Buying inadequate insurance may be equal to buying no cover at all.

Why?

Let’s look at an example. Manish lives in Mumbai with his spouse, kids, and parents. His spouse is a homemaker and his kids are in middle school. His parents need medical checkups each month. Manish earns Rs 12,00,000 annually and decides to purchase a term plan with a 1 crore cover, without calculating the financial needs of his family. He passes away suddenly, leaving behind a home loan of Rs 60,00,000. Will the 1 crore cover amount be enough for his family, considering all of them are financial dependents?

Spoiler Alert - No. The loan will take up a huge chunk of the cover amount, there will be daily expenses, school fees, medical bills, etc. to be paid. His family’s comfortable lifestyle will be hampered and they’ll have to limit their dreams (higher education abroad, two big weddings, and such).

This is the very reason why you shouldn’t rely on thumb rules. Thumb rules do not cater to your and your family’s individual needs. It’s absolutely pertinent to use a systematic method of calculation while figuring out the cover you need - based on your lifestyle, income, needs, and requirements.

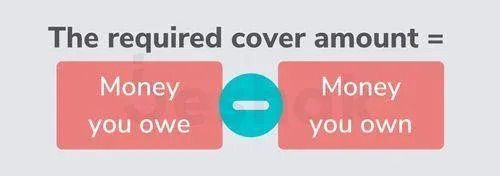

Now, you buy Term Insurance to protect family members dependent on your earnings, from any financial disruptions, when you pass away. The financial disruption will be caused by the gap between what you will leave behind and what your family actually needs.

How Do You Calculate This Gap

‘20x your yearly income' is the most commonly recommended thumb-rule formula for calculating the cover. But, like every thumb rule, this one too has its flaws, and you've got to be extra careful.

What you should ideally do as your first step in calculating this ‘gap’ or the cover you need is -

- Calculate the amount you owe

- Calculate the amount you own

You might be wondering how each of these amounts should be calculated and what factors contribute to each one of them. Let’s dig deeper to make sure you have included everything.

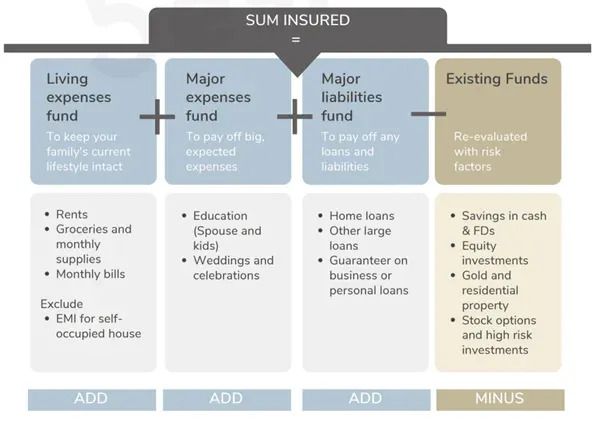

The amount you owe

This is the amount your family will have to pay for, in the absence of the breadwinner. It includes short-term everyday and long-term expenses.

This can be categorized and calculated under three headers -

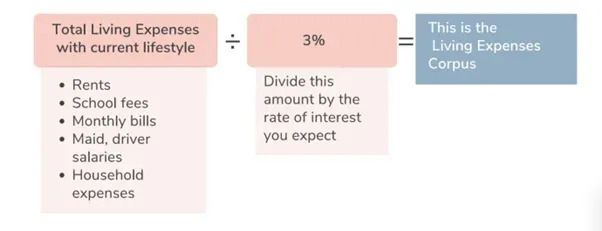

A. Living expenses corpus:

This corpus will provide regular passive income for your family’s everyday needs. You can arrive at this number by summing up all your monthly and yearly expenses such as rents, school fees, maid/ driver salaries, groceries, and other household expenses for one year. Divide this total by the expected rate of interest. (Take this as 3% which is the current rate of interest on FDs after cutting taxes).

B. Big dreams fund:

These are all the large, one-time expenses your family will incur in the long run. In this, include all the big dreams (like your wife’s MBA, kid’s international education, kid’s destination wedding, etc.)

C. Major liabilities fund:

Here, you will account for all the loans and liabilities that you owe, and your family will have to pay off when you die. Sum all the loans you’ve taken (house loans, car loans, personal loans, etc.), any joint loans you’re liable for as well as any other loans that you’ve signed as a guarantor for. When you sum these three, you will get the total amount you owe.

Next, moving to the amount you have.

The amount you own

Take a complete stock of the existing funds you hold. This is the money or financial assets that you currently have - Fixed deposits, Mutual Funds, Equity shares, Cash, Cash in the bank, etc.

It might seem pretty straightforward that you will simply add up all the money and value of assets you’ve got. But, that’s where you will go wrong.

You see, not all assets have the same risk factor. Meaning, not all of them might be readily available for your family - as liquid funds to spend on their needs. So, you will have to multiply these risk factors to plan for the worst-case scenario. Here are the risk factors you should consider.

- Existing Life Insurance Covers @ 100%

- Savings, FDs & Cash @ 100% - You can consider these amounts at a 100% value

- Equity investments @ 50% - Conservatively, take all your equity shares and equity-linked investments at half their total value

- Gold & residential property@ 0%: Practically speaking, you would not want these assets to be liquidated for grocery purchases. So, take them at zero value.

- Stock options @ 0%: As these are high-risk investments, take them at zero value. If any of them pay off, consider it a bonus.

Summing up all these numbers will give you the actual amount you own.

Now, you can calculate the total cover or sum insured you will need using the formula -

This is the most meticulous and scientific way to calculate the exact amount that your family needs - instead of depending on a random figure.

Let’s look at an example to understand how this works.

Sakshi is a 27-year-old analyst, who draws a yearly salary of 6 lakh rupees. This is how her finances look, at this moment.

Her expenses

|

Current Living Expenses

|

Rs 30,000/- per month (excluding EMIs on loan)

|

|

Major Expenses - Planning to do a masters from a premier university in the next 3 years

|

Rs 50 Lakhs

|

|

Major Liabilities |

No liabilities

|

|

Existing Funds - Savings

|

- Savings - Rs 5 Lakhs

- Mutual Fund - 20 Lakhs

- Fixed Deposit - 5 Lakhs

|

Let’s retabulate these figures to make the calculation simpler.

Money Sakshi owes

|

Living Expenses Fund

|

Rs 30,000 × 12 ÷ 3% = Rs 1.2 crores

|

|

Major Expenses Fund |

Rs 50 lakhs |

|

Major Liabilities |

Zero

|

|

Total Liabilities

|

Rs 1.7 crores

|

Money Sakshi owns

|

Savings @100%

|

Rs 5 Lakhs X 100% = 5 Lakhs

|

|

Fixed Deposit @100% |

Rs 5 Lakhs X 100% = 5 Lakhs

|

|

Mutual Funds @50% |

Rs 20 Lakhs × 50% = Rs 10 Lakhs

|

|

Total Existing Fund |

Rs 20 Lakhs

|

So, the required cover for Sakshi is the difference between her liabilities and her existing funds.

Liabilities - Existing fund = 1.7 Crores - 20 Lakhs = 1.5 Crores

If she went by the usual calculation of 20X her yearly salary, she would only take a cover of 20 X 6 Lakhs, that is - 1.2 Crore Rupees, leaving her family without a sufficient cover - 30 lakhs short.

Further, in this calculation, we haven't factored inflation. If you have to - you should factor at least 2.5X this coverage amount or buy an increasing cover that takes your cover systematically to 2X.

But what about inflation?

For the sake of simplicity, this calculation considers a scenario where death happens today.

We strongly recommend you opt for the increasing cover option available with all leading term life insurance plans - this will ensure your cover increases systematically over a period of time beating inflation.

If you want to factor in inflation for the entire term right now, you may multiply this cover amount by 2.5 to 3X to calculate the inflation-proof cover you need.

Pro Tip: Maintain and monitor your expenses, financial goals, investments, and liabilities in your personal financial spreadsheet. Take your dependents through this sheet and share access with them.

If you have any other insurance cover, you can subtract that amount from the cover needed. Make sure that you review your cover amount every few years, to ensure you account for any new, unplanned responsibilities you take up.

So, use this scientific method to calculate the term insurance cover your family needs instead of relying on thumb rules and precedents. Every family has a unique set of needs and requirements, and it’s important to consider every aspect of your finances and expenses to calculate the cover you need.

Key takeaways from this chapter

Key takeaways from this chapter