letter and mailer to the Customer with the details of the electronic transfer.

-

If Claimant wants to re-issue the cheque which has become stale, then what all the documents should be submitted to process the re-issuance of the cheque or to transfer the claim proceeds electronically?

Claimant should submit the Original cheque along with the written statement stating the reason for re-issuance and payment option alongwith the documentary proof of Bank details to nearest Aditya Birla Sun Life Insurance Branch.

Ps: For cases wherein cheque is lost then requirement of Original cheque is not applicable. -

What are the IRDAI regulations pertaining to Claims?

The IRDAI (Insurance Regulatory and Development Authority of India) guidelines state that a claim will have to be paid within 30 days from the date of receipt of all claim documents.

In case the claim warrants an investigation, then the insurance company has to complete the investigation not later than 120 days from the time of making the claim.

Moreover, if a claim is ready for payment but the payment cannot be made because of conflicts or insufficiency of proof of title, then the insurer may apply to pay the amount into the Court, or, such an amount will earn interest at the prevalent rate applicable to a savings bank account. -

What if Claimant’s want to transfer the part/ full death claim proceeds in new business?

Transfer of part/full death claim proceeds in new business is not allowed.

-

What if nominee has also died along with the Life Assured or has expired prior to death of the Life Assured, then who will fill the Claimant’s statement / submit the claim documents?

If the Nominee has also expired, then Claimant's statement can be filled by the nearest blood relative who is claiming for Policy monies. However they would need to furnish legal documents as required by the Claims Dept to disburse the claim proceeds in their favour.

-

What if nominee is minor and there is no appointee stated in the application form, then who will fill the Claimant’s statement / submit the claim documents?

If the nominee is minor and there is no appointee, then claim forms needs to be filled by the individual who is custodian of the minor nominee. However they would need to furnish the legal documents as required by the Claims Dept to disburse the claim proceeds.

-

What is the Claim process / claim documents required if Policy is issued under HUF?

If the Karta under the Policy has expired, then claim documents needs to be filled by new Karta of HUF and the standard set of claim requirement needs to be submitted depending on early /non-early claim.

-

When is a Claim repudiated / rejected?

In the claims findings if it is established that there had been a material suppression of facts pertaining to the proposal information, which would have impacted the assessment of risk, if disclosed at the proposal stage, then it may lead to repudiation of the claim.

If documents submitted at the Proposal / Claims stage are not genuine, it would also lead to claim repudiation.

Hence it is very important to read through the Proposal form and submit factual details at the proposal stage and provide genuine Know Your Customer requirements to ensure that in case of the unfortunate event of death, the claim always gets paid. -

How can one file a Claim with the Company?

You can file your Claim in any of the following ways:

Website – Intimate claim online by clicking here,

Call us at our Toll free number 1-800-270-7000,

Visit your nearest Aditya Birla Sun Life Insurance Branch,

Email us at claims.lifeinsurance@adityabirlacapital.com,

Intimate the Claims Dept with the claim documents at below mentioned address:

Claims Dept,

Aditya Birla Sun Life Insurance Company Limited

G Corp Tech Park,

5th & 6th Floor,

Kasar Wadavali, Ghodbunder Road,

Thane - 400 601. -

How do I know what are the requirements meant for if I need to explain the claimant?

Please refer the glossary below of the various requirements called for:

Claimant's Statement: -

It is required to be completed by the person entitled to policy moneys.

Medical Attendant Certificate: -

It is to be filled by the doctor / hospital who attended on the life assured during his / her terminal illness or who certified his / her death. In case the Life Assured was not having any terminal illness prior to death and death was not certified by any doctor then it needs to be completed by the life assured's family physician.

Employer's Certificate: -

This has to be completed by the employer of the deceased.

Indemnity bond for loss of Original Policy Document: -

To be submitted where the Original Policy Document is lost / misplaced

FIR: -

FIR stands for First Information Report which is a written document prepared by Police Authorities generally when a complaint is lodged with the police by the victim of a cognizable offense or by someone on his or her behalf, but anyone can make such a report either orally or in writing to the police.

Post Mortem Report: -

An examination of a dead body to determine the cause of death.

Application for dispensing with Legal Evidence of Title: -

Application for dispensing with Legal evidence of title is only called if the policy was not nominated or Nominee has expired or if there is no appointee. The document is to establish the existing legal heirs of the deceased Life Assured. The document needs to be executed on a Non-Judicial Stamp Paper of Rs. 200/- and should be attested by Notary Public.

Guardianship Certificate: -

It's a Certificate issued by judicial authority to a legal guardian who has the legal authority to care for the personal and property interests of the Minor Nominee Succession Certificate.

Legal heirs Certificate: -

A Legal Heirship Certificate is issued by a Judicial Authority. Prior to the issuance of the Legal Heirship Certificate, a summary enquiry is undertaken by the Judicial Authority, through his or her functionaries, to ascertain the legal heirs of the deceased, so far as may be possible. A certificate is issued on the basis thereof. -

What are the requirements needed to carry out NEFT if there is a claim payout?

As per standard requirement Original pre-printed Cancelled Cheque containing Beneficiary's Name, Account Number and IFSC Code has to be submitted to carry out the electronic claim payment transaction.

In case of non availability of the above document, we requires copy of Passbook / Bank statement containing Beneficiary's Name, Account Number and IFSC Code.

If none of above documents are available then Printed Bankers Authorization in original on their letter head containing Account Number, IFSC Code and Beneficiary Name duly seal and signed by respective Bank Branch Manager would be required. -

What documents are required to file a claim?

To know the documents required to file a Individual Death claim, visit our website.

To know the documents required to file a Individual Rider claim, visit our website.

To know the documents required to file a Group Death claim, visit our website.

To know the documents required to file a Group Rider claim, visit our website.

To know the documents required to file a Social Death claim, visit our website.

To know the documents required to file a Health claim, visit our website. -

What are the requirements needed to carry out NEFT if there is a claim payout?

In rare cases where the Claimant's Bank does not participate in the NEFT Process either directly or indirectly, ABSLI may at its own discretion make Claim payment through cheque.

-

What if LA has died at home and claimant is not able to fill up the Medical Attendant Certificate?

In that case, Claimant needs to arrange the Medical Attendant's Certificate filled by the Hospital/ Family Doctor / Doctor which/ who had treated him/her during ailment prior to death or which/ who has certified him/ her dead.

In case there was no Family Doctor or Life Assured was not treated by any doctor during his/her life time then same needs to be provided as a written declaration by the Claimant. -

What is an alternate requirement if claimant has lost the original Policy document?

In case Claimant has lost the Original Policy Bond, then they need to provide the Indemnity Bond for loss of Policy document executed on Rs. 200 stamp paper duly notarized.

-

What is the Claim process of Aditya Birla Sun Life Insurance Company?

3 step Claim process:

Step1:

Claim Intimation - Intimate and submit the required set of documents.

Step2:

Claim Processing - Claim assessors will review the documents and guide you throughout the process.

Step3:

Claim Decision - Claims team will communicate the decision. Payments will be made through electronic transfer. -

Who should inform ABSLI about the claim?

The Nominee or the blood relatives / family members of the Life Assured should inform about the death of the Life Assured.

-

Whom should I contact if I need to know my claim status or need any help during claim process?

To know the status of the claim you can visit the “Manage Claims” page and track the claim status. You can also call up on the toll free no. 1-800-270-7000 or send an email to claims.lifeinsurance@adityabirlacapital.com or can visit the nearest Aditya Birla Sun life Insurance branch to know the status of the claim or for any assistance required.

-

What is the Claim process / claim documents required if Policy is issued under Keyman Insurance Policy?

If the policy is issued under the Keyman Insurance Policy, then standard set of claim documents needs to be submitted by the Employer depending on early /non-early claim and the claim monies would be disbursed in favour of the Employer.

At Aditya Birla Sun Life Insurance, we demonstrate customer centricity in everything we do. Our customers are our valued stakeholders, whose satisfaction is our foremost agenda. In case you are dissatisfied with our services, we have in place an internal mechanism to ensure effective and timely resolution of your complaints.

Please find appended key points regarding Grievance Handling/Redressal.

- Customer Request:

Communication received from a Customer soliciting a service such as a change or modification in the policy/requests for statement.

e.g. change in nomination, increase / decrease in sum assured, placing of a surrender request, request for a duplicate renewal premium receipt, request for unit statement (Policy account statement), etc

- Customer Query:

Customer contacts the Company primarily for information about the policy and/or its services and/or follows up on a status of a particular request within the stipulated regulatory time frame.

e.g. Information related to policy features, premium due, fund value, claim procedure, follow up on status of policy within regulatory timeframe as prescribed in the IRDAI servicing TATs.

- Customer Complaint:

Customer communicates and expresses dissatisfaction as there has been a lapse / deficiency in service

Company has defined its 'service delivery standards' for its core service delivery processes in line with the regulatory guidelines. This would be a base to ascertain deficiency of service.

Customer Complaint Resolution Process:

- All grievances (service and sales) received by us are responded to within the prescribed regulatory Turn Around Time (TAT) of 15 days.

- The complaint must be in the form of a letter signed by the policy holder or e-mail from the registered e-mail id

- A complaint can be registered by Contacting our toll free number or

- By Registering a complaint through our grievance redressal process on our website or

- By a letter signed by the policy owner

- By sending an email from the registered email id

- If required, we undertake complaints investigation by taking inputs from the customer over calls or personal meetings.

- We issue a written response as acknowledgement to the customer within 3 working days of the receipt of complaint. 3 working days to be replaced with 48 hours;

- The final response offers redressal of the complaint with the reason. To know more click here

-

At what age can you purchase a term insurance plan?

You can buy a term insurance plan anytime between 18 years to 65 years of age. As one’s age increases, the premium for the policy increases too. Hence, it is better to start early and in good health.

-

Decreasing Term Insurance

Policy Year Policy Term (upto 20 years) Policy Term (above 20 years) 1 to 5 100% 100% 6 to 10 90% 95% 11 to 15 75% 90% 16 to 20 50% 85% 21 to 25 N.A. 70% 25 to 30 N.A. 50% -

How can you buy term insurance?

Buying a term insurance plan is very easy. You can buy it online or offline. If you wish to buy term insurance online:

- Go to the website of your chosen insurance provider. Select the plan that meet your requirements.

- Fill up personal details such as name, gender, date of birth, policy term, smoking habit, city of residence, sum assured, mobile number, email id, etc

- The insurer would generate a quote based on the details which will let you know about the monthly/annual premium to be paid to get the term cover

- If you are satisfied with the quote, you would need to provide additional details such as nominee’s name, health and employment details, among others

- Make payment online through any of the digital payment modes

- Upload scanned copy of KYC documents and others as required

- The soft copy of the insurance policy will be mailed to your registered email id

In case you get stuck, you can call the customer care who will provide the necessary assistance. Also, most insurers have chatbots on their website to guide you with the entire process.

On the other hand, if you wish to buy term insurance offline, you can do so from an insurance advisor. Fill up the proposal form and submit the relevant documents. Whether you buy term insurance online or offline, make sure to provide accurate details, particularly related to your health. Hiding information may lead to a claim rejection.

Also, before policy issuance, you may need to undergo a medical examination. Insurers do so for better risk assessment. Make sure not to skip it as it may reveal conditions that you aren’t aware of.

-

How to choose the best term plan?

- Chose a plan that best answers the below questions for you What are the features offered by the plan? - Some important features to look out for will be flexibility in enhancing the cover as per your need, cover critical illnesses or cover all your protection needs.

- How much premium are you required to pay? – Do evaluate a term plan from a Company who has a legacy of trust and then identify the maximum coverage that you can get at an affordable cost

- What is your payment term? – Look out for a plan that provides you flexibility in choosing the payment term. For example, you may decide to pay premium in lumpsum amount or in monthly/yearly instalments

- What is the additional coverage (riders) being offered? – These are helpful additional features that you can check out like include waiver of premium, accidental benefits, etc.

- How good is the insurer’s claim settlement ratio? – The higher and more consistent the claim settlement ratio, the quicker and more robust is the company in its claim settlement process

- What is the insurer’s solvency ratio? - As per IRDAI, every life insurance provider should have a solvency ratio of 1.5, which tells if the company will be financially capable of settling your claim, should such a requirement arise.

-

Increasing Term Assurance with Waiver of Premium (WOP) Benefits

In addition to benefit applicable for Option 1, in case you are diagnosed with Critical Illness^ or Total and Permanent Disability^ whichever is earlier, all future premiums, if any, will be waived off and policy will continue till end of policy term.

-

What is the objective & utilization of Insurance Repository?

The objective of creating an insurance repository is to provide policyholders a facility to keep all his insurance policies in electronic form in one account and to undertake changes, modifications and revisions in the insurance policy with speed and accuracy.

Once the investor opens an account with a Repository. He can purchase subsequent policies from any insurance company without the hassle of submitting KYC documents (Know your customer documents, ID & Address proofs) again.

-

Which are the Policies eligible to hold in electronic form?

All individual life insurance policies, health and pension policies issued by registered life insurance, Health Insurance and General Insurance companies registered with IRDAI.

-

Which are the Policies eligible to hold in electronic form?

In order to hold e- insurance policies a separate and distinct e‐insurance account shall be opened with insurance repositories for keeping insurance policies in electronic form and the same shall be opened by a person who has insurance policies on his own or who proposes to take insurance policies.

-

What are the requirements to open the e-insurance account?

The documents that would be required are an Application form & KYC norms (ID Proof, Address Proof).

-

Is it possible to assign the Insurance Policy through insurance repository?

Subject to the provisions of insurance act and such Regulations, guidelines as may be made in this behalf from time to time, a policyholder may assign a policy of life insurance through insurance repository.

-

Are there any charges to open the e-insurance account?

Insurance companies will not charge the investor for issuing e-policies. The charge structure for opening a repository account is yet to be finalised. However, this is likely to be nominal.

-

I want to open an account. How to proceed?

The repositories will be operational in the next few weeks and thereafter account opening will start. We will inform you about the same once the process starts.

-

Which are the 4 different IR’S?

1) National Insurance Repository Limited

2) Central Insurance Repository Limited

3) Karvy Insurance Repository Limited

4) CAMS Insurance Repository Services Limited

-

What are the contact points of the Insurance Repository?

1) National Insurance Repository Limited - 91-22-49142631/49142502 helpdesk.nir@nsdl.co.in

2) Central Insurance Repository Limited - 1800-200-5533 / cirlhelpdesk@cdslindia.com

3) Karvy Insurance Repository Limited - 91 09642 546737 / eVault@karvy.com

4) CAMS Repository Services Limited - 1800-200-7737 / repository@camsonline.com

-

From which email ID will the customer get updates?

1) National Insurance Repository Limited - nir@ndml.in

2) Central Insurance Repository Limited - cirlhelpdesk@cdslindia.com

3) Karvy Insurance Repository Limited - eVault@karvy.com

4) CAMS Repository Services Limited – repository@camsonline.comt

-

How will the customer receive his login credentials and welcome kit?

The customer will receive his login credentials and welcome kit via email from the Insurance Repository. No email will be sent by Aditya Birla Sun Life Insurance Company Ltd.

-

If a customer has not received any update, whom should he/ she contact?

The customer can get in touch with the Insurance Repository’s touch points mentioned below.

1) National Insurance Repository Limited - 91-22-49142631/49142502 helpdesk.nir@nsdl.co.in

2) Central Insurance Repository Limited - 1800-200-5533 / cirlhelpdesk@cdslindia.com

3) Karvy Insurance Repository Limited - 91 09642 546737 / eVault@karvy.com

4) CAMS Repository Services Limited - 1800-200-7737 / repository@camsonline.com

-

How many days does it take to open an e-Insurance account after all the necessary formalities are completed?

An e-Insurance account will be opened within 7 days from the date of submission of application complete in all respects. Once, an account is opened, a welcome kit with the details of how to operate the same would be sent to the applicant/e-Insurance account holder.

-

Do I need to pay for opening of e-Insurance Account or on periodic basis?

NO. e-Insurance account is offered 'free of cost' to the applicants.

-

What is the objective of an Insurance Repository?

The objective of creating an insurance repository is to provide policyholders a facility to keep insurance policies in electronic form and to undertake changes, modifications and revisions in the insurance policy with speed and accuracy. In addition, the repository acts as a single stop for several policy service requirements. The Insurance repository system also brings about efficiency and transparency in the issuance and maintenance of insurance policies.

-

What is an Insurance Repository?

"Insurance Repository" means a company formed and registered under the Companies Act, 1956 (1 of 1956) and which has been granted a certificate of registration by Insurance Regulatory and Development Authority (IRDA) for maintaining data of insurance policies in Electronic form on behalf of Insurers. The Insurance Repositories provide the ease of holding insurance policies issued in an electronic form.

-

Can any individual/firm act as an Insurance Repository?

No, only an entity which is registered under company's act and who is granted a 'Certificate of Registration' by Insurance Regulatory and Development Authority (IRDA) can act as an Insurance Repository.

-

Can Insurance repository sell/solicit Insurance policy?

No, Insurance repositories cannot sell/solicit insurance policies. They are authorized only to maintain the policies in electronic form and provide a service record of all insurance policies.

-

What is an eIA (e-Insurance account)?

eIA stands for e-Insurance Account or "Electronic Insurance Account" which will safeguard the insurance policy documents of policyholders in electronic format. This e-Insurance account will facilitate the policyholder by providing access to the insurance portfolio at a click of a button through internet. IRDA has granted the Certificate of Registration to the following five entities to act as 'Insurance repositories' that are authorized to open e-Insurance Accounts:

a) M/s NSDL Database Management Limited

b) M/s CDSL Insurance Repository Limited

c) M/s SHCIL Projects Limited

d) M/s Karvy Insurance Repository Limited

e) M/s CAMS Insurance Repository Services Limited

Each e-Insurance Account will have a unique Account number and each account holder will be granted a unique Login ID and Password to access the electronic policies online.

-

What is an e-Insurance account application form? Where can it be obtained from?

An e-Insurance account application form is one that is used by an individual to open an e-insurance account with the Insurance Repository. This form would be available with Insurance Company, Insurance Repository or an Approved Person.

-

What are the requirements to be completed for opening an e-Insurance account?

An e-Insurance account holder or policyholder is required to:

a) Fill the e-Insurance account form and

b) Submit the following documents to the office of Insurance Repository or Insurance company or authorized

Approved Person (AP) appointed by Insurance Repository:

1. Photo ID

2. Recent passport size photograph

3. Cancelled Cheque ( In case of ECS/NEFT services for insurance premium payment transaction) and

4. Address proof

-

What are the requirements to be completed for opening an e-Insurance account?

An e-Insurance account holder or policyholder is required to:

a) Fill the e-Insurance account form and

b) Submit the following documents to the office of Insurance Repository or Insurance company or authorized

Approved Person (AP) appointed by Insurance Repository:

1. Photo ID

2. Recent passport size photograph

3. Cancelled Cheque ( In case of ECS/NEFT services for insurance premium payment transaction) and

4. Address proof

-

Can I open an e-Insurance account without having a life or non life policy for my own self?

Yes, an individual who is not having any insurance policy can open an e-Insurance account. After buying a policy, the policyholder can give a request for dematerialization to the Insurer or Insurance Repository or Approved Person.

-

How will I come to know that my e-Insurance account has been opened & how will I receive my User ID & Password?

Once e-Insurance account is created, you will receive a welcome kit. A pin mailer shall be sent separately. Using the login credentials and PIN, you can access and start using your e-Insurance account.

-

Can I convert my existing paper polices into electronic policies?

Yes, it is possible to convert the existing paper policies into electronic form. A service request may be made to the Insurance Repository or Insurer or the Approved person in this regard.

-

If I already have an e-Insurance account, how do I buy a new policy in electronic form?

Once you have opened an e Insurance Account, to buy a new policy in electronic form, you just need to quote your unique e-Insurance account number in your new insurance proposal form and make a request to issue policy in an electronic form.

-

Which are the insurance policies that can be held in electronic form?

All Life insurance, Health insurance, General insurance & Annuity policies that are issued by registered insurance companies with IRDA and who have signed up with the Insurance Repositories are eligible to be held in the electronic form.

-

How can I come to know that my policy is successfully credited into my e-Insurance Account?

You will receive a mail and SMS on your registered e-mail id and mobile number.

-

What are the charges for maintaining policies in electronic form?

All the services provided by Insurance repositories are FREE of charge.

-

What all policy details will be available in the e-insurance account?

A list of all policies that are credited will be available in the e-Insurance account. For each policy, policy level details like the status, commencement, maturity/expiry, nomination, assignment, endorsement, address, terms and conditions etc., would be available. In addition, the e-Insurance account holder will be able to download a copy of the policy bond.

-

Can ‘Nominee’ and ‘Authorized Representative’ be the same person?

Yes both Nominee and Authorized Representative can be the same person.

-

Can an Authorized Representative be changed?

Yes. Authorized Representative can be changed by making a request to the Insurance Repository.

-

Can any individual open more than one e-insurance account with any Insurance Repository?

NO. As per the IRDA guidelines, an individual cannot open multiple e-Insurance accounts.

-

How will the Authorized person deal with the e-Insurance account?

After the demise of the e-Insurance account holder and after settlement of all insurance claims, the Authorized representative needs to make a request to the Insurance Repository to close the e-Insurance account.

-

Is it possible to opt out of the Insurance repository system?

Yes, the policyholder shall make a request to his insurer and upon completion of all formalities in respect of the same, the hard copy of the policy document shall be made available.

-

Is it possible to shift from one Insurance repository to the other?

Yes, the e-Insurance account holder will have an option to shift from one Insurance Repository to the other. All the policy details and transaction history would then be transferred to the new Insurance repository.

-

What communications shall the e-Insurance account holder receive in a hard copy?

a) Welcome Kit with details of e-Insurance Account and modus operandi of its operation, the login ID.

b) A Pin mailer with the password.

c) The statement of account giving the details of all policies held whenever additional insurance is taken or a policy matures/ surrendered/ lapses would be provided to the e-insurance account holder.

d) When a new policy is issued the insurer shall send an insurance information sheet containing the basic details of insurance policy to the address stated.

-

What is the grievances redressal mechanism at Insurance Repository?

Every Insurance repository will have a policyholders’ grievances cell to address the grievances in respect of repository services and electronic policies held by them.

-

What is the procedure to effect changes in my policy or e-Insurance Account? Should the request be made to the Insurance Company or IR?

All requests in respect of either your e-Insurance account or any of the electronic policies may be made to the Insurance Repository. However, requests in respect of the policies can also be made directly with the Insurer concerned.

Upon a request, the Insurance repository would handle all servicing needs that fall within scope of their services directly and would forward the others to the Insurer concerned. An update to the policyholder would be provided by the Insurance Repository on the status of the request in respect of all the requests that it receives.

-

Which are the valid KYC documents?

Identity proof (any one):

a) PAN Card

b) UID

Address proof (any one):

a) Ration card

b) Passport

c) Aadhar letter

d) Voter ID card

e) Driving license

f) Bank Pass Book (not more than 6 months old)

g) Verified copies of:

i) Electricity bills (not more than 6 months old)

ii) Residence Telephone Bills (not more than 6 months old)

iii) Registered Lease and License agreement / Agreement for sale

Self-declaration by High Court and Supreme Court judges, giving the new address in respect of their own accounts.

Identity card/document with address, issued by:

a) Central/State Government and its Departments

b) Statutory/Regulatory Authorities

c) Public Sector Undertakings

d) Scheduled Commercial Banks

e) Public Financial Institutions

f) Colleges affiliated to universities

g) Professional Bodies such as ICAI, ICWAI, Bar Council etc. to their Members

-

Who is an Approved Person (AP)?

An Approved Person is a Point of Sale (PoS) appointed by Insurance Repository and will be working on behalf of Insurance Repository to extend the IR services.

-

Who is an Authorized Representative and what is his/her role?

An Authorized Representative is a person who is appointed by e-Insurance account holder to operate his/her e-Insurance account in case of unfortunate demise or incapability of e-Insurance account holder to operate the account. The Authorized Representative will intimate the Insurance Repository about the demise/incapability of policyholder with valid proof.

An Authorized Representative has only access rights to the e-Insurance account in the event of demise of the policy holder. The Authorized Representative would only to act as a facilitator and is not entitled to receive any policy benefits unless designated as a 'nominee' or 'assignee' by the deceased policy holder.

-

How many days does it take to open an e-Insurance account after all the necessary formalities are completed?

An e-Insurance account will be opened within 7 days from the date of submission of application complete in all respects. Once, an account is opened, a welcome kit with the details of how to operate the same would be sent to the applicant/e-Insurance account holder.

-

Do I need to pay for opening of e-Insurance Account or on periodic basis?

NO. e-Insurance account is offered 'free of cost' to the applicants.

-

What is the objective of an Insurance Repository?

The objective of creating an insurance repository is to provide policyholders a facility to keep insurance policies in electronic form and to undertake changes, modifications and revisions in the insurance policy with speed and accuracy. In addition, the repository acts as a single stop for several policy service requirements. The Insurance repository system also brings about efficiency and transparency in the issuance and maintenance of insurance policies.

-

What is an Insurance Repository?

"Insurance Repository" means a company formed and registered under the Companies Act, 1956 (1 of 1956) and which has been granted a certificate of registration by Insurance Regulatory and Development Authority (IRDA) for maintaining data of insurance policies in Electronic form on behalf of Insurers. The Insurance Repositories provide the ease of holding insurance policies issued in an electronic form.

-

Can any individual/firm act as an Insurance Repository?

No, only an entity which is registered under company's act and who is granted a 'Certificate of Registration' by Insurance Regulatory and Development Authority (IRDA) can act as an Insurance Repository.

-

Can Insurance repository sell/solicit Insurance policy?

No, Insurance repositories cannot sell/solicit insurance policies. They are authorized only to maintain the policies in electronic form and provide a service record of all insurance policies.

-

What is an eIA (e-Insurance account)?

eIA stands for e-Insurance Account or "Electronic Insurance Account" which will safeguard the insurance policy documents of policyholders in electronic format. This e-Insurance account will facilitate the policyholder by providing access to the insurance portfolio at a click of a button through internet. IRDA has granted the Certificate of Registration to the following five entities to act as 'Insurance repositories' that are authorized to open e-Insurance Accounts:

a) M/s NSDL Database Management Limited

b) M/s CDSL Insurance Repository Limited

c) M/s SHCIL Projects Limited

d) M/s Karvy Insurance Repository Limited

e) M/s CAMS Insurance Repository Services Limited

Each e-Insurance Account will have a unique Account number and each account holder will be granted a unique Login ID and Password to access the electronic policies online.

-

What is an e-Insurance account application form? Where can it be obtained from?

An e-Insurance account application form is one that is used by an individual to open an e-insurance account with the Insurance Repository. This form would be available with Insurance Company, Insurance Repository or an Approved Person.

-

What are the requirements to be completed for opening an e-Insurance account?

An e-Insurance account holder or policyholder is required to:

a) Fill the e-Insurance account form and

b) Submit the following documents to the office of Insurance Repository or Insurance company or authorized

Approved Person (AP) appointed by Insurance Repository:

1. Photo ID

2. Recent passport size photograph

3. Cancelled Cheque ( In case of ECS/NEFT services for insurance premium payment transaction) and

4. Address proof

-

What are the requirements to be completed for opening an e-Insurance account?

An e-Insurance account holder or policyholder is required to:

a) Fill the e-Insurance account form and

b) Submit the following documents to the office of Insurance Repository or Insurance company or authorized

Approved Person (AP) appointed by Insurance Repository:

1. Photo ID

2. Recent passport size photograph

3. Cancelled Cheque ( In case of ECS/NEFT services for insurance premium payment transaction) and

4. Address proof

-

Can I open an e-Insurance account without having a life or non life policy for my own self?

Yes, an individual who is not having any insurance policy can open an e-Insurance account. After buying a policy, the policyholder can give a request for dematerialization to the Insurer or Insurance Repository or Approved Person.

-

How will I come to know that my e-Insurance account has been opened & how will I receive my User ID & Password?

Once e-Insurance account is created, you will receive a welcome kit. A pin mailer shall be sent separately. Using the login credentials and PIN, you can access and start using your e-Insurance account.

-

Can I convert my existing paper polices into electronic policies?

Yes, it is possible to convert the existing paper policies into electronic form. A service request may be made to the Insurance Repository or Insurer or the Approved person in this regard.

-

If I already have an e-Insurance account, how do I buy a new policy in electronic form?

Once you have opened an e Insurance Account, to buy a new policy in electronic form, you just need to quote your unique e-Insurance account number in your new insurance proposal form and make a request to issue policy in an electronic form.

-

Which are the insurance policies that can be held in electronic form?

All Life insurance, Health insurance, General insurance & Annuity policies that are issued by registered insurance companies with IRDA and who have signed up with the Insurance Repositories are eligible to be held in the electronic form.

-

How can I come to know that my policy is successfully credited into my e-Insurance Account?

You will receive a mail and SMS on your registered e-mail id and mobile number.

-

What are the charges for maintaining policies in electronic form?

All the services provided by Insurance repositories are FREE of charge.

-

What all policy details will be available in the e-insurance account?

A list of all policies that are credited will be available in the e-Insurance account. For each policy, policy level details like the status, commencement, maturity/expiry, nomination, assignment, endorsement, address, terms and conditions etc., would be available. In addition, the e-Insurance account holder will be able to download a copy of the policy bond.

-

Can ‘Nominee’ and ‘Authorized Representative’ be the same person?

Yes both Nominee and Authorized Representative can be the same person.

-

Can an Authorized Representative be changed?

Yes. Authorized Representative can be changed by making a request to the Insurance Repository.

-

Can any individual open more than one e-insurance account with any Insurance Repository?

NO. As per the IRDA guidelines, an individual cannot open multiple e-Insurance accounts.

-

How will the Authorized person deal with the e-Insurance account?

After the demise of the e-Insurance account holder and after settlement of all insurance claims, the Authorized representative needs to make a request to the Insurance Repository to close the e-Insurance account.

-

Is it possible to opt out of the Insurance repository system?

Yes, the policyholder shall make a request to his insurer and upon completion of all formalities in respect of the same, the hard copy of the policy document shall be made available.

-

Is it possible to shift from one Insurance repository to the other?

Yes, the e-Insurance account holder will have an option to shift from one Insurance Repository to the other. All the policy details and transaction history would then be transferred to the new Insurance repository.

-

What communications shall the e-Insurance account holder receive in a hard copy?

a) Welcome Kit with details of e-Insurance Account and modus operandi of its operation, the login ID.

b) A Pin mailer with the password.

c) The statement of account giving the details of all policies held whenever additional insurance is taken or a policy matures/ surrendered/ lapses would be provided to the e-insurance account holder.

d) When a new policy is issued the insurer shall send an insurance information sheet containing the basic details of insurance policy to the address stated.

-

What is the grievances redressal mechanism at Insurance Repository?

Every Insurance repository will have a policyholders’ grievances cell to address the grievances in respect of repository services and electronic policies held by them.

-

What is the procedure to effect changes in my policy or e-Insurance Account? Should the request be made to the Insurance Company or IR?

All requests in respect of either your e-Insurance account or any of the electronic policies may be made to the Insurance Repository. However, requests in respect of the policies can also be made directly with the Insurer concerned.

Upon a request, the Insurance repository would handle all servicing needs that fall within scope of their services directly and would forward the others to the Insurer concerned. An update to the policyholder would be provided by the Insurance Repository on the status of the request in respect of all the requests that it receives.

-

Which are the valid KYC documents?

Identity proof (any one):

a) PAN Card

b) UID

Address proof (any one):

a) Ration card

b) Passport

c) Aadhar letter

d) Voter ID card

e) Driving license

f) Bank Pass Book (not more than 6 months old)

g) Verified copies of:

i) Electricity bills (not more than 6 months old)

ii) Residence Telephone Bills (not more than 6 months old)

iii) Registered Lease and License agreement / Agreement for sale

Self-declaration by High Court and Supreme Court judges, giving the new address in respect of their own accounts.

Identity card/document with address, issued by:

a) Central/State Government and its Departments

b) Statutory/Regulatory Authorities

c) Public Sector Undertakings

d) Scheduled Commercial Banks

e) Public Financial Institutions

f) Colleges affiliated to universities

g) Professional Bodies such as ICAI, ICWAI, Bar Council etc. to their Members

-

Who is an Approved Person (AP)?

An Approved Person is a Point of Sale (PoS) appointed by Insurance Repository and will be working on behalf of Insurance Repository to extend the IR services.

-

Who is an Authorized Representative and what is his/her role?

An Authorized Representative is a person who is appointed by e-Insurance account holder to operate his/her e-Insurance account in case of unfortunate demise or incapability of e-Insurance account holder to operate the account. The Authorized Representative will intimate the Insurance Repository about the demise/incapability of policyholder with valid proof.

An Authorized Representative has only access rights to the e-Insurance account in the event of demise of the policy holder. The Authorized Representative would only to act as a facilitator and is not entitled to receive any policy benefits unless designated as a 'nominee' or 'assignee' by the deceased policy holder.

-

What is an ‘asset class’?

An 'asset class' is a group of investment instruments such as equity, debt, cash, etc., which have similar investment risk and return profile. Equities comprise of investments in various company stocks and though contain high levels of risk, are the best performing asset over the long term. Debt investments mainly consist of fixed deposits, government securities, corporate debt, etc. These generate a fixed return and generally face lower risk as compared to equities. Cash investments include saving deposits and short term money market investments and are exposed to negligible risks.

-

What is a ‘risk – return’ profile?

The risk-return profile is the relationship between the risk that an asset class is exposed to and the returns it generates. Generally, higher the risk involved in an asset class, higher is the return associated with it. For example, equity has the potential to generate higher returns than debt, but at a higher risk. Cash on the other hand, though the safest asset class, generates the lowest returns. E.g. An individual who invested in the equity market in April-September 2009 would have generated a whooping 76% returns on his investment but if he had invested in the entire Financial Year 2009 - 2010 he would have incurred a loss on investment of -38%. Further, his investment would have grown at a Compounded Annual Growth Return (CAGR) of approx 23% had he invested for a period of 20 years ending in September 2009. On the other hand, savings in bank will generate a stable return of 3-4% per annum with no downside risk and no upside potential as well whereas value of cash kept at home without investing will keep shrinking over a longer period of time due to inflation.

-

How do I define my risk appetite?

To determine your risk appetite you will have to consider several factors such as your age, number of dependants, income, future goals, etc. Your risk appetite may not remain constant and change depending on your life stage and financial status.

-

What is meant by ‘asset allocation’?

The process of dividing your investments across different asset classes is known as 'asset allocation'. By spreading your investment across different asset classes, you create a diversified portfolio where the loss that you may make on a certain asset class can be compensated by the profits that you make on another. Thus, you reduce the overall risk of your investments.

-

How should I decide my optimum asset allocation between debt and equity?

Your risk appetite, investment objective and investment horizon will determine the asset allocation between debt and equity. Higher the risk appetite and longer the investment horizon larger will be the allocation towards equity and vice versa. An ideal portfolio should have a judicious mix of various asset classes.

-

What is market capitalization and what is the difference between large-cap and mid-cap stocks?

Market capitalization (market cap) represents the total market value of a company. It is calculated by multiplying the number of shares of the company with its current stock price. On the basis of this market cap, companies are segregated into large-caps, mid-caps and small caps. There is however no standard way to categorize the companies on the basis of this value. At ADITYA BIRLA SUN LIFE INSURANCE, we define mid-caps as companies having market capitalization between US$ 100mn to US$ 2bn. Generally, while large caps are considered to be the present industry leaders, mid caps are the emerging leaders of the future. Mid-caps offer higher risk-return profile than large caps. They rise faster than large-caps in bull markets, but may also fall at the same pace. when the markets collapse.

-

What are ‘growth’ and ‘value’ stocks?

A ‘growth’ stock is one that has the potential to generate higher returns than the overall market, and deliver substantial earnings. The stock is often traded at a higher value due to the expectation of high future earnings. A ‘value’ stock, on the other hand, is one that is undervalued, and is traded at a price that is much lower than its true worth. The undervaluation can be due to many reasons, for e.g. being in an industry which is going through a downturn etc

-

What is the ‘top-down’ and ‘bottom-up’ investment approach?

In top-down investing, overall economic and market environment is assessed to arrive at sectors that are likely to outperform the market. After selecting sectors, specific companies in those sectors are analyzed and chosen for investments. In bottom-up investing, extensive research and analysis is done on individual companies and they are chosen based on their future prospects and not on the basis of significant economic or market cycles. At ADITYA BIRLA SUN LIFE INSURANCE, we adopt a blend of both strategies.

-

What is the investment strategy of ADITYA BIRLA SUN LIFE INSURANCE?

ADITYA BIRLA SUN LIFE INSURANCE focuses on constructing high quality diversified equity portfolio which is skewed towards large-cap stocks with selective exposure to mid-caps. We invest in companies having clear business plans, scalable business model, efficient & visionary management as well as growth prospects. On the debt side, we predominantly invest in highest rated instruments to ensure better portfolio quality and liquidity.

-

What is an IPO? Does ADITYA BIRLA SUN LIFE INSURANCE invest in IPO’s?

When a company approaches the capital market with an issue of shares for the first time, the issue is called an ‘Initial Public Offering’ or an IPO. This process makes the way for listing and trading of the company’s equity shares on the stock exchanges. ADITYA BIRLA SUN LIFE INSURANCE invests in IPOs of fundamentally strong companies. Prior to investing, ADITYA BIRLA SUN LIFE INSURANCE conducts an in-depth research of the company with an emphasis on management quality and capabilities. An interaction with the company management is also undertaken to get a better understanding of their business model and future plans.

-

What are ‘ULIPs’?

A Unit Linked Insurance Plan (ULIP) is a life insurance policy, which offers the dual benefits of a protection for life and investments. The protection element is the underlying insurance cover while the investment element is that portion of the premium that is invested by the life insurance company on your behalf in a fund of your choice.

-

What is the benefit of investing in ULIPs?

ULIP is a unique investment avenue, which helps you fulfill your long-term financial goals. It fosters disciplined investment as it requires you to make investment at regular intervals. Being long-term in nature, it automatically provides a shield against short-term market volatility. It provides flexibility and transparency. Investment portfolios are disclosed on a monthly basis and Fund’s NAVs are disclosed on a daily basis. It offers a range of fund options with different asset allocations meeting the requirement of policyholders with different risk appetite. Investment in ULIP is eligible for tax deduction of Rs 100000 under Section 80(C) of Income Tax Act as per current tax laws

-

What would be the time period over which one could expect favourable returns from ULIPs?

ULIPs are well suited for meeting your long-term financial goals. The premiums paid by investors (net of insurance charges) are invested in funds as mandated by the policyholders. These funds invest in market-linked instruments such as equity, bonds and government securities. Since the returns on ULIPs are market-linked, they too might get impacted in short term. However, long-term returns do not get much impacted by such short-term volatilities. Over a long-term, one should expect favourable returns from ULIPs.

-

How should one analyse ULIP’s performance?

To analyse how well your ULIP has fared, compare the returns with the fund’s benchmark and peer group. The peer group should be of funds with similar asset allocation, investment strategy and asset quality (ratings, market capitalization and diversification). For example, a fund with a 20 per cent equity and 80 per cent debt exposure should be compared against fund options with similar asset allocation only.

-

What is a ‘benchmark’? What is my fund’s benchmark?

A benchmark is an index used by fund managers to compare the fund’s performance and portfolio risk. At ADITYA BIRLA SUN LIFE INSURANCE, we use BSE100 as a benchmark for equity investments, while CRISIL Composite Bond Index, CRISIL Liquid Index or CRISIL Short-Term Bond Index are used for debt investments.

-

How often does the ADITYA BIRLA SUN LIFE INSURANCE, investment team churn the fund portfolio and why?

Being a life insurance company, all investments are undertaken with a long-term view. We conduct active fund management and sell stocks if the fundamentals of the company/sector changes, valuations become too stretched or some other investment opportunity looks attractive in relative terms.

• Tax benefits are subject to changes in tax laws.

• Past performance is not indicative of future performance..

• Investment risk in the investment portfolio is borne by the policy holder.

Login

-

How do I access my Policy Account details online?

To access and manage your policy account online you would need your CIP/User Name and TPIN/Password.

-

I have a CIP/ TPIN, do I need to change over to User Name and Password?

Yes, you would need to change your CIP & TPIN to User Name & Password of your choice. To change the same click on the log-in tab and type in your existing CIP (10 digit number), then follow the instructions.

-

If I do not have an Existing CIP/User Name then how do I opt for online access?

Please click on Register tab and proceed to enter your Customer ID number followed by your registered e-mail id.

-

What are benefits of Online Access?

With your User Name and Password, you can manage your policy online. You can transact and view your policy details.

Online access benefit's

• Change or update your contact details.

• Change the mode of your policy.

• Switch of funds and Premium redirection.

• Pay your premiums online (even for policies which are lapsed).

• Generate the reinstatement quote. -

Why am I unable to log in?

You may have trouble logging in because of incorrect CIP/User Name and Password.

-

What do I need to do if I have forgotten my User Name or Password?

If you have forgotten your User Name or Password, kindly click on the Forgot User name link and follow the instructions provided. After you have correctly responded to validation questions, the details are sent to your registered e-mail Id.

-

What is the meaning of Password locked?

Your Password would be locked after you exceed the maximum number of five attempts for Login. Once your password is locked, you will have to wait for 15-20 minutes or else can request for a new password by clicking on forgot User Password

-

What is Survival Benefit?

Survival Benefit is the amount which is paid to the policy holder at the end of the policy term on Monthly/Quarterly/Annually basis the due date of the policy.

-

Where to submit the Survival Certificate?

Submit the survival certificate at nearest ABSLI branch. To locate a ABSLI branch nearest to you, click here: https://www.adityabirlacapital.com/branch-locator (Timings: Monday to Saturday 9:30 am to 6:00 pm).

Or

Submit the Survival Certificate through our Customer Portal.

Follow the below steps to upload the Survival Certificate through Customer Portal

Who has ONE ABC Login

Who don't have ONE ABC Login

Register user can login by ONE ABC ID

Login with password or login with OTPClick on Manage my Policy -> Policy Servicing -> Submit Survival Certificate

Click on My Services –> My policy Details -> Submit Survival Certificate

Enter Registered Email ID/ Mobile No./ Policy No. and Primary Life Insured Date of Birth. In the OTP screen, enter the password and click on "Verify"

On the policy dashboard screen click on "Submit Survival Certificate" button.

On the policy dashboard screen click the "Submit Survival Certificate" button.

Agree T&C and click on "Allow" to access camera. Smile and say "Namaste ABSLI"Or just smile while using phone to click selfie.

Agree T&C and click on "Allow" to access camera. Smile and say "Namaste ABSLI"Or just smile while using phone to click selfie

Upload PAN or Aadhaar card images - front/main side only. This can be done by capturing a fresh photo through the screen or by choosing the upload option if you already have an image stored on your device

Upload PAN or Aadhaar card images - front/main side only. This can be done by capturing a fresh photo through the screen or by choosing the upload option if you already have an image stored on your device

If all steps have been done properly, you will receive a "Success" message confirming your request number

If all steps have been done properly, you will receive a "Success" message confirming your request number

-

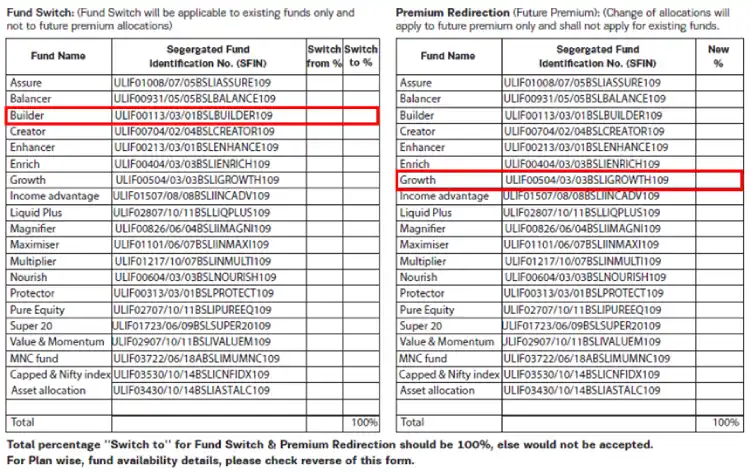

What is Switch in fund & Premium Redirection?

Switch in Fund – Fund Switch is the facility provided to the policy owner to switch existing fund option in the policy to available fund options as per the plan. On receiving this request, the existing fund value is moved to the fund requested by the customer.

Premium redirection – Premium redirection or Premium Allocation is an option given to the customer to redirect future premiums in requested fund available under the plan. Existing funds will continue to remain in old funds unless switch request is accompanied with the premium redirection request.

-

Where to submit Fund Switch / Premium Redirection request?

- Branches: Submit fund switch form duly Signed by the Policy Owner. To locate nearest ABSLI branch click here: https://www.adityabirlacapital.com/branch-locator (Timings: Monday to Saturday 9:30 am to 6:00 pm).

- Email: Submit switch request by writing to us on care.lifeinsurance@adityabirlacapital.com from registered email id. Provided if the client has invested in multiple funds then you have mention in email, the fund to which you wish to transfer and percentage or can also send scan copy of switch form.

- Contact Centre: Submit the request by calling on our toll-free number 1800270700 (Timing: Daily, 10 am – 7 pm).

- Website: Submit fund switch request through Customer Portal.

Follow below steps to submit the request through Customer Portal (Timing: Daily, 10 am – 7 pm).Step 1

Step 2

Click on – PROTECTING – Life Insurance

Step 3

Click on – Mange My Policy - Switch Fund Option

Step 4

Update mobile number/Registered Email ID/ Policy Number and Update Primary Life Insured Date of Birth. Click on Send OTP

Step 5

Once customer Complete OTP process he/she will redirected to Fund Switch / Premium Redirection page.

Step 6

Customers need to fulfill all requirement asked on page

Step 7

On this screen it will show you the current funds with fund value and below you can enter the %age of fund where you want to do switching and click on "NEXT"

Step 8

Submit the request once all details are mentioned.

Important Points:

- In case of Investor profile change from guaranteed to self-managed fund, client must opt both “Fund Switch” and “Re – direction” option on fund switch from existing fund to new funds and re- allocation for future fund allocation.

Example:

-

Which NAV is applicable for the requests?

If Fund Switch/premium redirection request is received and accepted at branch/contact centre/website before or at 3.00 pm then applicable NAV will be of the same day provided it is a business working day or else NAV of next working day is applied.

If Switch in fund/premium redirection request is received and accepted at branch/contact centre/website after 3.00 pm then applicable NAV will of the next day provided it is a business working day or else NAV of next working day is applied. Also, If the request is submitted on holidays then applicable NAV will be of next day.

-

My Policy is about to get Mature, What do I need to do?

If your Bank account details are already updated, maturity benefits would be automatically transferred to the registered bank account, depending upon the plan features.

To check your registered bank details or to register/update your bank details now, click here: https://lifeinsurance.adityabirlacapital.com/customer-service/manage-your-policy/edit-bank-account-details

In case you don’t receive the Maturity amount or cheque in 15 days from the Maturity date, you may reach out to our customer support through Email/Call/Branch.

Note - 1: While submitting the documents through Email/Branch, if the request is submitted by any person other than the policy owner, photo id proof of that person is also required.

Note - 2: In case of NRE transfer, bank statement with premium payment transactions need to be submitted at the customer support touchpoints.

NRI customers can also send Email to our NRI helpdesk : Absli.nrihelpdesk@adityabirlacapital.com

Note - 3: In case of Maturity of Deferred Pension Plan, Please reach out to any of the customer support touchpoints to opt out commutation and annuity benefit.

For further assistance, reach us at:

- Call us: 18002707000 (Timings: Daily, 10 am - 7 pm)

- Email Us: care.lifeinsurance@adityabirlacapital.com

ABSLI Branch visiting hours: To locate a ABSLI branch nearest to you, click here: https://www.adityabirlacapital.com/branch-locator (Timings: Monday to Saturday 9:30 am to 6:00 pm)

-

What is my Policy Number and Client ID?

The policy number consists of nine digits and can be found at the right hand side of the first premium receipt of your policy document.

This is a unique identification number that distinguishes your policies from other policies and will remain unchanged throughout the lifetime of the policy.

Remember to quote the policy number every time in your correspondence, as it helps us to locate your records for reference.

Whereas, the client ID consists of ten digits, which is located at the left hand side of the first premium receipt of your policy document. This ID remains unique if you have more than one policy with us.

This provides an alternative to your policy number. Easy to remember one client ID, if you have more than one policy number. -

Are Policy Conditions different for all policies?

Every policy is taken for different types of needs; therefore the conditions for your policy will vary according to the Plan and Term of the policy.

Policy document consist of a. Your Personal Details, b. First Premium Receipt and c. Your Policy Details. Hence it is important that you read the policy document and understand the policy conditions. The details like annual premium for your policy, the premium payment term and the term of the policy, the maturity date of the policy, the maturity value of the policy are mentioned in the policy document's' Your Policy Details' page.

The policy features are stated in the policy value provisions. Request you to refer to the policy value provisions depending upon your requirement you may avail the features offered. -

What if I lose my Policy documents?

Kindly make a thorough search before concluding that you have lost the policy document. Look for the same within your residence, among your investment papers, at your office and even with your agent to whom you might have entrusted the document for some reason.

It could have been even pledged with us/any other financial institution for availing a loan by you. We retain the policy document when you go in for a loan against the policy. Make sure that the document you are searching is not one that has already been assigned to us, or to another financial institution.

If the policy document is partially destroyed due to natural causes like, fire, flood, etc, the remaining portion may be returned as evidence of loss of policy to us, while applying for a duplicate policy.

In case you are sure that the policy document is untraceable due to unknown causes, there is a simple procedure to comply with while applying for the duplicate policy at the branch that services your policy. You may submit an Indemnity bond executed on a stamp paper of Rs. 500 if you reside within Maharashtra or Rs. 200 if you reside outside of Maharashtra. The stamp paper needs to be duly signed by you (policy owner) along with the below requirements.

• Self-attested Address proof (validity 6 months), also to be attested by ABSLI authorized signatory.

• Self-attested Identity proof also to be attested by ABSLI authorized signatory.

To locate the nearest branch, click here

Once we receive your request, the duplicate policy documents will be dispatched to your registered mailing address within 10 days. -

Your Contact Address & Number – Keep Us Posted without Fail

Your address is very important for us. Without your latest address we would not be in a position to contact you for any service offering. We would not like to keep any benefit that is due to you pending for want of this very important information. Whenever you shift residences, please inform the new address to us. Otherwise any communication we send to you, like premium notices, discharge vouchers for maturity and survival benefits etc., will get delayed in reaching you

To change your address, you may submit a Policy service request form to any of our branches, along with the below requirements;

• Self-attested Address proof (validity 6 months), also to be attested by ABSLI authorized signatory.

• Self-attested Identity proof also to be attested by ABSLI authorized signatory

You can update your contact numbers and email addresses on our website using your CIP / TPIN. -

How do I change my name?

Do let us know in case of any change of name by providing a copy of the gazette notification or a copy of the marriage certificate in case of change in name due to marriage. For all other request with significant name change, a copy of the gazette notification is required. Certified true copy (ies) of the supporting document should also be enclosed.

.

In case of a correction in name, please enclose a copy of any of the following:

• Passport

• PAN Card

• Voter's Identity Card

• Driving license

You may submit a Policy service request form to any of our branches along with the above stated requirement(s).

To locate the nearest branch, click here

Once we receive your request, the name change endorsement letter will be dispatched to your registered mailing address within 10 days. -

What is Nomination? And how do I nominate?

Nomination enables speedy processing of claims ensuring that your loved ones get hassle free-access to the policy benefits in their hour of need.

Nominee is possible where owner and insured is the same person.

You may nominate more than one person under a policy; however percentage wise nomination is permitted. You may also change/add nominees anytime during the tenure of the policy.

A minor can be nominated, however for all such nomination an appointee who is a Major need to be appointed.

Click here for the Nomination form to be used for fresh/addition/change of nominee. The form should be completely filled in all respects. -

What is Assignment? How do I assign the policy?

Assignment is a means whereby the beneficial interest, rights and title under a policy get transferred from assignor to assignee. Insurance Act, 1938 recognizes only one mode of transfer of ownership of an insurance policy i.e., assignment under Section 38 of the Act.

Assignor is the policy owner who transfers the title of the policy and assignee is the person who derives the title to the policy from the assignor.

To assign the policy you can fill the Assignment form and submit to any of our branches along with the below requirements.

Original Policy contract/document

• Photograph of the proposes/new policy owner Not required in case of assignment to banks/Financial Institutions for loan.

Note: In case of assignment to banks /Financial Institutions for loan the following documents are required;

Identity Proof

• Passport

• PAN card

• Voter's Identity card

• Driving license

• Letter from any recognised public authority or public servant verifying the identity and residence of the customer

Residence Proof (last 3 months)

• Telephone bill

• Bank account statement

• Electricity bill

• Ration card

• Letter from any recognized public authority.

Income Proof (only in case of the total annual premium contribution for all the policies attached to the assignee id is Rs. 1 Lakh or above. Policies where assignee is owner and payee or just payee need to be considered for this calculation). -

Can the ownership of the policy be changed in case of unfortunate death of policy owner?

Yes, you need to fill up the Deed of Relinquishment form along with the below mentioned requirement/s;

.

• Change in ownership form

• Deed of relinquishment DOR should be notarized on a Rs.200 stamp paper

• Death certificate

• Photograph of the proposed policy owner

• Proof of identity of the proposed policy owner

• Proof of residence of the proposed policy owner

• Proof of Income of the proposed owner.

Note: The income proof is required only in case of the total annual premium contribution for all the policies attached to the assignee id is Rs. 1 Lakh or above. Policies where assignee is owner and payee or just payee need to be considered for this calculation. -

When to Pay the Premiums?

Remember to pay your premium in time i.e. on the due date mentioned in the policy document. Aditya Birla Sun Life Insurance sends renewal notice one month prior to your due date. However there may be postal delays / issues leading to non receipt / delay in receipt of renewal notice.

. -

Does my policy immediately lapse if I don't make a premium payment on the due date?

In case you have not paid the premium within the due date there is still time for you to make the payments without payment of interest on the premium. This period is called the grace period.

The grace period for policies where the premium payment mode is monthly is 15 days from the due date. (For plans issued from September 01, 2010)

The grace period for policies where the premium payment mode is quarterly, half-yearly or yearly is one month but not less than 30 days. -

What are the premium payment options available for me?

Online payment - Make an online payment on our website - www.lifeinsurance.adityabirlacapital.com.

.

ECS / Direct Debit – Make regular premium payment debit from your bank account by registering for ECS / Direct Debit. To download the form Click here.

Direct Debit from credit card – Enroll your credit card and avail the benefit of SIP. To download the form Click here.

Branch Office - You can pay your premiums at our branch by cheque or cash.

Bill Junction / Bill Desk – You can also authorize your premium payments online through Bill Desk / Bill Junction.

NEFT - NEFT is a secure way of making premium payment on the bank's website. -

How is the facility of ECS availed? And how many days will it take to get the ECS to get activated?

Activating the ECS facility is a one-time activity. The policyholder should fill up the Auto Debit Form and get it verified and certified by the Bank where the Bank Account is maintained. The Mandate form should be sent to the nearest ABSLI branch with an original cancelled cheque.

It takes 30 days for the first time.

• What does this service cost me?

It costs nothing. This service is free of charge

• When will the premium amount get debited?