Home Loans

Home Loans

Personal

Loans

Personal

Loans

SME Loans

SME Loans

Business Loans - Udyog

Plus

Business Loans - Udyog

Plus

Loan against Securities

Loan against Securities

Mutual Funds

Mutual Funds

Stock and

Securities

Stock and

Securities

Portfolio

Management Services

Portfolio

Management Services

Pension Funds

Pension Funds

Life

Insurance

Life

Insurance

Health

Insurance

Health

Insurance

Wellness

Solutions

Wellness

Solutions

Pay Bills

Pay Bills

Pay anyone

Pay anyone

Pay on call

Pay on call

Payment

Lounge

Payment

Lounge

ABC Credit

Cards

ABC Credit

Cards

1800-270-7000

1800-270-7000

none

Module 03 Term Insurance

Ch. 12: Customization in Term Plans?

Share

Index

What Is Term Insurance

When To Buy Term Plan

Why Should You Buy Term Plan

Who Should Buy Term Insurance

Where to Buy Term Insurance From

How to Buy Term Plan

How Much Cover Do I Need

Saral Jeevan Bima

Term Insurance Riders

Exclusions in Term Insurance

Term Insurance Claims Process

Customization in Term Plans

Benefits of Buying Term Insurance

Decreasing Term Insurance

Group Term Insurance

Married Women’s Property Act

Claim payout options

Eligibility Requirements

How Does It Work

Increasing Cover

Life Stage Benefit

Things To Keep In Mind IG

Types of Term Insurance Plans

Whole Life Term Insurance

Term Insurance Tax Benefits*

-

Key takeaways from this chapter

Key takeaways from this chapter

Customize Term Insurance Plans

Premium Payment Frequency

Claim Payout Options

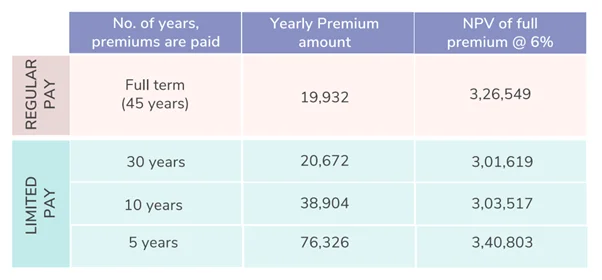

Premium Pay Model

Does Limited Pay save money?

Insurance Riders

How much helpful you found this article?

3.7

Rated by 7 readers

/ 5 ( reviews )

Not Helpful

Somewhat Helpful

Helpful

Good

Best

Thank you for your feedback

Share

Get Guaranteed Returns After a Month^

Unlock the Power of Smart Investment!

Looking to buy Term Plan

ABSLI Salaried Term Plan

Exclusively For Salaried Individuals

Optional Accelerated Critical Illness benefit

Inbuilt Terminal Illness Benefit

Life Cover upto 70 years

4 Plan Options

Life Cover

₹1 crore

Premium:

₹492/month¹

-

Disclaimer

ABSLI Salaried Term Plan (UIN:109N141V01) is a non-linked non-participating individual pure risk premium life insurance plan; upon Policyholder’s selection of Plan Option 2 (Life Cover with ROP) this product shall be a non-linked non-participating individual savings life insurance plan.

¹ LI Age 21, Male, Non Smoker, Option 1: Life Cover, PPT: Regular Pay, SA: ₹ 1 Cr., PT: 10 years, Premium paying term: 10 years, Annual Premium: ₹ 5900/- ( which is ₹ 491.66/month) Premium exclusive of GST. On death, 1 Cr SA is paid and the policy terminates.

ADV/4/22-23/79